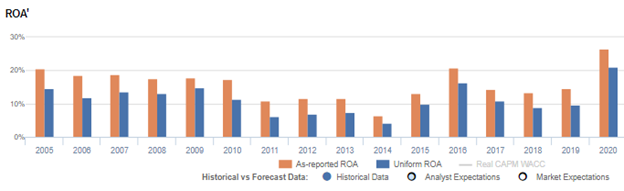

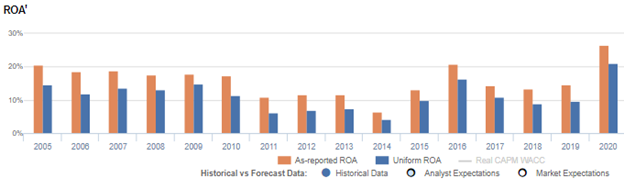

The absence of its rival network delivered an all-time high Uniform ROA of 21%, not 27% per as-reported metrics

Despite the rise of the internet, television still remains to be one of the leading media and advertising platforms in the Philippines.

This company became the Philippines’ dominant network due to the shutdown of its rival network. Although it has seen increasing profitability in recent years, it’s not as strong as what as-reported metrics portray.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Despite the rise of new customer experiences, such as niche and personalized content, many are still using traditional media because it can be easily accessed.

According to a survey conducted by Kantar Media in 2018, about 96% of Filipino respondents stated that they still access media through television.

For many years, the Philippine media landscape has been dominated by two of the country’s largest broadcasting networks, ABS-CBN Corporation (ABS:PHL) and GMA Network, Inc. (GMA7:PHL).

The business rivalry between these two networks has been going on for decades, considering both companies’ market shares haven’t changed during the same period.

That said, each network has its own audience. Prior to its shutdown, ABS-CBN claimed the top spot in most provinces because of its vast geographic reach, while GMA7 controlled urban areas, especially Luzon.

For over 70 years, GMA7 gained popularity through its mainstream programs and sensational television series. Before airing in television and broadcasting on Channel 7, it first started out as a DZBB radio station that was established by Robert La Rue Stewart in 1950. The company was renamed Republic Broadcasting System, Inc. (RBS) in 1963 and expanded to television two years later.

Then, in 1974, Felipe L. Gozon, Menardo R. Jimenez, and Gilberto M. Duavit took over the management of RBS and renamed it to GMA Network, Inc.

As a company that relies on advertising revenues, getting high ratings from its shows is essential to secure more advertising contracts. That wasn’t an easy feat for GMA7 as many of its shows ranked second to ABS-CBN in terms of ratings, resulting in a gradual decline in profitability until 2014.

It was only in 2015 that the company’s shows started to become recognized. Specifically, GMA7’s Eat Bulaga variety show, the country’s longest noontime show that has been on air for over 36 years now, added a viral segment called the AlDub phenomenon that year. Through this segment, the company was able to double its profitability in 2015 from the previous year.

In addition, GMA7 news and public affairs continued to bag awards for news content through its 24 oras news segment and 24 radio stations across the country.

However, in recent years, consumers started shifting to other devices and media channels to get their entertainment and news. To be able to remain relevant, GMA7 focused on improving its right arm for digital media and technology through its GMA New Media.

2020 became an important year for the company because of the pandemic. The presence of the pandemic helped GMA7 effectively cut its production expenses as filming for shows was suspended due to the lockdown.

On top of that, in May 2020, ABS-CBN was shut down as they were not granted franchise renewal.

While the rival station is still appealing their franchise renewal, GMA7 took this as an opportunity to launch its version of digital terrestrial television (DTT) receiver, GMA Affordabox, in June 2020. Eventually, with the absence of its main competitor, GMA7 became the dominant network in the media industry.

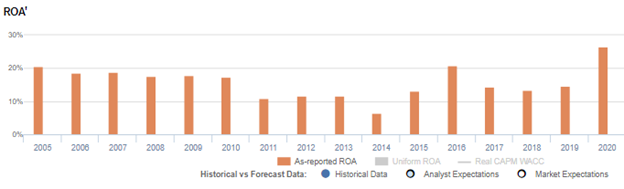

With all of the network improvements and the closure of its main competitor, as-reported metrics seem to agree with the company’s advantages, with ROAs improving from 15% in 2019 to a peak of 27% in 2020.

In reality, while recent events brought a 79% surge in GMA7’s net income in 2020, Uniform ROA only reached a peak of 21% in the current year.

One of the main contributing factors is how Philippine Financial Reporting Standards (PFRS) accounts for property, plant, and equipment (PPE).

According to PFRS, PPE is recorded at historical costs—that is, in the purchasing power the year the fixed asset was recorded. But to better reflect reality, PPE should be adjusted for inflation for each year of use.

In Uniform Accounting, adjustments have to be made so that the asset and cash flow values accurately reflect the current purchasing power each year.

In 2020 alone, the company should have recognized PHP 5 billion more in fixed assets when adjusting for inflation.

When we add PHP 5 billion more to GMA7’s PHP 24 billion asset base, and with the many other necessary adjustments Valens makes, we arrive at a PHP 28 billion Uniform Net Assets and a 21% Uniform ROA.

GMA7’s earning power is weaker than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that GMA7’s profitability is stronger than what real economic metrics highlight.

In reality, GMA7’s true profitability has generally been lower than its as-reported ROA for the past sixteen years. Specifically, as-reported ROA was 27% in 2020, but Uniform ROA was only 21% that year.

As-reported ROA declined from 21% in 2005 to a low of 7% in 2014, before recovering to 21% in 2016. Thereafter, as-reported ROA has compressed to 14%-15% levels in 2017-2019 before achieving a peak of 27% in 2020.

Meanwhile, after declining from 15% in 2005 to a low of 4% in 2014, Uniform ROA improved to 16% in 2016 before fading to 9%-11% levels in 2017-2019. Thereafter, Uniform ROA reached a peak of 21% in 2020.

GMA7’s margins are weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin. However, Uniform margins have been lower than as-reported EBITDA margins in each of the past sixteen years.

As-reported margins declined from 41% in 2005 to a low of 18% in 2014, before expanding to 34% in 2016. Then, as-reported margins compressed to 25%-27% levels in 2017-2019 before elevating to a high of 47% in 2020.

Meanwhile, after fading from 23% in 2005 to 8% in 2014, Uniform margins increased to 21% in 2016. Uniform margins then decreased to 15%-17% in 2017-2019 before reaching a peak of 31% in 2020.

Looking at the firm’s margins alone from 2005-2020, as-reported metrics make the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and GMA Network, Inc. Tearsheet

As the Uniform Accounting tearsheet for GMA Network, Inc. (GMA7:PHL) highlights, it trades at a Uniform P/E of 6.1x, below the global corporate average of 23.7x but around its historical average of 6.3x.

Low P/Es require low EPS growth to sustain them. In the case of GMA7, the company has recently shown a 132% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, GMA7’s sell-side analyst-driven forecast calls for an immaterial EPS growth for 2021 and 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify GMA7’s PHP 9.18 stock price. These are often referred to as market embedded expectations.

GMA7 is currently being valued as if Uniform earnings were to shrink by 23% annually over the next three years. What sell-side analysts expect for Uniform earnings growth is above what the current stock market valuation requires in 2021 and 2022.

The company’s earning power is 3x the long-run corporate average. On the other hand, cash flows and cash on hand are 4x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend and credit risk.

To conclude, GMA7’s Uniform earnings growth is in line with its peers, and the company currently trades in line with average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com