This $9 billion company kept its head “up in the cloud,” reaching Uniform ROAs of 13%+

Cloud storage has been an increasingly significant cog in the modern business machine. Given the theoretically infinite volume of data that businesses have to work with, cloud storage offers a solution that relies less and less on the more asset-intensive, limited-capacity in-house servers.

This company became a major player in that industry by competing on value, interface intuitiveness, and any-platform compatibility.

However, despite its competitive advantages and the significant user base it has amassed, as-reported data makes it seem like the business has not been profitable. In reality, Uniform Accounting shows that returns have actually been positive for the past four years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Drew Houston, then-student at MIT, created one of the largest file-hosting platforms while on a bus in New York. He had a habit of forgetting to bring his USB flash drive that had the files he needed to work on. He needed a solution that would allow him access to his files without the need for a flash drive.

The lines of codes that Drew would write to address his problem would eventually be the $9 billion cloud storage powerhouse, Dropbox (DBX).

Businesses used to depend on limited-capacity in-house servers for data storage. With the ever-increasing volume of data businesses have to work with, those storage spaces are not enough. Companies then turned to cloud services, which have become a valuable alternative that allows for unlimited storage and ubiquitous access.

Similar to how people have moved from using DVDs and CDs to watch movies and listen to music to simply streaming on Netflix or Spotify, many businesses have moved most, if not all, their data and software to the cloud.

Since it is good practice for businesses not to have all of their data in just one place, they use several different cloud services. Diversifying their storage location helps eliminate operational risk by having access to backup files whenever necessary.

With the cloud industry growing by more than 20% over the past few years, businesses have plenty of options to choose from.

Currently, heavyweights Amazon, Google, Apple, and Microsoft are dominating the cloud infrastructure space. However, when it comes to the simple service of file storage, Dropbox manages to hold its own with a market share of around 20%, second only to Google.

The reason why Dropbox is a popular application businesses use for backup storage is because of four reasons: inexpensive subscription prices, competitive technology, ease of use, and platform-agnosticism.

A premium subscription for Dropbox would cost as low as $10/month for 2TB of storage. Since it can’t compete on price alone, the company has also added features such as smart sync, file recovery, and remote data wipe to boost their competitive position.

In addition, Dropbox’s low-latency sync speed enables it to deliver the fastest upload and download speeds among its peers, which provides for greater user experience.

Cost and technological advantage aside, however, what really draws users to the app is its easy and intuitive interface.

Dropbox’s platform is easy to navigate and is compatible with third-party apps such as Zoom, Trello, Salesforce, and Adobe. The company also has a partnership with Google and Microsoft, giving premium subscribers the option to integrate with Google Drive and Office 365.

Moreover, being platform-agnostic, the app can operate in any operating system. While some competitors such as Apple have created an ecosystem that’s user-restrictive where files can only be shared from one Apple device to another, Dropbox offers a solution that allows for instant file sharing across any device.

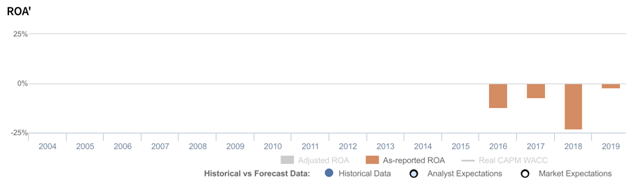

Dropbox has penetrated the cloud market by competing on simplicity and value. However, looking at as-reported metrics, it seems that the company has yet to turn in a profit even with its massive user base and successful competitive strategy.

In reality, being a highly-efficient alternative to other complicated cloud platforms, Dropbox has produced robust returns that inflected positively as early as 2016.

A source of the distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

Dropbox materially spends on R&D as it continues to make investments to enhance its platform and scale its business. The company’s R&D spend has consistently been about 50% of total operating costs, significantly distorting the company’s profitability.

After adjustments, we can see that Dropbox’s Uniform ROA is, in fact, positive and is materially higher than as-reported ROAs. Without this adjustment, it appears that the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Dropbox’s earning power is actually more robust than you think

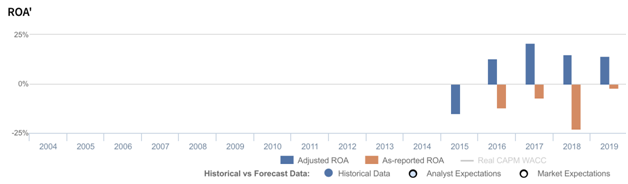

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

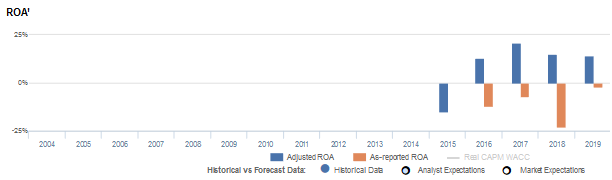

Dropbox’s Uniform ROA has actually been higher than its as-reported ROA in the past four years. For example, as-reported ROA was -2% in 2019, but its Uniform ROA was actually higher at 14%.

Historically, Dropbox’s Uniform ROAs have ranged from -15% to 21% while as-reported ROAs ranged only from -23% to -2% in the same timeframe. After rising from -15% in 2015 to a peak of 21% in 2017, Uniform ROA gradually declined to 14% in 2019.

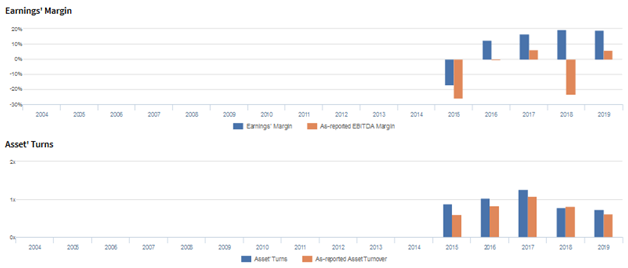

Dropbox’s Uniform earnings margins are stronger than you think

Dropbox’s improvement in profitability has been driven by improvements in Uniform earnings margins, slightly offset by declines in Uniform asset turns.

From 2015-2018, Uniform earnings margins improved from -17% to a peak of 20%, before slightly dropping to 19% in 2019.

Meanwhile, Uniform turns gradually improved from 0.9x in 2004 to a peak of 1.3x in 2017, before declining to 0.7x in 2019.

At current valuations, markets are pricing in an expectation for Uniform margins and Uniform turns to continue declining.

SUMMARY and Dropbox Tearsheet

As the Uniform Accounting tearsheet for Dropbox, Inc. (DBX) highlights, the Uniform P/E trades at 21.2x, which is below corporate average valuation levels but above its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Dropbox, the company has recently shown a 1% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dropbox’s Wall Street analyst-driven forecast is a 41% EPS growth in 2020, followed by a 16% EPS shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dropbox’s $21 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 8% each year over the next three years to justify current prices. What Wall Street analysts expect for Dropbox’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Dropbox’s Uniform earnings growth is above its peer averages in 2020, but the company is trading below its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com