MONDAY MACRO: The valuation of the PH stock market is slightly above historical averages, but is still lower than you may think

The PSEi surpassed 7,000 this July for the first time since February 2021. Absent any black swan event, it seems unlikely for the stock market to repeat and fall below 6,200 again, given today’s better macro situation and our understanding of each company’s FY 2020 and Q1 2021 results.

That said, valuation levels suggest that the Philippine stock market may currently be overbought, but still lower than as-reported metrics suggest.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

In recent Philippine Markets Daily articles, we’ve talked a lot about the importance of Uniform ROAs. While these are crucial to any stock investment analysis, valuation metrics are equally significant.

A company can have high Uniform ROAs with huge upside, but still be a bad stock. This is because the market may have already priced in the current and future performance of the company.

Even worse, the stock can be overbought and trade well above its fundamental value, warranting a decline in its stock price.

There are a lot of valuation metrics for investors to look at, and one of the most common is the price-to-earnings (P/E) ratio—simply a measure of the company’s market capitalization relative to its most recent earnings.

A company with a P/E ratio higher than the market or industry average is said to be overvalued, while a lower-than-average P/E is said to be undervalued.

A key weakness of the standard P/E ratio we see on most financial databases is that it doesn’t directly price in a company’s future growth, which investors tend to do. So we might see companies that look like they’re too expensive because the stock price includes the growth potential investors are expecting.

On the other hand, we might see P/E ratios that look inexpensive because despite having higher earnings for the year, investors do not expect that growth to continue.

As a result, it’s much better to use a company’s projected earnings next year in the denominator, called the forward P/E ratio.

Using market cap as the numerator also has its inaccuracies. The stock price only represents the value of the company’s outstanding shares, not of the entire business.

When companies acquire assets, they don’t just use equity to finance those transactions; some assets are acquired through debt.

Moreover, when acquiring a business, the acquirer also takes on the target’s debts. As such, enterprise value provides a more accurate picture as it represents the theoretical price one would have to pay to buy the entire company.

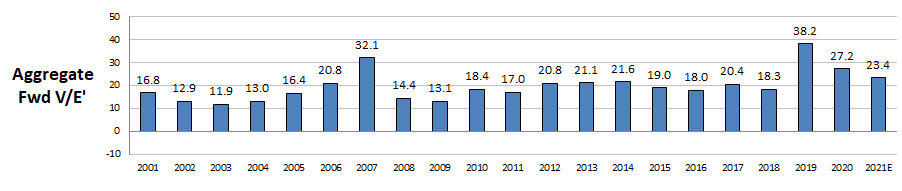

This is why in Uniform Accounting, the Uniform P/E (or Fwd V/E′) represents the Uniform enterprise value of the company relative to its Uniform earnings for the next period.

The aggregate Fwd V/E’s of companies listed on the Philippine Stock Exchange (PSE) have ranged from 11.9x to 38.2x since 2001, with an average of 19.6x. It reached its historical high of 38.2x in 2019 as a result of the earnings collapse in 2020 due to the coronavirus pandemic.

The aggregate Fwd V/E’ currently sits at 23.4x, slightly above its historical average. This implies that the Philippine stock market is close to being overvalued, unless the succeeding quarters lead to an upward revision in earnings forecasts.

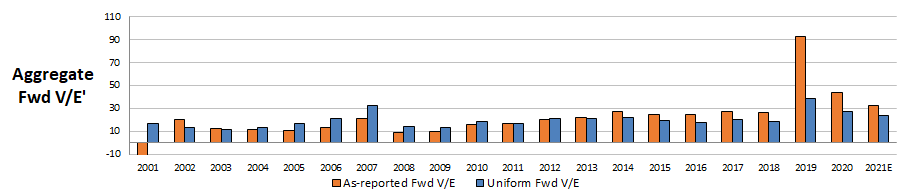

However, when comparing against as-reported metrics, valuations appear substantially more overvalued than reality. As-reported Fwd V/E’ peaked significantly higher in 2019 at 93.1x.

In addition, as-reported Fwd V/E’ is currently at 32.9x, materially higher than Uniform Fwd V/E’ of 23.4x.

As-reported metrics overstate the ratio because of how Philippine Financial Reporting Standards (PFRS) distort earnings. For these PSE-listed companies, as a whole, the largest distortion comes from the accounting treatment of interest expense.

According to PFRS, interest expense can be classified as an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully only a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

In 2020, Philippine corporations spent more on interest expense than they earned in profits. The aggregate as-reported net income was PHP 192.9 billion, while a total of PHP 348.9 billion in interest expense was recorded.

Adding back interest expense, along with the many other necessary adjustments made by Valens, leads to a much higher aggregate Uniform earnings of PHP 487.4 billion and a significantly lower Fwd V/E’ ratio.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com