Thailand’s largest beverage company is brewing Uniform returns that are almost thrice the as-reported!

Today’s company is a product of a massive business consolidation in Thailand. Its growth plans have also included acquisitions throughout Southeast Asia.

However, as-reported metrics do not reflect the company’s real profitability, making it look like a weaker business than it really is. Uniform Accounting shows that this company’s Uniform return on assets (ROA) is actually stronger than what the market thinks.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

The terms “business acquisition” and “business consolidation” are often mistakenly used interchangeably. Although both are types of business combinations, there’s a large difference between the two.

In one of our previous articles, we discussed acquisition as a strategy for companies, like CITIC Telecom, to obtain growth. To recall, this means that a company buys another company to grow inorganically. After an acquisition, the target company ceases to exist, as it becomes a part of the buying company.

Meanwhile, business consolidation is when different companies combine to form a separate larger entity. It usually involves more than two companies, as opposed to business acquisition that only involves the buyer company and the target company.

Moreover, in business consolidation, all participating companies are dissolved to create a larger corporation, usually to improve operational efficiency.

Today’s company originated from a 2003 business consolidation of 58 beer and beverage companies. It also engages in business acquisitions as part of its strategy to seek growth.

Thai Beverage Public Company Limited (ThaiBev) was founded by Charoen Sirivadhanabhakdi with a vision of combining leading beer and spirit businesses into a single holding.

Since the Stock Exchange of Thailand (SET) prohibits the listing of alcohol-related stocks, Thailand’s largest alcoholic beverage manufacturer and distributor was instead listed on the Singapore Exchange (SGX).

One of ThaiBev’s best known brands is Chang Beer, which controls the second largest slice of Thailand’s beer market, after Singha beer. Aside from Chang Beer, the company also has spirit brands that are recognizable nationwide like Ruang Khao, SangSom, Mekhong, Hong Thong and Blend 285.

Through the consolidation, ThaiBev was able to obtain a strong production and sales & marketing capacity, which allowed the company to compete with foreign liquors at lower costs.

Moreover, the company continuously made acquisitions after its consolidation. Aside from its leading alcoholic beverages, ThaiBev also ventured into non-alcoholic beverages and snacks.

In 2008, the company acquired Oishi Group Public Company Limited, a Thailand-based company that specializes in ready-to-drink green tea products and Japanese restaurants.

Additionally, to become one of Asia’s largest beverage companies, ThaiBev not only acquired beverage companies from Thailand, but also ventured outside the country, particularly in Southeast Asia.

Its Southeast Asian expansion began with its 2012 acquisition of Fraser and Neave (F&N), a Singaporean food and beverage conglomerate. ThaiBev also bought stakes in Myanmar’s biggest player in its whisky market, Grand Royal Group, in 2017. In the same year, ThaiBev also acquired Sabeco, the producer of Vietnam’s famous Saigon Beer.

With these continued expansion efforts through acquisitions, ThaiBev has broadened its presence and grown its customer base.

Since alcoholic beverages virtually sell themselves, one would expect ThaiBev to have robust profitability.

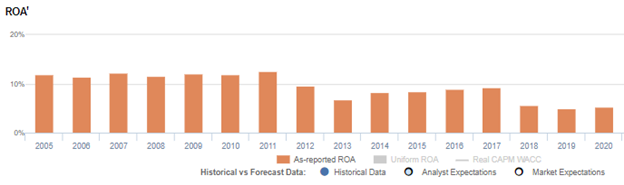

However, as-reported metrics tell us otherwise, showing returns falling from 7%-10% in 2012-2017 to just below cost-of-capital levels in 2018 to 2020.

Looking at these numbers, it seems that ThaiBev’s acquisition strategies aren’t really working for the company’s benefit. However, Uniform Accounting shows an entirely different story.

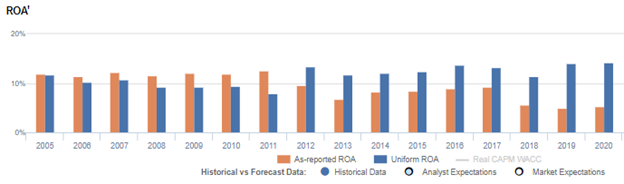

The company’s acquisition strategy actually resulted in much more robust returns than what as-reported metrics imply. Since 2012, its Uniform ROA has been stronger than its as-reported returns, with Uniform ROA currently at 14%, higher than as-reported ROA of 5%.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on ThaiBev’s balance sheet.

The company’s goodwill currently sits at about THB 152.9 billion due to its many acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the true strength of ThaiBev’s profitability. After adjusting for goodwill and other necessary adjustments, we can see that the company doesn’t actually have weak, below cost-of-capital performance. In reality, its Uniform ROA is 3x stronger than what as-reported metrics show.

Thai Beverage Public Company Limited’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

ThaiBev’s Uniform ROA has been higher than its as-reported ROA in the past nine years. For example, Uniform ROA was 14% in 2020, while as-reported ROA was only 5%.

The company’s Uniform ROA for the past nine years has ranged from 11% to 14%, while as-reported ROA has ranged only from 5% to 9% in the same timeframe.

Specifically, Uniform ROA fell from 12% in 2005 to 8% in 2011, before stabilizing at 11%-14% through 2020.

Thai Beverage Public Company Limited’s Uniform earnings margins are weaker than you think, but its Uniform asset turns make up for it

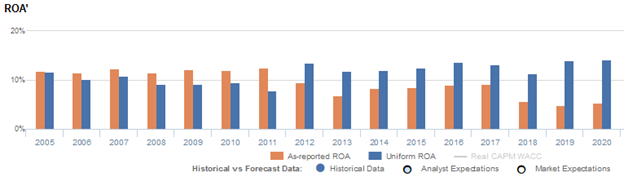

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

After decreasing from 11% in 2005 to 7% in 2011, Uniform margins stabilized at 9%-12% levels through 2020. Meanwhile, Uniform turns maintained 1.0x-1.4x levels from 2005 to 2020.

SUMMARY and Thai Beverage Public Company Limited Tearsheet

As the Uniform Accounting tearsheet for Thai Beverage Public Company Limited (Y92:SGP) highlights, its Uniform P/E trades at 20.5x, which is below the global corporate average of 25.2x, but around its historical average of 21.3x.

Low P/Es require low EPS growth to sustain them. In the case of ThaiBev, the company has recently shown a 1% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Singapore Financial Reporting Standards (SFRS) earnings and convert them to Uniform earnings forecasts. When we do this, ThaiBev’s sell-side analyst-driven forecast is a 27% and 10% earnings growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ThaiBev’s SGD 0.82 stock price. These are often referred to as market embedded expectations.

ThaiBev would need Uniform earnings to grow by 2% in each of the next three years to justify current market expectations. What sell-side analysts expect for ThaiBev’s earnings is above what the current stock market valuation requires in 2021 and 2022.

The company’s earning power is twice the corporate average. Moreover, cash flows and cash on hand are almost 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend and credit risk.

To conclude, ThaiBev’s Uniform earnings growth is in line with its peer averages, and the company is trading above its peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com