The “Athleisure” trend might be a perfect fit for this company, giving it a Uniform ROA that is twice the as-reported!

Running, home workouts, and a balanced diet. More people have been swapping unhealthy habits for healthy, sustainable alternatives in recent years.

One’s idea of fitness is no longer confined to just playing sports. Functional gyms, crossfit, and yoga are other popular options in the fitness revolution of recent years. People are also more mindful about the food they consume, with organic and whole foods becoming crowd favorites.

Those aren’t the only businesses benefiting from this fitness revolution. This Chinese company made strategic adjustments to respond to the new needs of the rapidly growing market.

However, as-reported metrics do not show this company’s REAL economic profitability. Uniform Accounting, on the other hand, shows that this company’s efforts are paying off with over twice the returns compared to as-reported value in the past years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Whether it’s because of a pre-existing condition or they just want to look or feel better, more people are making the effort to get physically fit.

In the U.S. alone, gym membership increased by nearly 2 million members in 2019 from the 62.5 million members recorded in 2018. China is an even bigger market, with over 400 million gym memberships.

With the rise of gyms and fitness centers came the rise of fitness or sports apparel. These weren’t just any ordinary apparel—they had to have some added benefit so that people would choose to buy them over just wearing any workout attire.

The rise of “athleisure,” a fashion trend distinguished by comfortable clothing that can be used for both exercise and everyday wear, has become proof of consumers’ newfound interest in functional and personalized products.

Sportswear companies now needed to make clothes that were both functional and aesthetically pleasing.

According to Grandview Research, the global sportswear industry is growing. With a 2018 market size of an estimated USD 239.8 billion, the industry is expected to register a CAGR of 10.4% from 2019 to 2025.

Competition has grown fiercer, too. It’s not enough for companies in the industry to be able to give the lowest prices, they must also be able to give the best quality products in a wide range of variety.

Brands have started to invest more in product quality and innovative technology such as nano-technology, microfibers, insulation, and compression garments in hopes of gaining an edge on the market.

Amidst the intense competition is Anta Sports Products, the world’s third largest sportswear company by revenue. Established in 1991, Anta has mainly engaged in the design, development, manufacturing, and distribution of sports shoes, apparel, and accessories in Mainland China, Hong Kong, and Macau.

In 2016, Anta adopted a single-focus, multi-brand, and omni-channel strategy with the goal of integrating new and existing retail channels to increase Anta’s market presence in China.

One of the main initiatives under the strategy was the creation of a well-rounded brand portfolio with brands such as Anta, Fila, Descente, Sprandi, Kingkow, and Kolon Sport used to cater to different market segments with different needs—from functional to fashionable sportswear.

In 2019, Anta acquired the Finnish sportswear group, Amer Sports Corporation, which handles globally-known brands such as Wilson.

Anta has also taken advantage of the growing online market by investing in e-commerce. Its e-commerce business offers a wide range of new products from the different brands in its portfolio, launching exclusive products online, and distributing in-season products offline.

To better integrate its physical and online stores, Anta allowed select authorized distributors to operate online stores outside of its existing online flagship stores, although under strict guidelines and policies. It also collaborated with popular e-commerce platforms in China, such as Tmall, JD, and Vipshop, to further boost brand presence online.

The company also restructured its brands into three business segments: performance sports, fashion sports, and outdoor sports. This would allow Anta the flexibility to refocus its distribution channels and improve quality control in order to let its brands effectively penetrate different markets in China.

Considering the company’s multi-brand, omni-channel strategy, its as-reported returns of 17% in 2019 is weaker than what it should really be.

Anta’s real economic profitability is better reflected with Uniform Accounting adjustments, which show its TRUE earning power.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

From 2008 to 2019, Anta has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 25% to 67% of its unadjusted total assets.

After excess cash and other significant adjustments are made, the company actually had a 34% Uniform ROA in 2019, which is 2x stronger than their as-reported ROA of 17%.

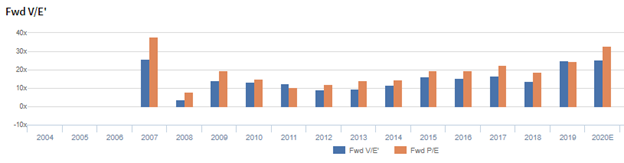

Anta’s valuations are above the corporate averages

ANTA Sports Products Limited (2020:HKG) currently trades above corporate averages at a 26.4x Uniform P/E (blue bars), but below its as-reported P/E of 33.9x (orange bars).

Even at these levels, the market is pricing in expectations for Uniform ROA to decline to 18% in 2024, accompanied by 25% Uniform asset growth going forward.

However, analysts have bullish expectations, projecting Uniform ROA to improve to 38% levels in 2021, accompanied by a 6% Uniform asset growth.

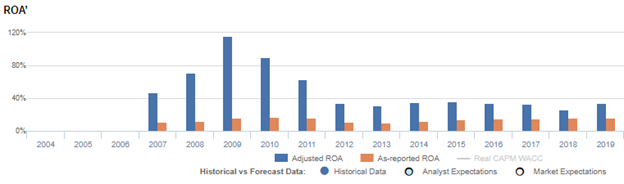

Anta’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Anta’s Uniform ROA has actually been higher than its as-reported ROA in the past thirteen years. For example, as-reported ROA is 17% in 2019, significantly lower than its Uniform ROA of 34%. When Uniform ROA reached 116% in 2009, as-reported ROA was just at 16%. The company’s Uniform ROA for the past thirteen years has ranged from 26% to 116%, while as-reported ROA ranged only from 10% to 17% in the same timeframe.

From 47% in 2007, Uniform ROA gradually improved to a peak of 116% in 2009, before falling to its all-time low of 26% in 2018. Afterwards, Uniform ROA recovered to 34% in 2019.

Anta’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins improved from 15% in 2007 to 21% in 2009, before falling to 16% in 2013. Uniform earnings margins gradually recovered to 19% in 2019.

Meanwhile, Uniform asset turns improved from 3.1x in 2007 to 5.4x in 2009, before falling to 1.7x in 2019.

SUMMARY and ANTA Sports Products Tearsheet

As the Uniform Accounting tearsheet for ANTA Sports Products Limited (2020:HKG) highlights, the Uniform P/E trades at 26.4x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Anta, the company has recently shown a 41% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Accounting Standards (HKAS) earnings and convert them to Uniform earnings forecasts. When we do this, Anta’s sell-side analyst-driven forecast is a 2% and 46% earnings growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Anta’s HKD 73.50 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 7% each year over the next three years to justify current prices. What Wall Street analysts expect for Anta’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

The company’s earning power is 6x the corporate average. Also, cash flows are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Anta’s Uniform earnings growth is below its peer averages in 2019. However, the company is trading in line with peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com