MONDAY MACRO: There’s a fair amount of optimism surrounding corporate and economic growth, but certain macro headwinds continue to be a problem

This primary indicator of the Philippines’ economic health continues its upward growth trend in the first quarter of 2022. While the government is fairly optimistic about a strong economic recovery this year, there are multiple headwinds that could dampen otherwise robust growth.

Today we’ll be talking about the drivers of the upward trend, the headwinds the country is currently facing, and how this indicator relates to aggregate corporate profitability.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

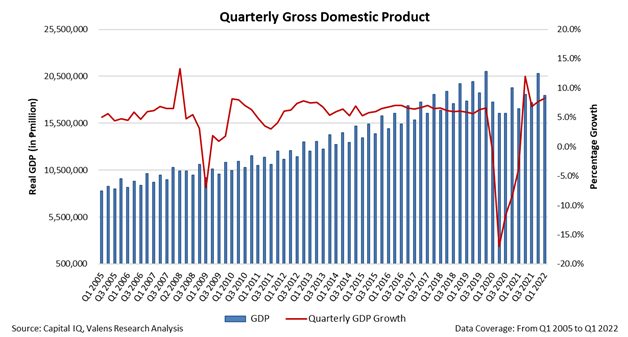

Philippine Gross Domestic Product (GDP) in the first quarter of 2022 expanded by 8.3%, which is an inflection from the year-ago quarter period contraction of 3.8% and is an acceleration from the revised 7.8% growth in the previous quarter.

We can further break down the components of this growth by using the expenditure approach of accounting for GDP. Under this method, total GDP is defined as the total of consumer spending, business spending, government spending, and net exports for the period.

Household consumption is the largest contributor, accounting for about three-fourths of the country’s GDP growth during the quarter. Consumption growth was 10.1% year-over-year, higher than the 7.5% posted in the previous quarter.

The other components of GDP had positive growth as well. Business investments grew 20% year-over-year, while imports and exports went up by 15.6% and 10.3% during the same timeframe, respectively.

Government spending, on the other hand, experienced slower year-over-year growth of only 3.6% due to the election spending ban.

The growth in GDP is driven in large part by macro tailwinds such as the election campaign spending, as well as the downgrading of quarantine restrictions from Alert Level 3 to Alert Level 1 which allowed businesses to operate at full capacity.

Overall, this is an optimistic indicator that the economy may fall within the annual GDP growth target range of 7%-9%.

That said, the economy still has to hurdle over major external and internal headwinds to stay on track.

The conflict between Ukraine and Russia continues to pressure the external oil supply, causing oil prices to remain at elevated levels. Furthermore, the U.S. monetary policy normalization is likely to cause depreciation pressure on the peso.

As one of the country’s main trading partners, China’s economic slowdown is also one to watch as it may dampen local growth due to disrupted import and export activities.

Lastly, inflation remains to be a significant threat as it weakens the consumers’ purchasing power. Considering that household consumption is the predominant GDP growth contributor, this is one area the government should be reasonably focused on.

Aggregate Corporate Performance and GDP

The largest Philippine corporations are a significant contributor to the total economic output of the country. Therefore, it might be useful to evaluate the forecasted performance of the corporate market to see where the economy is headed.

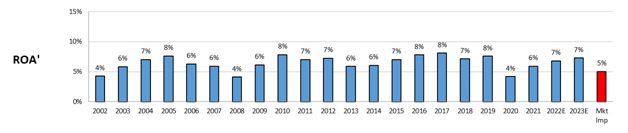

Currently, at a market implied ROA of 5%, investors are pricing in pessimistic assumptions for corporate growth.

It seems that they are expecting inflation to moderate demand for goods and services. Furthermore, they may be factoring in increased interest rates to ease higher inflation, which could discourage corporate borrowing and, consequently, investments for growth.

Analysts, on the other hand, are expecting aggregate corporate Uniform ROA to improve from 6% in 2021 to 7% through 2023, which is in line with the government’s higher target GDP growth rate. Analysts are also likely expecting pent-up demand from lockdown restrictions to outweigh decreased demand from macro pressures.

Barring any more restrictions on business operating capacity, and if the government can keep macro headwinds under control, it is likely that forecasts for higher corporate profitability and higher annual GDP may be achieved.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com