The growing number of cyberattacks has helped this company magnify its position in the industry, securing Uniform ROAs of 25%+

Malware and ransomware attacks have been a common occurrence over the recent years. Corporations such as Adobe, eBay, and Facebook, among others, have been targets of cyberattacks causing data breaches that cost hundreds of millions of dollars.

As technology advances and organizations begin to rely heavily on digital spaces to store highly sensitive data, cybersecurity has become an imperative safeguard against the weaponization of this information.

This company, one of the top cybersecurity firms in the world, is positioned to benefit from the increasing demand in cybersecurity platforms. While as-reported metrics would say that it’s not the case, with the company never showing profits, Uniform ROAs of 25%+ would argue otherwise.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

On May 4, 2000, people from around the world received an email with the subject line “ILOVEYOU” and an attached text file.

If we received that email today, we would be extremely cautious about opening a random email from an unknown sender. But at that time, the internet was still a relatively new concept. People were likely uninformed about the dangers of clicking suspicious links, and their curiosity got the better of them.

The first batch of recipients of the “ILOVEYOU” email began opening the attached text file, which was later revealed to be a program that sent out copies of itself to the user’s entire address book. The next wave of recipients then opened the same email, and the cycle continued.

Corporate servers were soon battling with an email that sent itself back and forth continuously. To make matters worse, the virus also renamed and deleted system files and personal files on the user’s computer, destroying much of their hard drive.

In just a few hours, the ILOVEYOU virus managed to spread to over a million computers across the globe. Major corporations and governments including the Pentagon, the British Parliament, Microsoft, and Ford had their communication servers taken offline and their operations disrupted.

What started out as a virus created to steal internet account passwords for free use of the service became a virus that lasted for about 10 days, infecting over 50 million, or 10%, of the world’s internet-connected computers.

Anti-virus software companies slowly released updates to resolve the issue and bring operations back online while the FBI hunted down the people responsible for the attack.

Authorities traced the code back to the Philippines where programmer Onel de Guzman was caught. However, because there were no laws against writing malware at the time, the charges were dropped.

The Guinness World Record named the ILOVEYOU virus as the most viral computer virus of all time. Besides single-handedly disrupting some of the world’s major corporations in a span of a few hours, it also caused at least $10 billion in damages.

Over the two decades since the attack, society has evolved to a point where we are growing increasingly reliant on digital assets to function. Corporations, governments, financial and medical institutions, as well as other organizations are storing massive amounts of data on computers and other digital devices now more than ever.

As the number of attacks even more sophisticated than the ILOVEYOU virus has grown, cybersecurity has taken the crucial role of safeguarding the sensitive information that organizations have amassed.

The global cybersecurity industry’s growth from an $88 billion market in 2012 to $150 billion in 2020—which is forecast to almost double to $270 billion by 2026—highlights how corporations and other organizations are emphasizing the importance of protecting their digital assets.

Palo Alto Networks (PANW), one of the top cybersecurity companies in the world, has benefited from that growth in cybersecurity spending.

The company is primarily focused on the development of firewalls and intrusion prevention systems as well as products to prevent malware. It also offers cloud security solutions, which are especially important today since many businesses and employees are working from remote servers because of the pandemic.

