The return of face-to-face classes has allowed this company to unlock a Uniform ROA of 5%, not 3%

The reopening of schools has welcomed students back to face-to-face classes after more than two years of pandemic-led online learning. This has made plenty of students decide to return to school as many may have felt the ineffectiveness of remote learning.

As a result, one of the largest education corporations in the country was able to see its enrollment rates skyrocket, producing an uptick in profitability greater than what as-reported metrics show.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The lack of physical interaction between students with their teachers and peers is only one of the many disadvantages of remote learning. Other reasons include difficulty maintaining focus and the lack of receiving immediate feedback as would be the norm in a face-to-face setting.

According to a report by the Department of Education, enrollment rates for S.Y. 2020-21 dropped 10% from the prior year, equivalent to a total of more than 2.7 million fewer students.

This was no different from what one of the largest education corporations in the country, STI Education Systems Holdings, Inc. (STI:PHL), had experienced during this sudden change in the academic landscape. STI, which runs STI schools and iAcademy, saw enrollment fall during this time as the pandemic disrupted operations.

The cons of remote learning wasn’t the only factor that held students back from enrolling during the past two school years. The pandemic also brought financial challenges to many families, making it difficult for them to afford education for their children.

Realizing this, STI started to roll out financial aid programs and reduce school fees to encourage students to enroll in the upcoming school year. This resulted in a massive increase in their enrollment rates, from 70,223 in S.Y. 2020-21 to 82,629 students in S.Y. 2021-22.

As the country started to reopen in 2022, STI started to offer more academic programs and resumed face-to-face classes for S.Y. 2022-23. Unsurprisingly, the total number of ongoing students reached 94,312, which represented a 14% increase in enrollees from the previous year.

It is an understatement to say that STI was able to bounce back from the pandemic slump, as it has most recently seen a 300 percent increase in profit in H1 2023 at PHP 223.4 million, compared to PHP 56.0 million during the prior fiscal year.

As the country continues to lift restrictions and fully transition back into the pre-pandemic practices, it is likely that students will resume their day-to-day schooling activities for the following years, boding well for education corporations such as STI and the country as a whole.

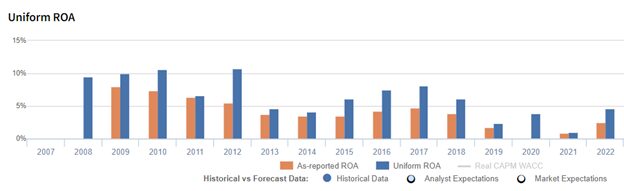

Overall, STI fared well in the past year despite the pandemic. However, looking at the as-reported metrics, the company was shown to be less lucrative, only reaching 3% in 2022.

In reality, STI has managed to effectively minimize a continuous downtrend in enrollment rates by rolling out financial aid programs, reducing school fees, and extending their academic programs, which has led them to reach a Uniform ROA of 5% in 2022.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example, in 2022, STI recognized an interest expense of PHP 313.3 million, three quarters of as-reported net income of PHP 414.0 million. When we add the PHP 313.3 million back to earnings, because it is not an operating expense, net income increases. This adjustment alone represents a 2.1% jump in Uniform earning power.

Cross-comparison against peers also becomes possible since the performance, expectations, and valuations of companies are now evaluated irrespective of the amount of leverage.

STI’s profitability is stronger than you think in the last two years

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that STI’s profitability has been weaker than what real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROA has been understated in the past two years. For example, as-reported ROA was 3% in 2022, but its Uniform ROA was higher at 5%.

SUMMARY and STI Education Systems Holdings, Inc. Tearsheet

As our Uniform Accounting tearsheet for STI Education Systems Holdings, Inc.(STI:PHL) highlights, the company trades at a Uniform P/E of 13.4x, which is below the global corporate average of 18.4x and its historical P/E of 22.5x.

Low P/Es require low EPS growth to sustain them. In the case of STI, the company has recently shown a 229% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, STI’s sell-side analyst-driven forecast is to see a 4% Uniform earnings growth and a 21% Uniform earnings shrinkage in 2023 and 2024, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify STI’s PHP 0.36 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 12% over the next three years. What sell-side analysts expect for GSMI’s earnings growth is above what the current stock market valuation requires through 2023.

However, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate dividend risk.

To conclude, STI’s Uniform earnings growth is below its peer averages and it also currently trades below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com