PH Monday Macro: Philippine economic prospects are getting clouded by expectations

When trying to project how an economy will perform, it’s important to look at different indicators. There is no single indicator that will give us the best picture of an economy’s health.

Looking at just a handful won’t always work. Sometimes, these could make sense in one period, yet leave investors more confused than ever in another period when the indicators contradict each other.

We are currently seeing some inconsistent messages from Philippine economic measures. Today, we take a look at the disparity and see what these indicators are trying to tell us.

Philippine Markets Newsletter:

The Monday Macro Repor

Powered by Valens Research

One component of the GDP calculation is business investments. Business investments are a variable in the formula because part of these firms’ capital go into purchasing goods and services to expand their business.

These business expenses are then used to provide their own goods and services for other businesses or consumers. Consequently, the higher volume of goods and services being produced and sold, the higher GDP is.

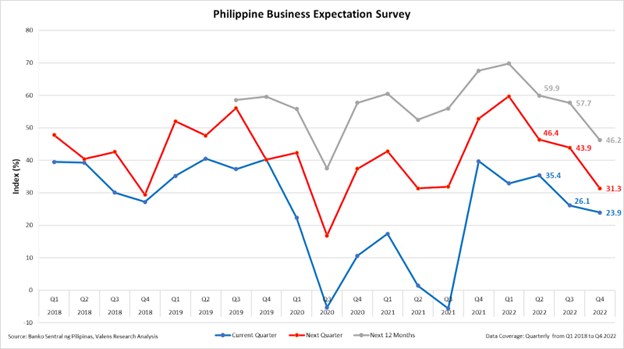

In consonance, business investments can be a barometer to gain insights into the future growth of an economy. Though how can we predict how much businesses are going to invest? The answer is through business expectations.

As shown in the graph, expectations plunged when the pandemic hit mid-year 2020. This was followed by optimism in the first quarter of 2021, though it fell right back down in the next quarter, before ending the year largely more optimistic for the next quarter and the next 12 months.

Since then, business expectations have been deteriorating. In the BSP quarterly report, the central bank indicated that businesses are becoming less optimistic due to the recent high inflation print, peso depreciation, decelerating consumer demand, an upward trend of raw materials, and higher interest rates.

These sentiments are consistent with consumer confidence that show people are currently becoming more concerned about the economy.

Taking these two forward-looking indicators into consideration, one might be confused as to why the Philippines is showing strength in other indicators such as GDP. The country even recorded its fastest annual growth in over 40 years.

A reason for this supposed disconnect is the economic lag between monetary action and economic response.

It takes time for monetary policy to ripple through the economy. When the Philippines entered a recession in 2020, the BSP (Bangko Sentral ng Pilipinas) shifted its monetary stance to crisis intervention. Two policy measures were to inject liquidity into the market system and cut interest rates to stimulate the economy.

Even before the pandemic, the BSP had already been cutting rates in 2019 to manage the historically high interest rates in the country.

Then in February 2020, in anticipation of the adverse effects of the novel coronavirus outbreak months before, the central bank accelerated its rate reduction program. It continued with its accommodative path with succeeding cuts when the virus turned into a pandemic a month or so later.

The strong rebound we saw these past quarters was an effect of the loose monetary policy, taking almost a year to materialize and reflect the effects of the rate cuts and relief stimulation.

Furthermore, such expansionary policy, although beneficial in the short-run, causes inflated prices because there is more money supply circulating in the system. If the money supply rises with economic output remaining the same or unable to match the level of money supply, this extra cash will cause the value of the currency to drop, resulting in lower purchasing power.

To tame inflation, the BSP announced in the second quarter of 2022 that it will be raising the overnight reverse repurchase facility interest rate. The anticipation of persistent and increasing inflation pressures pressed the central bank to pivot into a restrictive policy. As a result, business expectations started to sink.

It will take time until we see how the economy will respond to the reconfiguration from an accommodative measure into a restrictive policy. This is why we are looking at business expectations to get a glimpse of how the economy will perform.

Business expectations are a leading indicator, while GDP figures are a lagging indicator. This is why it is important to look at and examine a variety of indicators to provide us with a comprehensive understanding of the market.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com