This company bucks the fast fashion trend by using slow fashion to bring in a strong 14% Uniform earning power!

One industry heavily affected by the COVID-19 pandemic in the Philippines is retail, specifically non-essential items like apparel.

Although this company’s operation has been disrupted by the community quarantine, they have pledged a PHP 10 million donation to SM Foundation, Inc. to offer food assistance to communities hit hard by the disease, as well as to purchase personal protective equipment for frontliners.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Fast fashion is used to describe clothing designs that are primarily dependent on current or new trends. These designs are moved quickly from the catwalk to stores.

The rise of fast fashion has made dressing up for any occasion easier for more people. It has made extensive clothing selections available to a wider customer base, often at more affordable prices. However, this usually comes at a cost.

To compete in the fast fashion space, companies have to design and manufacture clothing at the quickest time possible. Instead of the standard two-fashion seasons, Spring/Summer and Fall/Winter lines, fast fashion popularized “micro-trends” or “micro-seasons.”

In a market that prioritizes keeping up with the quickly changing trends, the quantity of collections became more important than their quality. In order to be profitable in this space, companies needed cheaper ways to manufacture their garments.

According to a Forbes article written by environmental scientist James Conca, over 400% more carbon emissions per item each year is produced because of fast fashion. Cheap synthetic fibers that helped these companies keep costs low emitted more dangerous gases such as nitrogen oxide, which is said to be 300 times more damaging than carbon dioxide.

Additionally, since fast fashion garments are not designed to last a long time, people usually end up disposing them sooner rather than later.

Fast-changing seasons and trends prove that fashion fades. Nevertheless, with today’s growing concerns regarding sustainability, this brand believes that clothing shouldn’t be just a fad. Neither should it be detrimental to the environment.

Uniqlo, a Japanese brand owned by Fast Retailing, is a clothing store that debunks the notion that it’s a fast fashion company.

The company is named Fast Retailing not because it’s a fast fashion company, but because of how quickly their brand innovates.

Uniqlo belongs in the slow fashion industry, where companies are trying to address the environmental, social, and economic issues surrounding fast fashion through employing sustainable manufacturing processes.

With the brand’s mission to provide high-quality basic casual wear that can be worn anytime and anywhere, Uniqlo introduced the concept of LifeWear, which focuses on simple, high-quality, everyday clothing designed to make everyone’s lives better.

This encapsulates the brand’s philosophy “Made for All,” which highlights that apparel transcends age, gender, ethnicity, and all other ways to define people.

Uniqlo challenges fast fashion by giving timeless basics and essentials that are affordable as opposed to instantly responding to fast-changing fashion trends.

Unlike the business model adopted by fast fashion, Fast Retailing founder and CEO Tadashi Yanai has expressed that they do not make disposable clothes.

CEO Yanai is also fond of saying that “Uniqlo is not a fashion company, it’s a technology company.” True to his word, the company has provided its customers with “wearable technology” such as the HEATTECH, AIRism, and DRY-EX lines.

The HEATTECH line is designed to keep you warm in cold climates by generating and retaining the heat from your body. On the other hand, the AIRism line keeps you cool and dry in the summer by absorbing moisture and releasing heat. Similarly, the DRY-EX line is made of highly functional fabric that absorbs and wicks away your sweat.

Uniqlo shows that it continuously uses proprietary innovation to keep people stylishly comfortable.

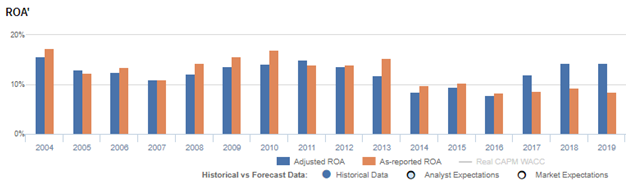

Even with the company’s differentiation and product innovation, as-reported returns for the past three years have been weak at just 8%-9% levels, which is far behind its true earning power.

Fast Retailing’s real economic profitability can be better reflected with Uniform Accounting adjustments.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base before looking at its performance metrics, the company’s profitability and capital efficiency may appear substantially weaker than it actually is.

After excess cash and other significant adjustments are made, Fast Retailing reported a 14% Uniform ROA in 2019, which is materially stronger than as-reported ROA of 8%.

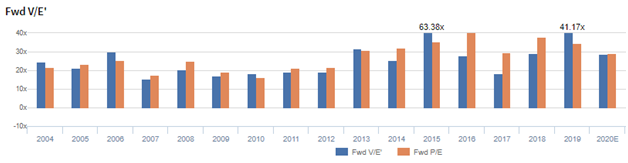

Although the company isn’t cheap at a 28.6x Uniform P/E, strong forecast earnings growth can justify these valuations.

Fast Retailing’s Uniform valuation is in line with the market

Fast Retailing Co., Ltd. (9983:JPN) currently trades above corporate averages with a 28.6x Uniform P/E (blue bars), but in line with the as-reported P/E of 29.0x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to expand to 18% in 2024, accompanied by a 2% Uniform asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to remain at 14% in 2021, accompanied by 2% Uniform asset shrinkage.

Fast Retailing’s profitability is actually better than you think it is—and improving

As-reported metrics are understating Fast Retailing’s profitability.

For example, as-reported ROA was 8% in 2019, lower than Uniform ROA of 14%. Uniform ROA has been higher than as-reported ROA in the past three years.

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Fast Retailing’s Uniform ROA ranged from 8% to 16% over the past 16 years. After dropping from a peak of 16% in 2004 to 11% in 2007, Uniform ROA rose to 15% in 2011. Afterwards, Uniform ROA dropped to a historical low of 8% in 2016, before rebounding back to 14% in 2019.

Fast Retailing’s margins are weaker than you think, but asset turnover makes up for it

Cyclicality in Uniform ROA has been primarily driven by trends in Uniform earnings margin, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margin decreased from a historical high of 12% in 2004 to 8% in 2007, before recovering to 10% in 2011. Thereafter, Uniform earnings margin fell to 5% in 2016, before rising to 9% in 2018-2019.

Meanwhile, after trending at 1.2x to 1.4x levels from 2004 to 2010, Uniform asset turns rose to 1.5x in 2011, before contracting to 1.0x in 2015. Since then, Uniform asset turns have recovered to 1.7x in 2019.

Summary and Fast Retailing Tearsheet

As the Uniform Accounting tearsheet for Fast Retailing highlights, they are trading at 28.6x Uniform P/E, which is above market average valuations and around historical P/E of 29.4x.

High P/Es require high EPS growth to sustain them. In the case of Fast Retailing, the company has recently shown a 3% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Fast Retailing’s sell-side analyst-driven forecast is for Uniform earnings to decline by 18% in 2020 and then grow by 33% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 41,570 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Fast Retailing, the company would have to have Uniform earnings grow by 4% each year over the next three years. What sell-side analysts expect for Fast Retailing’s earnings growth is well above what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is almost 2x greater than corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Fast Retailing has low credit and dividend risk.

To conclude, Fast Retailing’s Uniform earnings growth is below peer averages in 2020 and it is trading above peer average valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com