MONDAY MACRO: How the Philippine central bank impacts corporations and the overall economy

While it is easy to see how the Philippine government supports the economy through legislation and fiscal policy, its role through monetary policy might not be as easily understood.

Today, we’ll discuss one of the central bank’s main tools in supporting the economy during recessions and how it may impact people’s investments in the stock market.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

As the Philippines moves towards slowly returning to pre-pandemic levels of activity, all eyes are on the national government and how it can maintain the economy’s recovery while keeping the number of COVID-19 cases at a minimum.

Used correctly, the many tools at its disposal should help the government support the recovery. The most common tools are legislation and fiscal policy.

For example, during the pandemic, the government used legislation when it enacted the Bayanihan to Heal as One Act in May 2020 and the Bayanihan to Recover as One Act in September 2020. As for fiscal policy, President Duterte signed into law the 2021 budget that prioritizes efforts to address the pandemic.

Other than these more direct approaches, the Philippine government can also support the economy through monetary policy via the Banko Sentral ng Pilipinas (BSP).

The impact of monetary policy can at times go unnoticed because any discussion of this matter can get too technical and the relationships between indicators can get confusing. Nonetheless, we’ll be discussing one of its main purposes—the control of interest rates—and how it impacts investors.

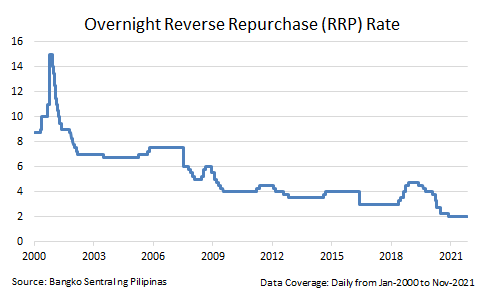

When talking about interest rates in relation to the BSP, we often mean the Overnight Reverse Repurchase (RRP) rate.

The RRP rate is essentially the interest rate various banks need to borrow from the BSP to meet their daily liquidity requirements. It is the benchmark interest rate because it sets the interest rates of all other loans.

Specifically, the interest rate of interbank loans is capped by the RRP rate. If it becomes more expensive for one bank to borrow from another bank, it can go to the BSP instead.

The same concept applies to business and consumer loans. If borrowing costs are low for banks (low RRP rate), chances are some banks will take advantage of this low rate and offer their clients cheaper rates. That means in order to remain competitive, other banks will also lower the interest they charge on loans or else risk losing their clients to competitors with a cheaper offering.

This is why a lot of people monitor the RRP rate and how the BSP will act in the future. Changes in monetary policy can have a significant impact on the economy.

During economic recessions, the BSP can drastically lower the RRP rate to stimulate Philippine aggregate demand. Businesses can take on more capital projects since the returns needed are much lower and consumers can spend a greater amount with borrowing being cheaper.

However, it is not always prudent to have a low RRP rate. Maintaining low rates would mean that in future recessions, further lowering RRP rates will no longer be effective. This is one of the reasons why central banks gradually raise interest rates during periods of economic expansion.

Another reason why a low RRP rate can be unfavorable is higher aggregate demand as a result of lower costs to borrow will eventually lead to high inflation. This is the reason why some analysts disagree with the BSP’s current policy stance.

BSP Governor Benjamin Diokno has recently communicated that interest rates will remain at a historical low of 2% through the end of the year.

While aggregate demand and borrowers will continue to benefit from the BSP’s decision, high inflation is likely to persist in the near-term. As of October 2021, inflation is at 4.6%, still higher than the BSP’s guidance range of 2%-4%.

That said, the BSP claims action is not yet needed and the higher-than-expected inflation is only transitory since the inflationary pressures are mainly due to supply constraints of a limited number of items like oil and some food items.

Regardless, for long-term investors, these inflationary pressures are nothing to be concerned about. When we discuss one of the other functions of the BSP, we’ll show what really drives inflation in the long-term.

As a result, low interest rates are a net benefit to those investing long-term in the Philippine stock market.

As companies release their Q3 2021 results, it’s becoming more evident that 2021 is a step up compared to 2020 when aggregate Uniform ROA was at a decade-low of 4%.

Now, with the government’s continued support through low interest rates and other policies, it is likely 2022 will be an even better year. If this scenario materializes, we will see Uniform ROAs return to pre-pandemic levels, possibly even higher.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com