Shop til’ you drop! This company developed a personalized platform that transformed online shopping and produced Uniform ROAs of 14%+

The unprecedented disruptions caused by the pandemic are forcing businesses globally to reshape their own strategies, challenging them to rapidly shift to e-commerce services in order to survive.

While other online platforms offer the more popular marketplace-style service, this company focuses on personalization and brand recognition through its main platform, enabling new businesses to build their own name without having to aggressively compete with other similar products.

Though as-reported data suggests that this strategy has not generated profitability for the company, Uniform Accounting shows that it actually helped improve returns from negative levels to current 14% levels.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Retail store closures and lockdown restrictions forced brick-and-mortar businesses to transition online. They’re hoping that this move would enable them to sustain their revenues while capturing untapped markets through new marketing strategies for the online space.

Since April, retail sales in the US were reported to have dropped 18% month-on-month, while online sales reached record highs of 30.7% as a percentage of total retail sales. Online retailers like Amazon (AMZN), eBay (EBAY), and Shopify (SHOP) have benefitted from this tailwind.

eBay’s marketplace-style service helps make the transition online easier. Essentially, it uses its auction-based website as an online marketplace to make transactions more convenient for buyers and sellers.

Amazon offers the same style of service, although while eBay focuses on auction sales, Amazon focuses on competitive retail sales.

The problem with this service is that many sellers are going to be offering the same products at more or less the same price on the same platform. You can type in “red sweater” on Amazon, for example, and a hundred different items from hundreds of sellers will appear.

Shopify poses a solution to this problem by adding a more personalized touch.

It’s an e-commerce platform designed to enable businesses to build and develop a more personalized brand by creating their own website domain. It provides its customers with a plethora of templates to work with to add to the customization process.

Furthermore, similar to other e-commerce platforms, Shopify has its own servers, simplifying the process of setting up an online shop without the need to purchase a separate server or software. Also, with its user-friendly interface, no knowledge on technical computer codes are necessary.

Shopify also lets its users expand into other sales channels such as Facebook, Instagram, and to any other website through its “buy button” feature—this embeds a buy button as an ad on any website, which would then lead to the user’s online site.

To further strengthen the users’ marketing and advertising capabilities, as well as expand their customer base, the platform allows the option of integrating partner apps such as Marsello (targeted marketing through texts and emails), Gift Box (customer rewards), and Justuno (customer data analytics) into their websites.

Finally, perhaps the most important feature Shopify has that differentiates itself from its competitors is its point-of-sale (POS) system. This lets users sell not just from their online stores, but through their physical stores as well.

The company can provide the necessary hardware such as barcode scanners and receipt printers, or the user can easily download the POS app on any iOS or Android device. With the POS, users can easily accept any mode of payment from the device they’re using.

As a subscription-based plan, Shopify is able to increase its client base by charging a small transaction fee that decreases as plan upgrades are made. This also enables the company to obtain more revenues as it grows.

Shopify’s target customers remain to be small and medium enterprises (SME) and lone entrepreneurs, with its main focus being brand strengthening. However, popular brands such as Nestle, Pepsi, and Unilever are also utilizing this platform, showing just how powerful its reach is.

Shopify’s focus on developing a strong brand recognition and personal user experience for its clients made the company distinguishable from its other competitors.

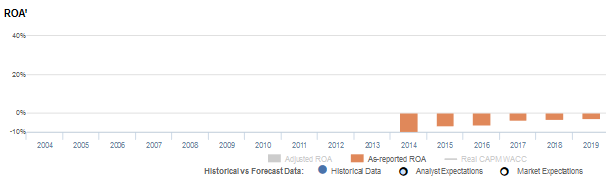

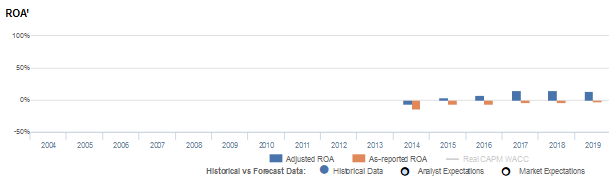

However, as-reported data makes it appear that this strategy has yet to generate profits for the company, with return on assets showing consistent negative levels through 2019.

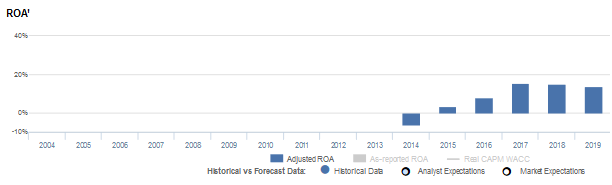

Although negative profitability is common for nascent businesses, in reality, Uniform Accounting actually shows the opposite, with Uniform ROAs inflecting positively in 2015 and rising to 14% in 2019.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In the case of Shopify, the company has a substantial excess cash balance currently in the amount of $1.8 billion, generated as proceeds from its IPO. This materially overstates the company’s cash balances, inflating the asset base and causing profitability to look weaker than it really is.

Adjusting for excess cash, we can see that Shopify’s actual returns have inflected positively from -6% in 2014 to 14% in 2019, while as-reported metrics remained negative in the same time frame.

Shopify’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Shopify’s Uniform ROA has actually been higher than its as-reported ROA in the past six years. For example, as-reported ROA was -3% in 2019, but its Uniform ROA was actually materially higher at 14%.

Through Uniform Accounting, we can also see that the company’s true ROAs have actually been positive. Shopify’s Uniform ROA has ranged from -6% to 16% in the past six years while as-reported ROA ranged only from -14% to -3% in the same timeframe.

Shopify’s profitability is driven by trends in Uniform earnings margins and Uniform asset turns

Shopify’s profitability has been driven by trends in Uniform earnings margins and Uniform asset turns.

From 2014-2015, Uniform earnings margins inflected positively from -5% to 2%. It then gradually expanded to a peak of 9% in 2017, before subsequently compressing to 8% levels in 2018-2019.

Meanwhile, Uniform turns gradually improved from 1.3x in 2014 to 1.9x in 2016, before stabilizing to 1.7x to 1.8x through 2019.

At current valuations, markets are pricing in expectations for both Uniform margins and Uniform turns to continue expanding.

SUMMARY and Shopify Inc. Tearsheet

As the Uniform Accounting tearsheet for Shopify Inc. (SHOP) highlights, Uniform P/E trades at 210.8x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Shopify, the company has recently shown a 31% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Shopify’s Wall Street analyst-driven forecast is a 338% EPS growth and 5% EPS shrinkage in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Shopify’s $1,053 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 118% each year over the next three years to justify current prices. What Wall Street analysts expect for Shopify’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows are 7x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Shopify’s Uniform earnings growth is above its peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com