The beauty of this company lies within its ability to innovate, giving it a 13% Uniform return that’s twice its as-reported!

In the past few months, numerous countries have enforced lockdown or quarantine procedures that encourage a work-from-home setup. As a result, people are spending more time at home, which means less time working on their appearances the way they would have pre-pandemic.

It’s not surprising then that the beauty and makeup industry was not spared from the economic issues caused by the pandemic. Makeup is not a requirement at home, and wearing masks outside has made wearing lipstick unnecessary. Despite this, Japan’s oldest cosmetics company remains hopeful that their reformed strategy will allow them to rise above the challenge.

As-reported metrics do not show the true beauty of this company’s profitability. Uniform Accounting shows that this company’s Uniform return on assets (ROA) is higher than what it looks like.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

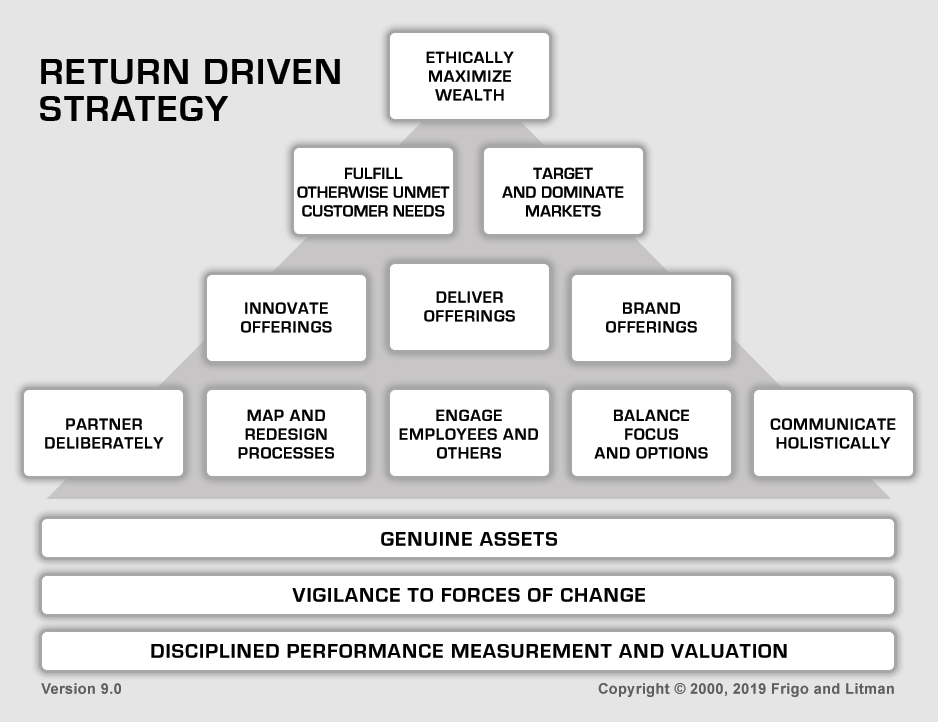

The Return Driven Strategy™, as discussed in the book Driven, lays out a framework for us to understand which businesses best achieve wealth-creation for themselves and for society. The framework contains three foundations and eleven tenets illustrated in a pyramid.

We won’t go into a discussion of the framework, but we’d like to highlight one competency tenet that has become even more important for companies in light of the ongoing pandemic.

Innovate offerings.

Shiseido Company, Limited has incorporated this tenet since its inception in 1872.

With the constant change in consumers’ needs, innovation is essential in keeping a business relevant. Without innovation to fulfill otherwise unmet customer needs, the business may get left behind.

Innovation not only gives a company the competitive advantage it needs, but can also turn the company around.

This Japanese brand was established as a pharmaceutical company selling herbal medicine. The company ventured into other industries before turning into the global cosmetics brand we know today.

Who would have thought that the marriage of eastern artistry and aesthetics with western technology and science would give birth to a company that innovates in the area of cosmetics? The combination of these two influences in its products is still apparent, as seen in Shiseido’s brand image and advertisements until today.

Shiseido is not just one of the oldest cosmetics companies in the world, but it is also the largest cosmetics company in Japan and the 5th largest in the world. It handles premium brands such as Shiseido, Nars, and Laura Mercier, as well as drugstore brands such as Senka and Elixir.

To increase market leadership, Shiseido launched VISION 2020 in 2014. This medium-to-long-term strategy aims to rebuild a strong business foundation within three years—mainly in its center of operations in Japan. This was done by strengthening its business portfolio and prioritizing prestige brands through numerous acquisitions—a notable one of which is Laura Mercier.

From the strong business foundation built during the first three years of strategy implementation, Shiseido further aimed to accelerate growth in 2017 onwards through digitalization and innovation. The company executed this through partnerships with e-commerce platforms, as well as increased investments in research and development.

