MONDAY MACRO: Improvements in FDIs in the Philippines could boost Philippine economic growth, justifying 24x Uniform P/E and steady 6% Uniform ROA

The trade war between two of the biggest economies in the world has caused economic ripple effects throughout the international community, including in the Philippines.

Central banks around the world reacted to the US-China trade war concerns by cutting their interest rates in 2019. Multinational companies reacted by limiting their exposure to foreign investments. This resulted in the decline in net foreign direct investments (FDI) in the Philippines.

Though FDIs have been declining since 2017, driven by the decrease in equity capital, prospects for growth in the Philippines still remain positive. Changes to the rules governing these FDIs aim to attract once more these long-term investments despite continued sluggish global economic activity.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Foreign Direct Investments (FDI) refer to a controlling ownership of a foreign entity, usually foreign companies, in a business operating in another country.

An increase in FDI in the Philippines means more foreign companies are putting money into Philippine companies by investing not just their financial capital, but also their skills and knowledge. This is a form of long-term investing in another country.

FDIs are very different from the short-term foreign investments that are often termed as “hot money.” Hot money refers to foreign investments in stock or credit portfolios, where the foreign owners have no intention of taking part in the company’s daily operations.

Some of the long-term investors in Philippine businesses are the United States, Japan, Singapore, South Korea, and China. Most of their equity capital investments in 2019 went to financial services, insurance, real estate, and manufacturing.

In the past years, strict laws on foreign ownership and employment restrictions in the Philippines have resulted in low FDI versus other countries.

The Foreign Investments Act (FIA) of 1991 states that foreign investors can only have up to 40% of foreign equity ownership of local firms.

Moreover, foreign investors cannot own equity in small and medium-sized enterprises (SMEs) with paid-in capital less than the equivalent of US$200,000.

They can, however, invest in SMEs if they have advanced technology as determined by the Department of Science and Technology (DOST) or they employ at least 50 direct employees. If they satisfy either condition, then a minimum of $100,000 paid-in capital shall be allowed.

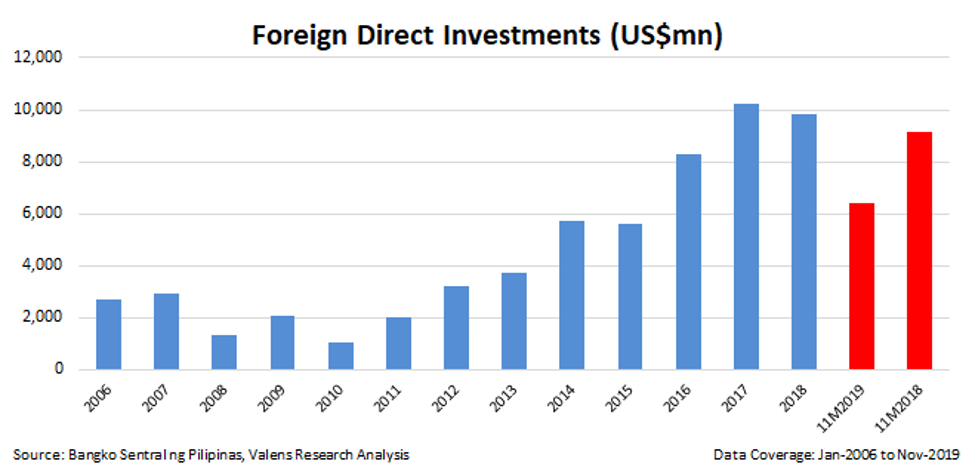

In the last 11 months of 2019, net inflows decreased by 30% to US$6.4 billion from the US$9.2 billion level posted in the same period in 2018.

The decline in net inflows was driven by the concerns over the global economic outlook that continued to curb FDI as investor confidence remained muted.

To spur global interest in long-term investment in the Philippines, Philippine lawmakers approved House Bill 300 last September 9, 2019, amending two provisions of the Foreign Investments Act (FIA) of 1991.

The provisions remove the ‘practice of professions’ from the foreign investment negative list and the reduction in the mandatory direct local hires by foreign investors.

Many Filipino workers could gain new skills and enhance their skill sets to be more competitive domestically and internationally, since the first amendment will make the Philippines more attractive to foreign skilled professionals.

The second amendment enables foreign investors to take full ownership of their small and medium-sized enterprises (SMEs) as long as they meet and follow the requirements.

Additionally, the Philippine lawmakers amended the Public Service Act to open other public utility sectors to foreign investors, such as telecommunications and transportation.

Furthermore, they introduced Corporate Income Tax and Incentives Rationalization Act (CITIRA), which will gradually reduce corporate income tax and rationalize specific tax incentives.

Our previous Monday Macro Report on Philippine corporate profitability emphasized that return on assets (ROA) of Philippine companies as a whole is expected to remain at current 6% levels based on Uniform Accounting. This is at the same level as global corporate averages.

Another thing we highlighted in that report is in order to justify the 24x Uniform P/E of the Philippine stock market, Philippine companies must improve their profitability without foregoing growth.

The Philippine government is expecting that the revisions and amendments mentioned above will contribute to the country’s growth. Those will hopefully help the Philippines become more globally competitive in terms of incentives given to investors who place their money in the country.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com