Philippine e-commerce is taking off. It could pay off for you to see how profitable e-payments can REALLY be (Uniform earnings power of 21%! Not 3%).

E-commerce platforms like Lazada and Shopee have become extremely popular in today’s hustle culture.

A seller in Baguio can easily connect with a buyer in Cebu. A stay-at-home parent can instantly become a distributor without worrying about logistics. A small-time manufacturer can conveniently commission a group of salespeople.

Even large retailers are making the shift online.

Revenue from e-commerce is expected to grow at an annual rate of 10% over the next few years in the Philippines. With this growth comes the need for secure alternative payment schemes other than credit cards. There’s GCash, PayMaya, Coins.ph, and even 7-Eleven’s CLiQQ.

It makes sense to see what this global company looks like, especially since it’s one of the most widely used alternatives for secure online purchases.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In 2019, it is estimated that e-commerce sales accounted for 14.1% of all retail sales globally.

For a transaction to be considered e-commerce, the buying and selling should have been done online, regardless of how the payment was made. Cash-on-delivery payments on purchases made online are still considered an online sale.

Since brick-and-mortar stores are too capital-intensive and have limited customer reach, more and more sellers have opted to establish a bigger presence online and spend on various social media platforms, since these are much more cost-effective than traditional marketing and advertising.

The convenience of shopping online has attracted a large and growing following worldwide, with some estimates putting global e-commerce sales at 22% of total retail sales by 2023.

In the US alone, e-commerce has been growing at a range of 14%-18% each year, contributing somewhere between 10% to 15% of total retail sales.

In China, the rise of giants like Alibaba and JD has resulted in around $680 billion in online retail sales in just the first half of 2019, an 18% growth from the first half of 2018. This is estimated to account for 20% of total retail sales in China.

In the Philippines, e-commerce is still rather small as a percentage of total retail sales at just 2%, but it is expected to reach 5%-7% in the next few years.

This growth in the e-commerce arena might not have been sustainable had there not been a secure way for both merchants and buyers to process payments online.

China’s large online market is evidence that the digital payment methods are an effective payment method. It brings shopping at the tip of your fingers, making it even more convenient.

As the rest of the world begins incorporating digital wallet options to their online stores, one company has been in this business for nearly 20 years.

PayPal started as a money transfer service in 1999. It quickly became the choice payment method of online shoppers at the time, especially on eBay.

In 2002, eBay acquired PayPal, recognizing the tremendous value-add this was to their online marketplace platform.

In 2015, eBay spun off PayPal but continued to use it as their preferred payment system.

As an independent and now purely payments processing company, PayPal was able to focus on strengthening its security features and innovating to adapt to the fast-changing online environment.

Investors recognized this value, with the stock now up over 200% since its IPO in 2015.

PayPal’s P/E is in line with Uniform Accounting metrics

PYPL:USA currently trades at historical highs relative to Uniform earnings, with a 35.4x Uniform P/E (Fwd V/E’).

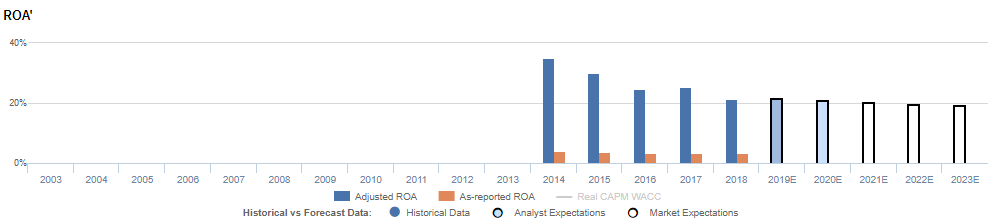

At these levels, the market is pricing in expectations for Uniform ROA to expand from 21% in 2018 to 24% by 2023, accompanied by 15% Uniform asset growth going forward.

Meanwhile, analysts have muted expectations, projecting Uniform ROA to sustain 21% levels through 2020, accompanied by 9% Uniform asset growth.

PayPal’s returns are far more robust than most investors think

PYPL has seen robust, but fading profitability. After reaching 35% levels after its spinoff from eBay, Uniform ROA fell to 21% in 2018, driven by competitive pressures and a growing balance sheet.

At these levels, the market is pricing in expectations for Uniform ROA to expand from 21% in 2018 to 24% by 2023, accompanied by 15% Uniform Asset growth going forward.

Meanwhile, analysts have muted expectations, projecting Uniform ROA to sustain 21% levels through 2020, accompanied by 9% Uniform Asset growth.

PayPal’s returns are far more robust than most investors think

PYPL has seen robust, but fading profitability. After reaching 35% levels after its spinoff from eBay, Uniform ROA fell to 21% in 2018, driven by competitive pressures and a growing balance sheet.