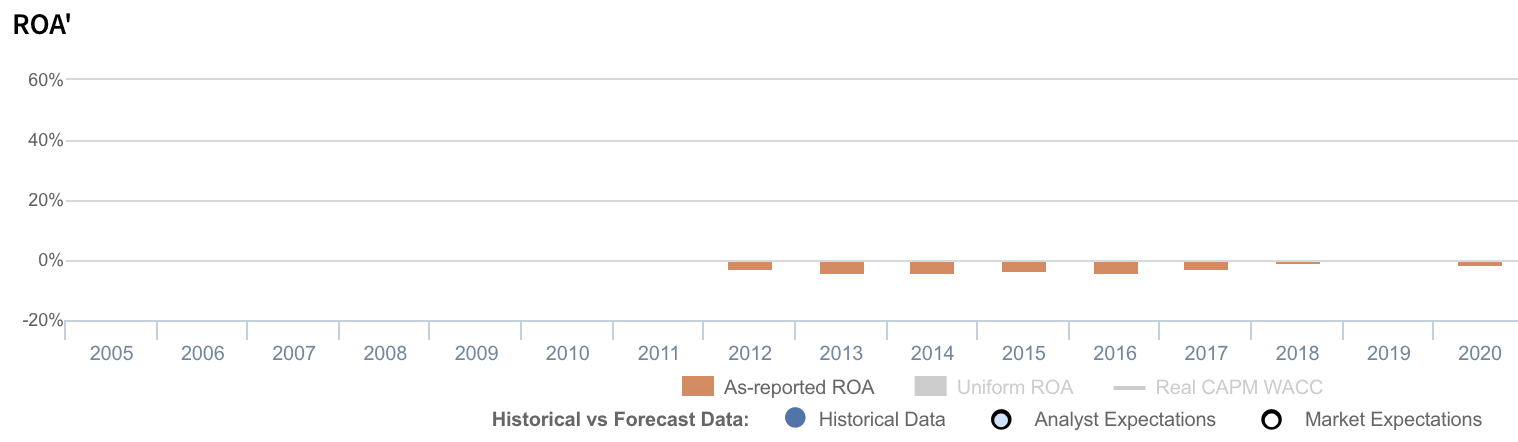

However, looking at as-reported metrics, it seems that Palo Alto hasn’t benefited at all from the macro tailwinds brought by the cybersecurity wave. Worse, it looks like the company has never profited during its operating lifetime, with return on assets (ROAs) ranging from -4% to 0%.

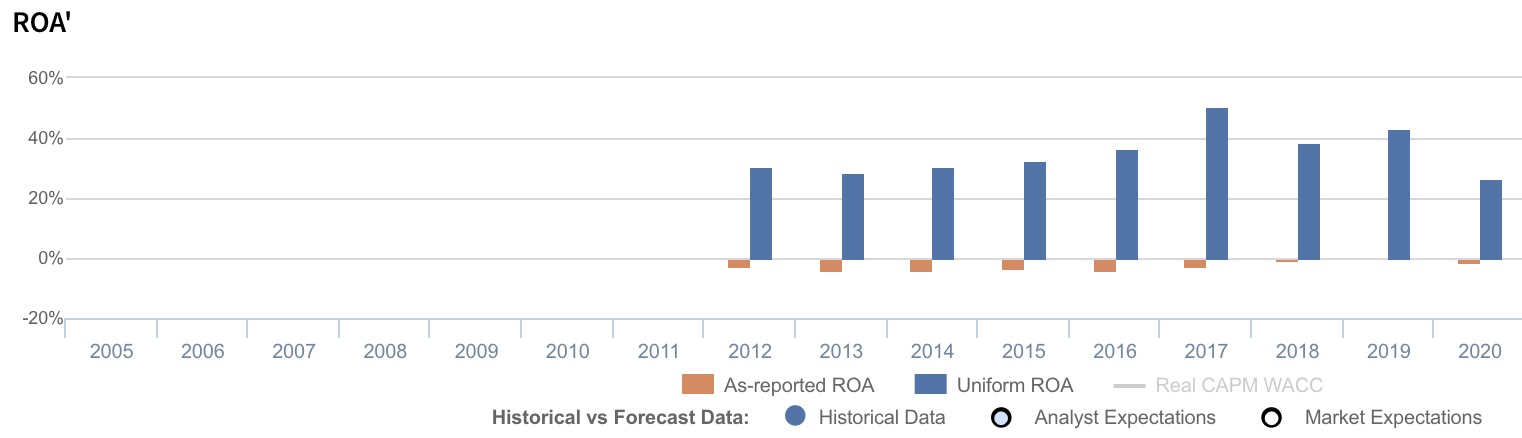

In reality, its Uniform ROAs north of 25% prove that the company did capture market share and financially benefited from its cybersecurity offerings.

One source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to recording it as an investment on the balance sheet, net income can become materially understated.

