MONDAY MACRO: This credit quality indicator remains at elevated levels, but is nothing investors should be worried about

Major macroeconomic headwinds such as unemployment and lower overall demand brought by the pandemic meant that consumers and businesses had lower overall cash flows. This meant that borrowers, especially the smaller ones, have had a difficult time repaying their loans on time.

Banks may tighten their lending capacity if unpaid loans rise to unmanageable levels. With that, we turn to this indicator to measure how much money banks are likely to lose due to soured loans and gauge their willingness to lend going forward.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

COVID cases are now finally at low levels last seen in the early stages of the pandemic. About 60% of Filipinos have been fully vaccinated, and the government has begun relaxing quarantine restrictions as well as increasing outdoor establishments’ capacities.

Due to the upswing in demand from the return of foot traffic, businesses seem to be more optimistic about the recovery and growth prospects of the economy—the Business Confidence Index would confirm as much.

Looking at the current growth trajectory of C&I and MSME loans would also tell the same story. C&I loans are at new highs and MSME loans have seen increasing demand and growth rates, both of which are indicative of a bullish outlook and a greater willingness and capacity to invest in growth.

Loans play a significant role in both consumer spending and business operations, as well as the broader growth of the economy. Consumers and businesses use loans to finance their expenditures and expand operations for the latter, which should lead to increased aggregate output.

That said, taking on loans carries a certain level of credit risk. There are certain instances when borrowers are not able to pay the principal or interest on time. However, it’s the lending institutions, such as banks, that are likely to be more impacted by these defaults.

So, in order to assess the quality of banks’ credit profile reviews, as well as their willingness to lend more cash in the future, it’s useful to look at the Gross Non-Performing Loans (NPL) Ratio.

NPLs (or bad loans) are principal amounts or interest that have been unpaid for ninety (90) days from the date of the contract. In addition, loans will also be considered as such when existing accounting standards classify them as impaired.

An increasing NPL ratio indicates that the quality of loans is worsening and implies a greater risk of loss for banks. During economic recessions, especially—like the most recent one caused by the pandemic—NPLs tend to increase as tight economic conditions make it more difficult for people and businesses to pay their loans on time.

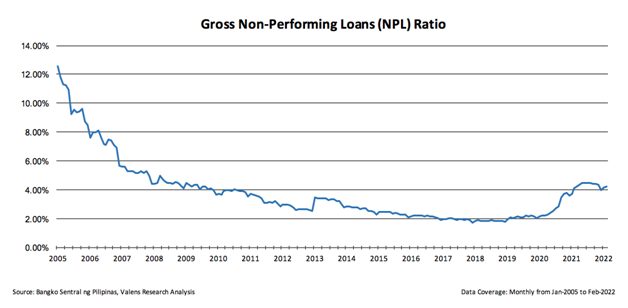

The NPL ratio began to rise during the onset of the pandemic, increasing from 2% levels in early 2020 and peaking at 4.51% in July 2021, a 13-year high.

Since then, the NPL ratio has stabilized at around 4% levels. Most recently, the country recorded NPLs of about PHP 473 billion in February 2022, a 9.6% increase from the previous year and a 2.4% growth from the month prior.

Despite the NPL ratio rising to elevated levels over the past decade, this is still far below the double-digit NPL ratio that the country saw during the Asian financial crisis and most of the early 2000s.

That said, the Bangko Sentral ng Pilipinas (BSP) projects that the NPL ratio of Philippine banks may reach a high of 8.6% this year. This could adversely impact businesses’ growth plans, especially the smaller ones, as borrowing becomes more difficult and expensive as banks become more reluctant to lend.

The BSP is optimistic, however, that the Financial Institutions Strategic Transfer (FIST) Act may help reduce NPLs and lower the ratio.

The FIST Act aims to strengthen the financial sector by facilitating the transfer of banks’ non-performing assets (NPAs) and NPLs to specialized FIST corporations. These corporations then help banks with the collection or disposal of NPLs and NPAs, enabling them to ultimately extend credit to more sectors of the economy.

Overall, with the NPL ratio rising to elevated levels, and even projected to double this year, it is still highly manageable considering banks’ evolving credit management systems and the FIST Act.

Furthermore, while this may be a useful indicator, it is not the end-all be-all of credit measures. It’s still important to look at other larger factors such as interest rates and overall demand that are likely to play more significant roles in banks’ willingness to lend.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com