MONDAY MACRO: Uniform Accounting reveals near-term contraction as the pandemic is seen to set off Uniform earnings back by 2% this year.

The Philippines was considered a rising economic powerhouse due to its favorable demographics and high consumer spending. It was one of the fastest-growing countries in Asia last year, enjoying an average of 6.4% GDP growth rate in the last three years.

However, the coronavirus pandemic derailed our current economic trajectory, with businesses now struggling to perform day-to-day operations on top of encountering sales generation difficulties.

To gain insights on near-term GDP growth through Uniform Accounting lenses, below is our analysis on earnings power for 2020 using our Performance and Valuation Prime Chart.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

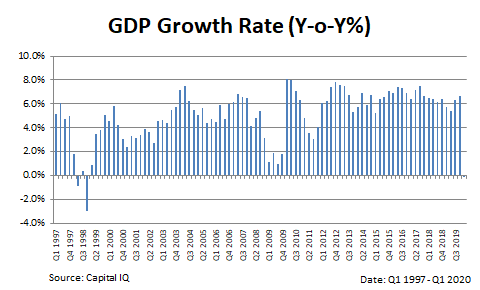

The Philippine economy experienced its first contraction in more than two decades in Q1 2020 due to the pandemic. Even when the global economy suffered during the 2008 financial crisis, the Philippines still managed to record positive GDP growth at a 1.8% rate in 2009.

When the global economy began its recovery in 2010, Philippine GDP growth surged to 8.1% in Q1 2010 and ended the year with a 6.3% GDP growth.

In 2011, GDP growth slowed down to an average rate of 3.9% pulled by limited government spending and export weakness. Since 2012, however, GDP growth levels were sustained at above 5% levels.

The last time the Philippines recorded an economic contraction was during the 1997 Asian Financial Crisis, a 0.5% contraction in 1998. Economic growth returned quickly a year later, with the country showing 3% annual GDP growth.

The Philippine GDP shrinking by 0.2% in Q1 2020 is concerning since COVID-19 restrictions imposed on most businesses started only in mid-March.

Travel, dining, and entertainment limitations, among others, were implemented during the 3-month quarantine period. Businesses had limited revenues and consumers had little spending power as a result of being temporarily unemployed.

Since most of the quarantine period falls in April to June, we are likely to see even worse results for Q2 2020.

Moreover, the country’s number of coronavirus cases continues to increase weekly. As long as these numbers do not fall to levels that show the coronavirus pandemic is under control, concerns about further economic contractions are understandable.

Most financial and research institutions are estimating negative GDP growth for the Philippines in 2020. Fitch Ratings goes so far as to forecast 4% shrinkage while median estimates are for GDP to contract by 1%.

On the other hand, prior to Q1 2020 data release, the Asian Development Bank believes that there are still enough growth catalysts in the Philippines for a 2% GDP growth to be possible in 2020.

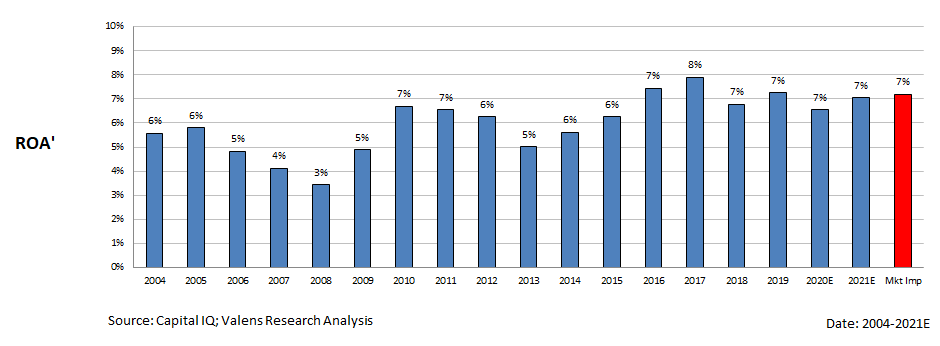

When we take these expectations into account and look at financial statements of the largest companies in the Philippines, what we see is that despite an impending recession, aggregate return on assets (ROA) in the Philippines will still remain above the cost of capital.

These Philippine companies have conservative enough balance sheets to avoid any bankruptcies or credit defaults, as we discussed in our June 1st Monday Macro report. Uniform Accounting shows that liquidity is not a near-term problem.

Performance and Valuation Prime Chart: Philippine Aggregate

The Philippine PVP chart above reveals that analysts still believe that returns will remain at 7% levels, as the market implied ROA shows. This is in line with what Uniform ROA shows.

Uniform earnings, the numerator of the ROA metric, is expected to decline by 1.8% in 2020, resulting in an expected 6.5% Uniform ROA. This is down from an ROA of 7.3% in 2019, but still above cost of capital. In 2021, this is expected to recover to 7.1%.

Investors and analysts are optimistic about near-term prospects despite the current economic environment, while research institutions have a generally more pessimistic outlook.

Fortunately, this current economic turmoil is not credit-driven, which means the economy’s swift recovery is expected. As we have seen historically, credit-driven recessions have a lot more inherent problems that need to be resolved before economic growth kicks back in.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com