The ship has sailed! This port operator pushed through with its expansion initiatives and anchored a Uniform ROA of 7%+

This major port operator took advantage of ports reopening and continued with its expansion initiatives despite the challenging environment. While as-reported data shows that this strategy will barely keep the business afloat, its Uniform ROA actually says otherwise.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

It’s hard to imagine a world without smartphones and smart TVs, especially now with the Internet of Things (IoT). There’s a reason why these devices are called “smart” to begin with.

Prior to this era, the existence of a device capable of synergizing an operating system that supports both mobile and web applications was unheard of. Now, we can purchase things in an instant, literally with a click of a button.

We can even go so far as to say online purchasing has become the backbone of economic progress during these unprecedented times. For this reason, it’s become increasingly important to have seamless transportation of import and export commodities.

International Container Terminal Services, Inc. (ICT:PHL), which is owned by billionaire Enrique Razon Jr., serves as the Philippines’ major port operator. The company has access to ports from all over the globe, making shipments increasingly convenient and accessible to Filipinos.

However, because of port closures and strict quarantine restrictions in several regions, International Container Terminal had a flat performance in 2020.

Now that ports have started to reopen, the company is slowly recovering from this pandemic-induced performance, generating profits of nearly PHP 10 billion in the second quarter of 2021. This 73% growth in profits was the result of the significantly lower profitability base in 2020.

As global trade continues to improve, International Container Terminal went on to execute its differentiated strategy through the company’s expansion initiatives. While other port operators deemed it prudent to forgo these plans, the company thought otherwise.

With the majority of individuals opting to shop online, there are new opportunities not only for e-commerce but port operators as well, prompting the company to further expand its operations.

These expansion initiatives include the purchase of an additional 10% stake under its subsidiary ICTSI Africa, as well as the recently completed berth expansion project. Aside from this, International Container Terminal even opened new terminals and bought the entirety of Manila Harbour Center Port Services, Inc. (MHCPSI), which currently operates the largest international breakbulk and bulk private port facility at Port Manila, for PHP 2.45 billion.

Through MHCPSI, the company was able to unload 48 light rail vehicles (LRVs) from Spain and Mexico in light of the LRT 1 Cavite Extension Project.

Overall, International Container Terminal’s continued resiliency and execution of its expansion initiatives drove this company’s business.

However, looking at the as-reported metrics, the company has had stable returns only near cost-of-capital levels, implying that the firm has generated little economic value for its stockholders in the past decade.

In reality, we see that the firm’s returns have actually seen robust and generally improving returns in the last eight years.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2020, International Container Terminal recorded interest costs at PHP 13.2 billion. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 27.1 billion net income and a 13% Uniform ROA, higher than its PHP 5.2 billion as-reported net loss and immaterial as-reported ROA.

International Container Terminal’s earning power is more robust than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

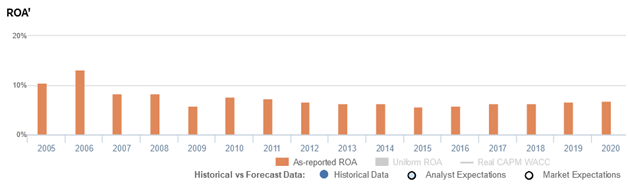

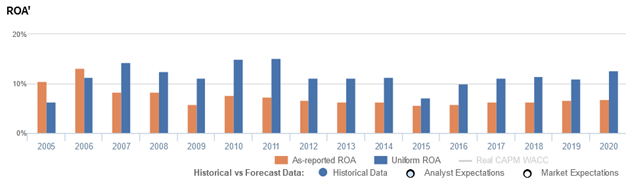

International Container Terminal’s Uniform ROA has actually been higher than its as-reported ROA in the past fourteen years. For example, as-reported ROA was 7% in 2020, significantly lower than Uniform ROA of 13%.

Historically, as-reported ROA has improved from 10% in 2005 to 13% in 2006, before compressing to 6%-8% levels through 2020. Meanwhile, since 2005, Uniform ROA has expanded from 6% to 15% levels in 2010-2011, before compressing to 7% in 2015 and recovering to 13% in 2020.

International Container Terminal’s margins are a lot weaker than you think but its Uniform asset turns slightly make up for it

Trends in Uniform ROA have been driven by trends in Uniform earnings margin, coupled with generally declining Uniform asset turns.

Uniform margins expanded from 12% in 2005 to 31% in 2007, before compressing to 20% in 2015 and recovering to 36% in 2020. Meanwhile, Uniform turn receded from 0.6x in 2006 to 0.3x-0.4x levels in 2012-2020.

At current valuations, the market is pricing in expectations for Uniform margins to reverse recent improvements and for Uniform turns to continue declining.

SUMMARY and International Container Terminal Tearsheet

As our Uniform Accounting tearsheet for International Container Terminal Services, Inc. (ICT:PHL) highlights, the company trades at a Uniform P/E of 18.7x, below the global corporate average of 24.3x, but above its historical P/E of 13.5x.

Low P/Es require low EPS growth to sustain them. In the case of International Container Terminal, the company has recently shown a 2% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, International Container Terminal’s sell-side analyst-driven forecast is to see Uniform earnings grow by 28% and 21% by 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify International Container Terminal’s PHP 178.90 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to decline 6% annually over the next three years. What sell-side analysts expect for International Container Terminal’s earnings growth is well above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 2x above the long-run corporate average. However, cash flows and cash on hand fall below total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 210bps above the risk-free rate. Together, this signals a high dividend risk.

To conclude, International Container Terminal’s Uniform earnings growth is in line with its peer averages, but currently trades below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com