Ultimately, Shiseido aims to fulfill its VISION 2020 strategy of having JPY 1 trillion in net sales and over JPY 120 billion in operating profits by 2020.

True to Shiseido’s expectations, the strategy was proving to be successful. In 2017, it reached its net sales goal three years ahead of the deadline. Also, ever since it started the strategy in 2014, Shiseido has experienced consistently high Uniform ROAs.

However, as COVID-19 plagued the world this year, VISION 2020 has been put to the test. Being a company that uses department stores as its main distribution channel, Shiseido’s sales plunged when social distancing measures caused physical stores to shorten operating hours or close temporarily.

Its non-cosmetic business units such as the Shiseido Beauty Salon and the Shiseido Beauty Academy have also suffered losses as travel restrictions hindered tourism and foreign consumers in Japan. As a result, short-term outlook for Shiseido is unfavorable, with analysts expecting Shiseido’s Uniform ROA to drop by 9% by the end of the year.

Despite this, Shiseido maintains its belief that with the right reforms, growth achieved from VISION 2020 pre-COVID-19 can be maintained and utilized for sustainable growth in the future. In response to the changes brought about by the pandemic, the company has reformed its strategy and increased online presence globally. It aims to use the current situation as an opportunity to fast-track the company’s plans for digitalization.

Considering the company’s efforts to innovate and accelerate growth, its as-reported returns of 6% in 2019 is weaker than what it really is.

Shiseido’s real economic profitability is better reflected with Uniform Accounting adjustments, which shows its TRUE earning power.

Shiseido has made a number of acquisitions over the last decade, including Drunk Elephant, Olivo Laboratories, and Match Co. This causes an accounting distortion given that as-reported metrics fail to consider the amount of goodwill on the company’s balance sheet from these acquisitions, which sits at about JPY 225 billion in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

After goodwill and other significant adjustments are made, the company actually had a 13% Uniform ROA in 2019, which is more than 2x stronger than its as-reported ROA of 6%.

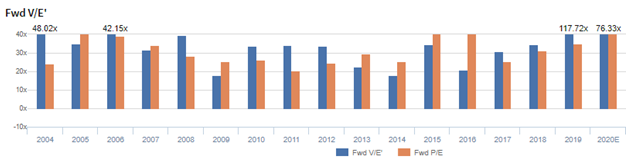

Shiseido’s valuations are cheaper than corporate averages

Shiseido Company, Limited (4911:JPN) currently trades above corporate averages at a 76.3x Uniform P/E (blue bars), below its as-reported P/E of 68.1x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to increase to 21% in 2024, accompanied by 4% Uniform asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to decline to 10% levels in 2021, accompanied by a 4% Uniform asset growth.

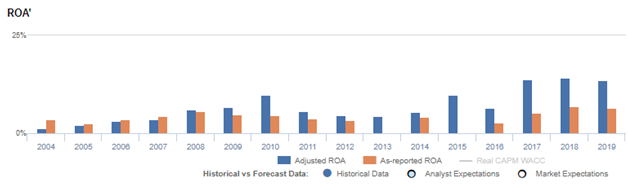

Shiseido’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Shiseido’s Uniform ROA has actually been higher than its as-reported ROA in the past twelve years. For example, as-reported ROA is 6% in 2019, significantly lower than its Uniform ROA of 13%. When Uniform ROA reached 14% in 2018, as-reported ROA was just at 7%.

The company’s Uniform ROA during the past sixteen years has ranged from 1%-14%, while as-reported ROA ranged only from immaterial levels to 7% in the same timeframe.

From 1% in 2004, Uniform ROA gradually increased to 10% in 2010, before falling back to 4% in 2013. Afterwards, Uniform ROA peaked to 14% in 2018, before settling to 13% in 2019.

Shiseido’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins, and to a lesser extent, by Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins increased from 1% in 2004 to 7% in 2010, before falling to 3% in 2013. Uniform earnings margins gradually recovered to 7% in 2019.

Meanwhile, Uniform asset turns increased from 1.2x in 2004 to 1.6x in 2009, and rose further to 2.2x in 2015. It then settled at 1.9x in 2019.

SUMMARY and Shiseido Company, Limited Tearsheet

As the Uniform Accounting tearsheet for Shiseido Company, Limited (4911:JPN) highlights, the Uniform P/E trades at 76.3x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Shiseido, the company has recently shown a 13% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Shiseido’s sell-side analyst-driven forecast is a 71% earnings shrinkage in 2020 and 183% earnings growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Shiseido’s JPY 6,718 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 15% each year over the next three years to justify current prices. What Wall Street analysts expect for Shiseido’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

The company’s earning power is 2x the corporate average. Also, cash flows are higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Shiseido’s Uniform earnings growth is below its peer averages in 2019. However, the company is also trading above average peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com