Meanwhile, Uniform asset growth has been consistently positive, ranging from 10%-70% each year since 2015, driven by the acquisitions of platforms such as iZettle, Paydiant,and TIO Networks.

As-reported metrics significantly understate PYPL’s profitability.

For example, as-reported ROA for PYPL was near 3% levels in 2018, materially lower than its Uniform ROA of 21%, making PYPL appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2014, as-reported ROA has remained at 3%-4% levels, while Uniform ROA compressed from 35% to 21% over the same timeframe, significantly distorting the market’s perception of the firm’s historical profitability trends.

PayPal’s earnings margins are in line with Uniform metrics

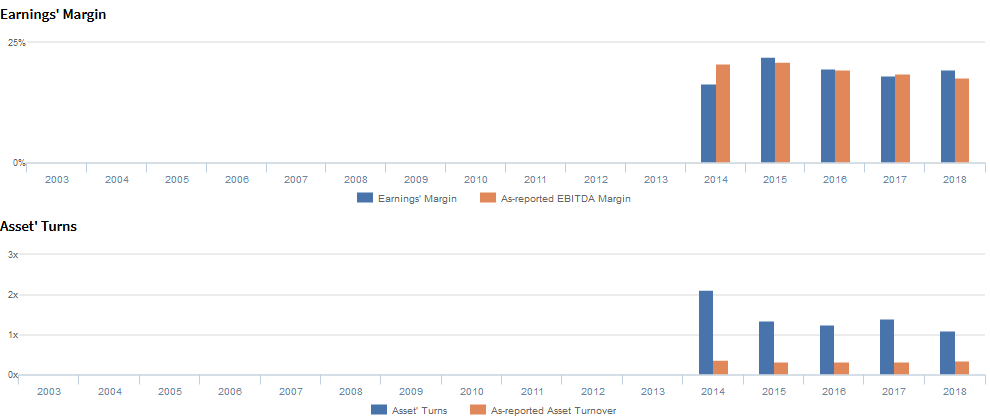

Trends in Uniform ROA have been mainly driven by trends in Uniform Asset Turns and, to a lesser extent, Uniform Earnings Margin.

After expanding from 17% in 2014 to 22% in 2015, Uniform Margins regressed to 20% in 2018. Meanwhile, after fading from 2.1x in 2014 to 1.3x-1.4x levels in 2015-2017, Uniform Turns fell again to 1.1x in 2018.

At current valuations, markets are pricing in expectations for a slight expansion in Uniform Earnings Margin, coupled with stability in Uniform Asset Turns.

SUMMARY and PayPal Holdings, Inc. Tearsheet

As our Uniform Accounting tearsheet for PayPal Holdings, Inc. highlights, the PayPal Uniform P/E trades at 35x, well above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of PayPal, the company has recently shown a 26% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, PayPal’s Wall Street analyst-driven forecast is a historically low growth of 15% into 2019, which then drops to a 10% growth in earnings in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $108 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of PayPal, the company would have to have Uniform earnings grow by 21% each year over the next three years.

What Wall Street analysts expect for PayPal’s earnings growth falls below what the current stock market valuation requires.

To conclude, PayPal’s Uniform earnings growth is above peer averages in 2020. The company has an above average earnings power, based on its Uniform return on assets calculation, compared with the 12% average earning power for US companies. Also, the company is trading at well above average peer valuations.

As for the Philippine e-payment firms similar to PayPal, it’s likely that they won’t look so good based on PFRS metrics as well. However, on a Uniform basis, they could be showing returns as strong as PayPal’s was in its early days.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing himself, Benjamin Graham.

Warren Buffett and Charles Munger of Berkshire Hathaway; David Sanford Gottesman of First Manhattan Co.; Walter Schloss of WJS Partners; William Ruane of Ruane Cuniff, Sequoia Fund; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; just to name a few.

Each of the great investors studied security analysis and valuation. They have applied this methodology to manage their multi-billion dollar portfolios.

But what sets them apart from everyone else who also uses financial statements and valuation to choose their investments? History.

These great investors don’t rely on as-reported numbers.

“… although accounting is the starting place, it’s only a crude approximation.” – Charlie Munger

“… the net earnings figure… it really is not representative of what’s going on in the business at all.” – Warren Buffett, Opening Remarks, the 2018 Berkshire Hathaway Annual Shareholders Meeting

“GAAP rules… I’ve warned you about the distortions. The bottom line figures… totally capricious. It’s really a shame.” – Warren Buffett, Opening Remarks, the 2019 Berkshire Hathaway Annual Shareholders Meeting

“Generally Accepted Accounting Principles are not truth or reality.” – Marty Whitman

Due to the multiple distortions and miscategorizations in GAAP and IFRS, investors are often unable to properly analyze companies in an apples-to-apples comparison.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS.

The goal of UAFRS is to create reliable and comparable reports of corporate financial activity.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company listed outside of Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s global company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

www.valens-research.com