Powering multiple plants across the country enabled this company to achieve a Uniform ROA of 10%, not 4%

A month ago, some parts of Luzon experienced a series of brownouts due to a massive increase in power demand.

This power generation company was able to use its large uncontracted power capacity as an opportunity to turn its business around. However, as-reported metrics show that it isn’t enough.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

A year ago, we discussed one of the largest conglomerates in the Philippines, Aboitiz Equity Ventures Inc. (AEV:PHL), which has major investments under its belt— particularly in power, banking and financial services, food, infrastructure, and land.

Today, we are going to dive deeper into its power generation business, Aboitiz Power Corporation (AP:PHL).

Incorporated in 1998, the company is AEV’s largest subsidiary, currently contributing 55% of its parent company’s total revenue. This unit is engaged in solar, oil, coal, hydroelectric, and geothermal operations.

Since its IPO in 2007, the company has been recording year-over-year sales growth. By 2010, Aboitiz Power was able to increase its revenues to P59.5 billion, which was a 157% increase from 2009. This jump is attributed to its coal operations, which increased the power supply to a level that is more than enough to meet expected demand.

However, in the succeeding years, the company’s profitability took a downward trend. This was most evident at the beginning of 2020 as a result of Aboitiz Power failing to contract the bulk of its capacity beforehand. In turn, the firm was subjected to spot price declines.

For this very reason, Aboitiz Power’s main competitors, such as First Gen (FGEN:PHL) and AC Energy, have surpassed the company in terms of earnings.

Recently, however, the island of Luzon experienced a series of power outages due to a massive increase in power demand, causing the National Grid Corp of the Philippines (NGCP) to signal a “red alert” for three consecutive days in the month of June.

Wholesale Electricity Spot Market (WESM) and Independent Electricity Market Operator (IEMOP) have stated that increased demand poses a threat to power supply since numerous corporations are nearing their maximum power capacity.

This could serve as a turning point for Aboitiz Power since the company has the opportunity to reclaim its previous earnings. Its uncontracted power capacity entails an excess on the company’s end.

This excess capacity will not only be able to satisfy increasing demand due to tight power supply, but it will also warrant higher prices in WESM when Aboitiz Power sells it. With this, the company has the possibility of surpassing the performance of its competitors.

Aside from the excess capacity, Aboitiz Power is also veering towards more power plant creation and expansion. Recently, the company has developed a new coal power plant located in Bataan and has set a number of renewable energy projects.

The company has scheduled its supercritical power plant in Bataan to go online in the middle of next year, with which Aboitiz Power aims to further increase its power capacity by developing more new plants, targeting 9,000MW in roughly 10 years.

Through the years, the company’s focus on increasing the number of its power plants has benefited the company’s earnings. It also helped combat the sharp decline of power generation demand during the pandemic.

However, the as-reported metrics of Aboitiz Power imply the company may not be adept enough at curbing the predicaments brought about by its large uncontracted capacity, with as-reported showing only below cost-of-capital levels in 2020.

In reality, Aboitiz Power’s continued focus on improving and increasing its number of power plants has actually produced above cost-of-capital returns.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense can be classified as an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully only a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2020, the company recorded a PHP 14.2 billion interest cost. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 19.7 billion net income and a 10% Uniform ROA, higher than its PHP 12.6 billion as-reported net income and 4% as-reported ROA.

Aboitiz Power’s earning power is stronger than you think

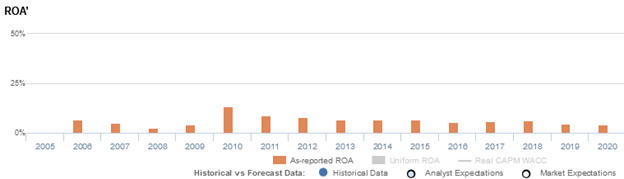

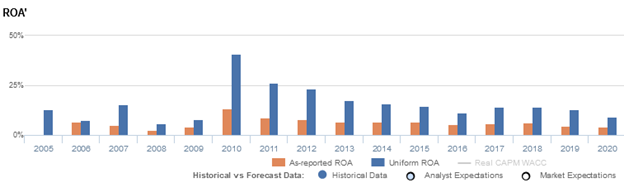

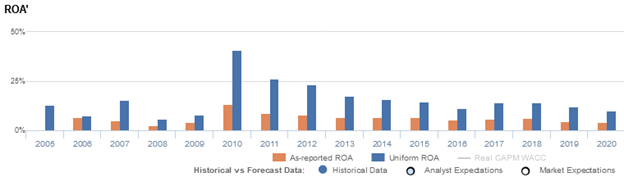

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Aboitiz Power’s profitability is weaker than what real economic metrics highlight in most years.

In reality, Aboitiz Power’s true profitability has generally been higher than its as-reported ROA except in 2020.

As-reported ROA expanded from 3%-7% levels in 2006-2009 to a high of 13% in 2010, before fading to 4% in 2020.

Meanwhile, after improving from 8% in 2006 to 16% in 2007, Uniform ROA compressed back to 8% in 2009, before rising to a peak of 41% in 2010. Then, Uniform ROA contracted to 11% in 2016, before rebounding to 14% levels in 2017-2018. Since then, Uniform ROA has declined to 10% in 2020.

Aboitiz Power’s earnings margin is weaker than you think

Volatility in Uniform ROA has been driven by trends in Uniform earnings margin.

As-reported margins expanded from a range of 18%-23% in 2005-2008 to a peak of 49% in 2010. It then contracted to 31% by 2014, and recovered to 36% in 2016. Thereafter, as-reported margins fell to 30% in 2019, before rebounding to 33% in 2020.

Meanwhile, after falling from 13% in 2005 to 5% in 2008, Uniform margins rose to a peak of 42% in 2010, before declining to 20% in 2014. Then, Uniform margins improved to 23% levels in 2016-2018, before contracting to 19% levels in 2019-2020.

As-reported metrics are making the firm appear to have better margins than real economic metrics highlight.

SUMMARY and Aboitiz Power Corporation Tearsheet

As the Uniform Accounting tearsheet for Aboitiz Power Corporation (AP:PHL) highlights, it trades at a Uniform P/E of 12.5x, below the global corporate average of 23.7x and its historical average of 15.3x.

Low P/Es require low EPS growth to sustain them. In the case of Aboitiz Power, the company has recently shown a 41% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Aboitiz Power’s sell-side analyst-driven forecast calls for a 127% EPS growth in 2021 and a 47% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aboitiz Power’s PHP 24.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 5% annually over the next three years. What sell-side analysts expect for Aboitiz Power’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

The company’s earning power is 2x the long-run corporate average. However, cash flows and cash on hand are below total obligations, while intrinsic credit risk is 320bps above the risk free rate. Together, this signals a high dividend risk and a moderate credit risk.

To conclude, Aboitiz Power’s Uniform earnings growth is way above its peer averages, and currently trades in line with its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com