Palo Alto materially spends on R&D as it continues to make investments to enhance its hardware and software platform. The company’s R&D spend has consistently been around 30% of total operating costs, significantly distorting the company’s profitability.

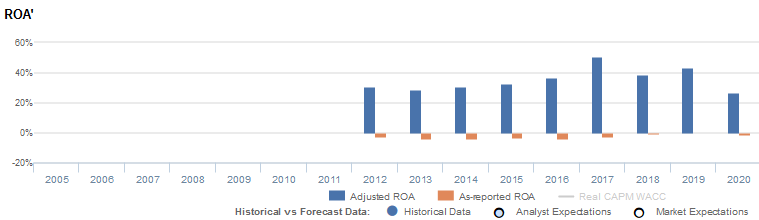

After adjustments, we can see that Palo Alto’s Uniform ROA is, in fact, positive and is materially higher than as-reported ROAs. Without this adjustment, it appears that the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Palo Alto’s earning power is actually far more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Palo Alto’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA was -1% in 2020, but its Uniform ROA was actually significantly higher at 26%.

Specifically, Palo Alto’s Uniform ROA has ranged from 26% to 51% in the past nine years while as-reported ROA remained negative in the same time frame.

After expanding from 31% in 2012 to a peak of 51% in 2017, Uniform ROA compressed to a low of 26% in 2020.

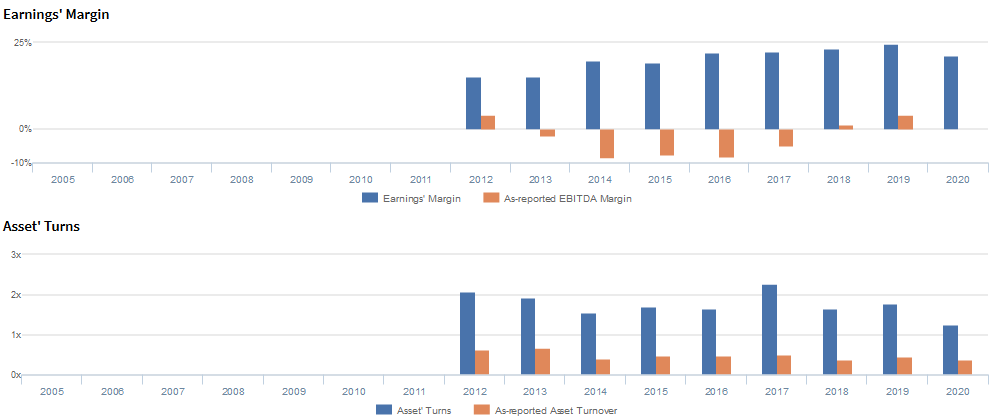

Palo Alto’s Uniform earnings margins are stronger than you think

Palo Alto’s historical improvements in Uniform ROA have been driven by expanding Uniform earnings margins, slightly offset by weakening Uniform asset turns.

Uniform margins have consistently expanded from 15% levels in 2012-2013 to a peak of 25% in 2019, before compressing to 21% in 2020.

Meanwhile, after declining from 2.1x in 2012 to 1.6x-1.7x levels in 2014-2016, Uniform turns improved to a peak of 2.3x in 2017 before slipping to a low of 1.2x in 2020.

At current valuations, markets are pricing in expectations for material compression in Uniform margins and for Uniform turns to decline to new lows.

SUMMARY and Palo Alto Tearsheet

As the Uniform Accounting tearsheet for Palo Alto Networks, Inc. (PANW) highlights, the Uniform P/E trades at 32.7x, which is above corporate average valuation levels, but around its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Palo Alto, the company has recently shown a 2% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Palo Alto’s Wall Street analyst-driven forecast is a 3% and 17% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Palo Alto’s $221 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 16% each year over the next three years to justify current prices. What Wall Street analysts expect for Palo Alto’s earnings growth is below what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows and cash on hand are 3x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Palo Alto’s Uniform earnings growth is above its peer averages in 2021, and the company is trading in line with its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com