The future is bright and shiny for this mining business unearthing Uniform returns at 37%, not as-reported 16%

This mining business spearheads the Philippines’ nickel ore exports. In turn, this means that it also tops the world’s market for the commodity.

However, as-reported metrics undervalues this development presenting a return of 16%, when in reality Uniform returns show more than double at 37%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Nickel Asia Corporation (NIKL:PHL), founded in 2008, is a prominent mining business in the Philippines. It focuses on discovering, extracting, and processing nickel ore and other related minerals. The company runs a number of open-pit and underground mining sites, including operations in Surigao del Norte, Palawan, and Zambales, among other places.

It provides nickel ore to both domestic and foreign markets, with China serving as a significant export market. Throughout the years, Nickel Asia has grown to become one of the nation’s major manufacturers of nickel.

In 2021, the company posted profits rising by 92% to PHP 7.8 billion for the year primarily due to higher ore sales prices. The commodity’s prices were driven by a classic demand and supply issue, which is the rise of the former and lack of the latter.

Supply for the commodity was negatively impacted by Indonesia’s ban on nickel ore export in 2020, which was home to 22% of the world’s nickel reserves. This was done to encourage domestic processing and increase the value-added benefits of the resource for their country.

On the other hand, the surging demand for nickel is due to the accelerating production of Electric Vehicles (EVs). The commodity is used for the batteries that are vital for EVs to function. It was reported that the EV market in Southeast Asia was around $500 million in 2021 and it is forecasted to grow to $2.7 billion by 2027.

Looking forward, the future for Nickel Asia is “bright and shiny” as significant tailwinds propel them to be a top nickel ore producer.

With the recent geopolitical tensions between Russia and Ukraine, and the subsequent sanctions imposed on the former, the supply of nickel ore from Russia–the world’s third largest exporter–is cut off.

Coupled with Indonesia’s ban, this opens up the Philippines’ potential to dominate the nickel market once again. The country produced a total of $1.5 billion in nickel ore exports for 2021, making the Philippines the largest nickel exporter in the world.

And with Nickel Asia leading the charge…

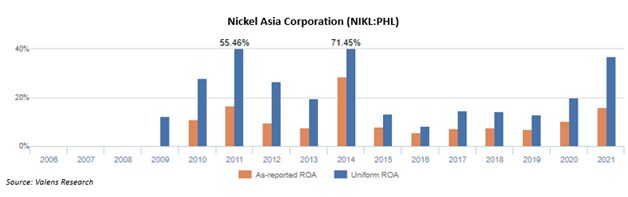

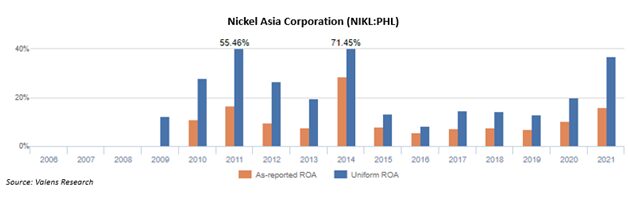

However, as-reported metrics in 2021 show that the company has generated steady but little returns since 2015 at 16%.

In reality, the company’s real economic profitability has actually been more than what as-reported metrics highlight, reaching 37% for the year.

The crucial lesson to learn from this is that accounting distortions can completely alter a company’s market valuation, which in turn can affect an investor’s stock decisions. In this case, Uniform ROA levels are more than double as-reported ROA levels.

Historically, one of the largest distortions for Nickel Asia comes from the treatment of minority expenses or the income attributable to the non-controlling interests of a company’s subsidiaries.

The Philippine Financial Reporting Standards (PFRS) allows minority interest expense to be recognized under operating cash flow, misleading people to think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders provide capital to the subsidiary in exchange for a piece of the company’s profits. As a result, minority interest expense should not be subtracted from revenue when calculating a company’s real core earnings.

In 2021, Nickel Asia recognized PHP 2.83 billion in minority interest expense, resulting in a PHP 7.81 billion net income and a 16% as-reported ROA. Adding this back alongside the many other adjustments Valens makes, the company should actually be recognizing PHP 9.62 billion in Uniform earnings and a 37% Uniform ROA.

Nickel Asia’s profitability is stronger than you think

The market’s assessment of the company’s recent profitability is distorted by as-reported measures. If you only considered as-reported ROA, you might conclude that the company is far less successful than its actual economic measures indicate. As-reported ROA, for instance, was 16% in 2021, which is far below its Uniform ROA of 37%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher than its as-reported ROA in each of the past eleven years..Additionally, when Uniform ROA reached a peak of 72% in 2014, as-reported ROA was only at 29%.

After rising from 12% in 2009 to 56% in 2011, Uniform ROA dropped to 20% in 2013 as nickel ore prices weakened. Thereafter, Uniform ROA rebounded to a peak of 72% in 2014, before deteriorating to 8% in 2016 and subsequently recovering to 37% by 2021.

Nickel Asia has a more efficient business than you think

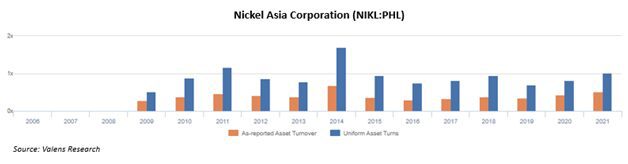

The firm’s asset utilization, a critical factor in profitability, is also greatly distorted. As-reported asset turnover of 0.5x in 2021 was lower than Uniform asset turnover of 1.0x, giving the organization a lower asset efficiency score than actual economic measures indicate.

Additionally, for the past ten years, as-reported turns have consistently been less than Uniform turns, which has distorted the market’s assessment of the firm’s historical asset efficiency levels.

Uniform turns historically increased from 0.5x in 2009 then jumped to a 1.7x high in 2014. This pattern is similar to the company’s ROA trend. Then, between 2016 and 2021, Uniform turns compressed to and stabilized at 0.7x-1.0x values.

SUMMARY and Nickel Asia Corporation Tearsheet

As our Uniform Accounting tearsheet for Nickel Asia Corporation (NIKL:PHL) highlights, the company trades at a Uniform P/E of 6.3x, below the global corporate average of 18.4x but around its historical P/E of 6.4x.

Low P/Es require low EPS growth to sustain them. In the case of Nickel Asia, the company has recently shown a 90% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Nickel Asia’s sell-side analyst-driven forecast is to see Uniform earnings growth of 16% and 34% in 2022 and 2023, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Nickel Asia’s PHP 6.52 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 17% per year over the next three years. What sell-side analysts expect for Nickel Asia’s earnings growth is well above what the current stock market valuation requires in 2022 and 2023.

Moreover, the company’s earning power is 6x the long-run corporate average. Additionally, cash flows and cash on hand are 5.3x of total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Nickel Asia’s Uniform earnings growth is above its peer averages, but in line with its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com