MONDAY MACRO: Philippine corporations have been more cost- and asset-efficient than as-reported metrics would suggest

Using Uniform ROA, we concluded that the aggregate profitability of the major Philippine corporations in 2021 was actually much higher than what as-reported metrics indicate.

Today, we further break down the Uniform ROA ratio into two separate metrics to draw additional insights as to what specifically drove this recovery in corporate profitability last year.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

Previously, we discussed the aggregate profitability of the top 100+ PSE-listed companies in terms of their return on assets (ROA).

Aggregate Uniform ROA hit previous lows of 4% in 2020 due to the pandemic but has since rebounded to 6% in 2021. Much of that recovery is thanks to the government loosening pandemic restriction as well as enacting monetary and fiscal policies to support corporate growth.

While looking at the aggregate ROA already tells us a clear story of the Philippine corporate market’s profitability, we can further draw insights from analyzing the two components that make up the ROA formula—earnings margin and asset turnover.

Earnings margin, calculated by dividing net income by revenues, is a profitability ratio that measures how efficient a company is at handling costs.

Businesses can increase margins by increasing revenues or reducing costs—or both. Generally, increasing revenues would entail additional marketing or advertising costs. Reducing costs, on the other hand, is typically done by decreasing or shifting to lower-cost supplies, and reducing labor or wages.

The second part of the question, asset turnover, is calculated by dividing revenues by total assets. This ratio is an indicator of how efficient the company is with using its assets to generate revenues.

A low asset turnover ratio suggests that the business may be having issues with inventory management, excess production, or too many investments in fixed assets that only marginally contributes to additional revenues.

That is not always the case, however, as some industries like oil and gas and real estate are highly asset-intensive and consequently earn lower asset turns.

Overall, the highest-quality companies are the ones that are both cost- and asset-efficient. Can we say the same for the Philippine corporate market as a whole?

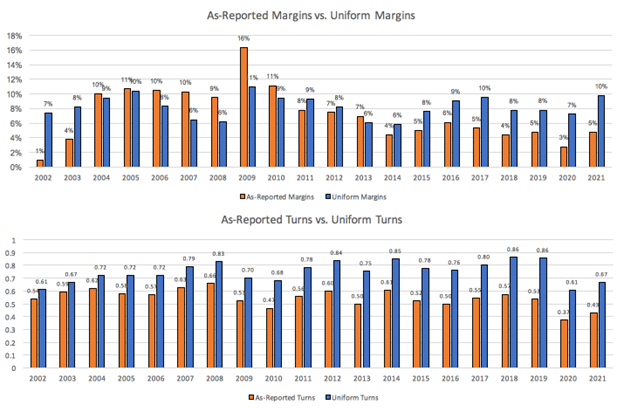

Coming from 9%-11% levels in 2004-2008, as-reported margins peaked at 16% in 2009 before subsequently returning to previous highs of 11% in 2010. Since then, however, as-reported margins have fallen to 7%-8% from 2011-2013, before fading to just 3%-6% through 2021.

Meanwhile, as-reported turns have been less volatile, ranging from 0.5x-0.7x from 2004-2019, before fading slightly to lows of 0.4x through 2021.

However, when removing the accounting distortions, both metrics have actually performed better than perceived. This is especially true for the aggregate asset turns of Philippine corporations, where balance sheets are incorrectly filled with excess cash, goodwill, and other items unrepresentative of the firm’s true operating assets.

While Uniform margins have been lower than as-reported margins from 2004-2010, it has since surpassed those levels in the years following. Specifically, Uniform margins have actually ranged from 6%-10% and not 3%-8%.

Also, it’s worth noting that corporations have taken efficient cost-cutting measures in 2020, with Uniform margin only falling to 7% from previous levels of 8%. These businesses have continued to be cost-efficient, with Uniform margin improving to previous highs of 10% in 2021.

Meanwhile, Uniform Accounting indicates that corporations have actually been more asset efficient, with Uniform turns ranging from 0.6x-0.9x and not 0.4x-0.7x.

That said, the decline in Uniform ROA in 2020 can be attributed predominantly to a decline in Uniform turns and a slight decline in Uniform margin. Companies continued to operate with the same asset base but were faced with lower revenues due to the massive decline in demand, leading to the inefficiency.

Furthermore, the Uniform ROA recovery in 2021 was driven by a significant improvement in Uniform margins. As mentioned, businesses have continued to be cost-efficient while revenues improve as operational restrictions loosen.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com