This broadcasting company’s TRUE margins is half what as-reported metrics show, indicating it’s not just political headwinds it needs to contend with

In the past six months, the Philippines’ largest media company has been in the news, with the firm’s franchise renewal coming under intense political scrutiny. The government moved to shut down the company’s broadcasting operations, causing its stock price to decline further.

Although it’s sensible to be wary of the macroeconomic and political headwinds impacting the company’s performance, one must also be wary of the distortions that are found within the as-reported financials.

Uniform Accounting reveals that this company isn’t as efficient at managing expenses compared to what as-reported metrics reflect.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

As the oldest and farthest reaching television broadcaster in the country, ABS-CBN gained popularity for hosting beloved award-winning programs. Their top programs include telenovela Ang Probinsyano, news broadcast TV Patrol, variety show It’s Showtime, and talent show Pilipinas Got Talent.

Besides television, ABS-CBN is known for its radio broadcasting networks such as DZMM Radyo Patrol. The firm has also expanded in the entertainment business with its production company Star Cinema.

The combination of all the mentioned businesses led ABS-CBN to dominate the media and entertainment industry, with an audience share of 54% in 2018. Yet despite the company’s leading market position, average Uniform profitability has only hovered near the 6% global corporate average.

Furthermore, ABS-CBN’s performance has been volatile due to the firm’s sensitivity to political headwinds and tailwinds.

During the Marcos regime, ABS-CBN’s stations were turned over to the government as part of the seizure and closure of private media. Meanwhile, the firm’s outperformance over the more recent years in 2004, 2010, 2013, and 2016 have come as a result of political advertisements from the general elections.

With the recent 2019 general elections, analysts are expecting ABS-CBN’s Uniform ROA to recover from a historical low. However, the company’s recovery is expected to be short-lived, with analysts forecasting 2020 Uniform ROA to fall to negative levels amidst the massive political headwind that is jeopardizing the company’s core operations.

As per law, broadcasting networks require a 25-year congressional franchise to operate. Although ABS-CBN had been requesting its 2020-expiring franchise to be renewed as early as 2014, their initiatives were unsuccessful.

With the expiration of the franchise on March 30, 2020, the National Telecommunications Commission (NTC) issued a cease-and-desist order on ABS-CBN, putting a halt to the company’s broadcasting operations.

Further renewal attempts post-expiration have so far been unsuccessful, with the House Committee on Legislative Franchises voting 70-11 against ABS-CBN’s franchise application last July 10, 2020.

Now, ABS-CBN is appealing to the Supreme Court to prohibit the cease-and-desist order of the NTC. However, the hearing has yet to commence.

Given the persisting political headwind, ABS-CBN’s stock price has been on a consistent downtrend since 2016. Moreover, there is no recent financial information on the company as its 2019 annual report has yet to be released. The firm had already delayed its release twice and may need to delay its filings again as a result of the recently announced worker layoffs.

Investors who are still optimistic about ABS-CBN’s ability to weather these headwinds may look at the company as a value stock, especially when the latest as-reported metrics are showing a 4.6x Fwd P/E and a 15.4% as-reported EBITDA margin.

However, Uniform Accounting teaches us to not just be cautious about the external factors affecting the company, but also the accounting distortions affecting the company’s real core performance.

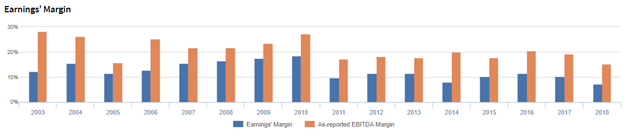

ABS-CBN’s Uniform earnings margin is actually just 7.3% in 2018, less than half of the 15.4% as-reported EBITDA margin. One of the main factors bloating the company’s earnings is how the Philippine Financial Reporting Standards (PFRS) treats depreciation.

In one of our past articles, we’ve talked about the distortion caused by failing to adjust Property, Plant, and Equipment (PP&E) for inflation. Allowing the distortion materially understates the firm’s fixed assets over time and, in doing so, similarly understates the depreciation a company charges on the income statement.

When adjusting PP&E for inflation, ABS-CBN has actually been recognizing PHP 7.5 billion less in fixed assets. This, in turn, has led the firm to charge PHP 1.1 billion less in depreciation expenses.

By applying this adjustment together with other necessary adjustments that Valens makes, we arrive at ABS-CBN’s TRUE earnings margin of 7.3%, not 15.4%.

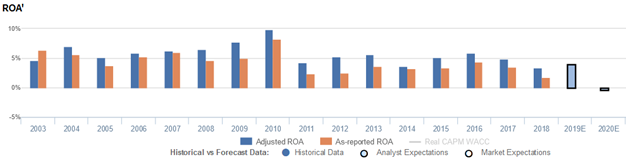

Analyst expectations are for ABS-CBN’s earning power to see unprofitability

ABS-CBN currently trades at a historical high relative to Uniform earnings, with a 90.7x Uniform P/E (Fwd V/E’). Analysts have bearish expectations even at this valuation, projecting Uniform ROA to decline to negative levels by 2020 due to political headwinds.

Historically, ABS-CBN has seen cyclical profitability as a result of political advertising driving the firm’s outperforming years.

Uniform ROA rose to cyclical peaks during election years: 7% in 2004, 10% in 2010, and 6% in 2013 and 2016. Meanwhile, Uniform ROA fell to cyclical lows in the years after the elections at 5% in 2005, 4% in 2011 and 2014, and 3% in 2018.

ABS-CBN’s earnings margin is weaker than you think

Since 2003, as-reported metrics have significantly overstated ABS-CBN’s margins, a key driver of profitability.

Uniform earnings margin improved from 12% in 2003 to 15% in 2004, before compressing to 11% in 2005 and rebounding to a peak of 18% in 2010. Thereafter, Uniform margins fell to 10%-12% levels through 2017, excluding an 8% underperformance, before declining further to 7% in 2018.

Meanwhile, after contracting from a high of 28% in 2003 to 16% in 2005, as-reported EBITDA margin jumped to 22%-25% levels in 2006-2009 and expanded to 27% in 2010. Subsequently, as-reported EBITDA margins dropped to 17%-21% levels from 2011-2017, before fading further to a low of 15% in 2018.

Given analyst expectations, Uniform earnings margin is on pace to drop to negative levels by 2020.

SUMMARY and ABS-CBN Corporation Tearsheet

As the Uniform Accounting tearsheet for ABS-CBN highlights, the Uniform P/E trades at 90.7x, which is far above corporate average valuation levels and its own history.

High P/Es require high EPS growth to sustain them. In the case of ABS-CBN, the company has recently shown a 40% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, ABS-CBN’s sell-side analyst-driven forecast calls for a 38% Uniform EPS growth in 2019 followed by a Uniform EPS decline of 146% in 2020.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ABS-CBN’s PHP 14.78 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings shrink by 1% each year over the next three years and still justify current valuations. What sell-side analysts expect for ABS-CBN’s earnings growth is far below what the current stock market valuation requires.

The company’s earning power is below the long-run corporate average. In addition, cash flows and cash on hand will fall short of its total obligations—including debt maturities, capex maintenance, and dividends—starting 2023. Together, this signals high credit and dividend risk.

To conclude, ABS-CBN’s Uniform earnings growth is above peer averages. However, the company is trading the highest among its peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com