Robots are taking over retail and this company is leading the charge, bringing in Uniform ROAs of 10%+ in the process

Self-checkout systems and self-service kiosks have risen in popularity among big-box retailers, restaurants, financial institutions, and other service-oriented businesses. The growth in cashless payments and pandemic-fueled concerns have only accelerated this trend further.

Benefiting from this tailwind is a company that’s in the business of providing the software and hardware necessary to power the self-checkout market.

While mediocre as-reported return on assets (ROAs) show that this company isn’t really benefiting that much, Uniform ROAs of 10%+ reveal that it captures enough of the growing market to make robust returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

“The future of grocery shopping” is how some people described Amazon’s cashier-less, shop-and-go grocery store, Amazon Go.

The stores are fully manned by AI technology that intelligently scans the products customers decide to purchase, and are then charged through their online accounts—all without having to get through a human cashier. The experience, as one analyst from RBC puts it, is like shoplifting… but legal.

Self-checkout has been a rising trend among other retailers such as Walmart, Kroger, and 7-Eleven, although the stores are not fully unmanned like Amazon Go.

One of the major reasons for companies investing in self-checkout capabilities is to increase customer satisfaction.

Having to wait in long lines can often cause customers to just leave and do their grocery shopping another day, or worse, go to a competitor whose lines and wait times are much shorter.

The growth in the self-checkout market is also fueled by another dominant consumer trend: cashless payments.

The use of cashless payment methods such as credit cards, debit cards, and payment apps continues to accelerate primarily because of its transactional ease and security.

You no longer need to carry large sums of money that may be easily stolen. Granted that going cashless does have its risks (i.e. getting hacked), cards and apps can easily be blocked, even remotely, and the transactions can be reversed.

Overall, thanks to the growing adoption of cashless payments as well as advancements in technology, the self-checkout market is poised to double its global market size from $3 billion in 2020 to about $8 billion by 2027.

One of the companies set to benefit from this tailwind is NCR Corporation (NCR).

NCR is the leading enterprise technology provider for the restaurant, banking, retail, and telecom industry. Specifically, the company provides end-to-end solutions for businesses, from point-of-sale and self-checkout kiosks and ATMs down to the mobile apps and data analytics software.

While a large chunk of NCR’s portfolio of products and services were developed through in-house R&D efforts, the company has also expanded this portfolio through strategic acquisitions.

A few of the company’s largest and most recent acquisitions include:

- Terafina – an omnichannel digital banking platform that provides account opening services, including fraud detection and know-your-customer capabilities

- Cardtronics – a provider of ATM and other financial kiosk products

- Stoplift – a computer vision system that detects retail theft, especially for those providing self-checkout services

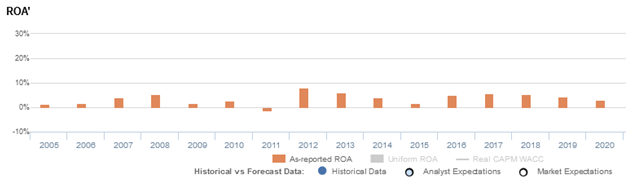

Since this company is able to ride on the tailwinds of “the future of grocery shopping” and beyond, one would expect this company to be earning considerable returns. However, NCR’s return on assets (ROAs) are well below cost of capital, declining from 8% in 2012 to just 3% in 2020.

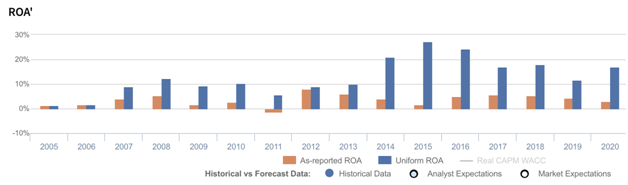

Uniform Accounting, on the other hand, paints a significantly different picture. Uniform ROA rose from 9% in 2012 to a peak of 27% in 2015 before declining to 12% in 2019. It has since recovered to 17% in 2020.

2020 is also an interesting data point. If you were looking at as-reported numbers, you’d think returns have fallen from the previous year, when in fact, it’s the opposite.

The pandemic accelerated the push for self-checkout and cashless systems as additional forms of social distancing. Without Uniform Accounting, investors would likely conclude that NCR’s business also suffered, as most companies did during the pandemic.

On a more specific note, the distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on NCR’s balance sheet.

In recent years, goodwill sits at about $2.8 billion, which sits at a little over a third of the company’s long-term assets, arising from acquisitions made to expand their products and services.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of NCR’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the opposite, with returns that are nearly 3x-13x greater.

NCR’s earning power is actually more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

NCR’s Uniform ROA has actually been higher than its as-reported ROA in the past fourteen years. For example, Uniform ROA was at 17% in 2020 while as-reported ROA was only at 3%.

Historically, NCR’s as-reported ROA has ranged from only -1% to 8% in the past sixteen years while Uniform ROA has ranged from 1% to 27% levels in the same timeframe.

Looking at the trend, Uniform ROA rose from 1% in 2005 to 12% in 2008, before fading to 6% in 2011. Thereafter, Uniform ROA expanded to a peak of 27% in 2015, before fading to 12% in 2019 and subsequently rebounding to 17% in 2020.

NCR’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Recent trends in Uniform ROA have been driven primarily by incremental improvements in Uniform earnings margin, coupled with stable Uniform asset turns.

Uniform margins rose from 1% levels in 2005-2006 to 7%-8% levels in 2007-2010, before falling to 4% in 2011 and subsequently rebounding to a peak of 14% in 2015. Thereafter, Uniform margins declined to 7% in 2019 before recovering to 10% in 2020.

Meanwhile, after improving from 1.0x in 2005 to 1.6x in 2008, Uniform turns contracted to 1.1x in 2013 and expanded to 2.1x in 2016. Since then, Uniform turns have faded to 1.8x in 2018-2020.

At current valuations, the market is pricing in expectations for a reversal of recent improvements in Uniform margins, accompanied by continued declines in Uniform turns.

SUMMARY and NCR Corporation Tearsheet

As the Uniform Accounting tearsheet for NCR Corporation (NCR:USA) highlights, the Uniform P/E trades at 39.2x, which is above the global corporate average of 23.7x and its historical Uniform P/E of 26.7x.

High P/Es require high EPS growth to sustain them. In the case of NCR, the company has recently shown a 65% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, NCR’s Wall Street analyst-driven forecast is an 86% EPS contraction in 2021 and a 1% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify NCR’s $47 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 6% annually over the next three years. What Wall Street analysts expect for NCR’s earnings growth is below what the current stock market valuation requires in 2021 but above its requirement in 2022.

Furthermore, the company’s earning power is 3x the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities and capex maintenance. Together, this signals an average credit risk.

To conclude, NCR’s Uniform earnings growth is below its peer averages, but the company is trading above average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com