This company continues to grow its family of convenience stores while growing its TRUE earning power to 17%, not just 2%!

We are now in the third week of the enhanced community quarantine for Luzon that President Duterte declared as part of the government’s plans to battle the spread of the novel coronavirus.

Restrictions during the quarantine mandated the temporary suspension of operation of non-essential businesses. Supermarkets and convenience stores are among the few places that remain open where people can purchase food and other essentials during the quarantine.

This Japanese convenience store chain, known for its homey ambiance and friendly service, remains open in key areas in Metro Manila to serve the people during the pandemic.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Sari-sari stores can be found almost everywhere in the Philippines. They are usually run by a family to generate some income by selling a variety of products such as candies, canned goods, beverages, cigarettes, and more.

Goods in sari-sari stores are normally a little more expensive than the same ones you can find in supermarkets, but that has not stopped Filipinos from buying again and again from their neighborhood store.

The value of these stores is in their convenience—in terms of their location and in the sizes of what can be purchased.

People usually buy from sari-sari stores when they need to purchase just a few items or in smaller quantities or sizes (tingi-tingi) than what they might find in supermarkets. They might even prefer purchasing at these stores because they can do so on credit, especially if they know the family running the business.

Some Filipinos even stay at their favorite sari-sari stores to hang out with their friends and neighbors. Since these stores are usually lined with benches at the front, they offer people a casual place to gather and just exchange stories.

For a lot of Filipinos, sari-sari stores aren’t just another business; they’re part of the Filipino culture.

It’s not surprising then that when convenience stores emerged in the country, consumers also became repeat customers. Products at convenience stores are normally more expensive than those in sari-sari stores, but they can charge at that price point because of the extra level of convenience they offer.

Being open 24/7 has allowed convenience stores to capture the late-night-to-early-morning market that other store formats have not catered to.

In the Philippines, 7-Eleven, Mini Stop, Lawson, FamilyMart, and All Day are examples of well-known convenience stores.

FamilyMart is the first Japanese-owned convenience store retail chain to go global. It is now the second largest convenience store chain in the world, having over 18,000 stores in Asia alone.

In 2013, the Philippines became the newest member of this convenience store’s family. After only two years, FamilyMart was able to expand to more than 60 branches in Metro Manila.

FamilyMart brands itself as having a familial, fast, and friendly service by treating its customers as part of their family. This serves to be on-brand for Filipinos, who have long become accustomed to the sari-sari store way of bringing people together.

Its competitive advantage lies in their “cafe-like” experience where customers are provided with a seating area where they can enjoy their meals, rest, or have a chat with their family and friends.

This is different from the usual convenience stores where people usually just take what they need from the shelves, pay for it, and leave.

FamilyMart then took this unique experience to the next level when it opened its biggest branch in the country in November 2019.

This new branch in Udenna Tower, Bonifacio Global City, promotes their vision of becoming an essential part of people’s everyday lives because it now has a co-working space, meeting rooms, and a videoke room.

Instead of meeting or working in expensive restaurants and cafes, people can enjoy a simple place such as in their new branch. Friends and families may now celebrate at this one-of-a-kind convenience store.

Moreover, while FamilyMart already provides ready-to-go “gourmet” food, this new branch now offers snacks that you could only find in Japan’s FamilyMart branches such as onigiri, donburi, and ramen.

FamilyMart has done well branching out to ASEAN countries thanks to its business model that is built around understanding the demographics within the specific country.

They understand that each country has its own set of people and cultures that may affect how the business is run. They also understand that they shouldn’t lose touch with their roots. As a result, FamilyMart thrives by incorporating the Japanese culture with that of the country the retail chains reside in.

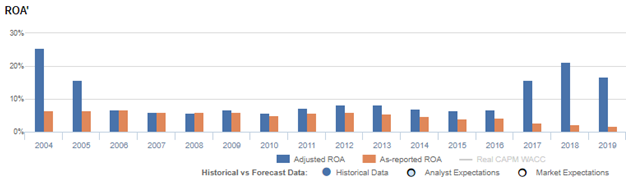

Even with the company’s effective business model and unique store offerings, as-reported returns for the past three years have been weak at just 2%-3% levels, which is far behind its true earning power.

FamilyMart’s real economic profitability can be better reflected with Uniform Accounting adjustments.

For the last three years, Uniform metrics show returns a lot stronger than what as-reported data state, with Uniform ROA being 5x to 10x more robust than as-reported ROA.

What as-reported data fails to do is to consider pension and OPEB cost as non-cash expenses. These are not operating expenses. When as-reported accounting includes these as expenses, earnings are incorrectly reduced, and profitability is incorrectly lower than it should be.

In reality, pension and OPEB costs are simply actuarial adjustments, not operating expenses, and Uniform Accounting adds these back.

After pension and other necessary adjustments are made, FamilyMart reported a 17% Uniform ROA in 2019, much higher than as-reported ROA of 2%.

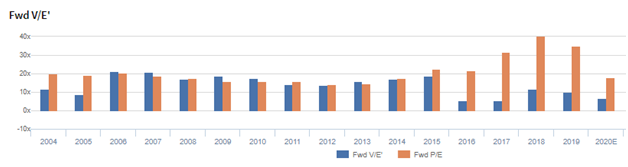

FamilyMart’s Uniform valuation is cheaper than what the market thinks

FamilyMart Co., Ltd. (8028:JPN) currently trades well below corporate averages with a 6.6x Uniform P/E (blue bars) and an as-reported P/E of 18.1x (orange bars). At these levels, the market is pricing in expectations for Uniform ROA to fall to 6% in 2024, accompanied by a 9% Uniform asset growth going forward.

However, analysts have more bullish expectations, projecting Uniform ROA to increase to 23% levels in 2021, accompanied by a 9% Uniform asset shrinkage.

FamilyMart’s profitability is actually better than you think it is

As-reported metrics are understating FamilyMart’s profitability.

For example, as-reported ROA was 2% in 2019, lower than Uniform ROA of 17%. Uniform ROA has been higher than as-reported ROA in fourteen of the past sixteen years.

As-reported metrics distort the market’s perception of the firm’s historical profitability trends. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

FamilyMart’s Uniform ROA ranged from 6% to 25% over the past sixteen years. From a historical high of 25% in 2004, Uniform ROA plunged to 6% in 2007-2008. It remained in the 6% to 8% levels in 2009 to 2016, and then doubled in 2017. Uniform earning power grew to 21% in 2018 and then returned to 17% in 2019.

Summary and FamilyMart Tearsheet

As the Uniform Accounting tearsheet for FamilyMart highlights, they are trading at 6.6x Uniform P/E, which is below market average valuations but around historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of FamilyMart, the company has recently shown a 44% decline in Uniform EPS.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, FamilyMart’s sell-side analyst-driven forecast is for Uniform earnings to grow by 30% in 2020 and 2% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 1,892 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of FamilyMart, the company would have to have Uniform earnings shrink by 20% each year over the next three years. What sell-side analysts expect for FamilyMart’s earnings growth is well above what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is 3x greater than corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, FamilyMart has low credit and dividend risk.

To conclude, FamilyMart’s Uniform earnings growth is above peer averages in 2020. Moreover, the company is trading lower than peer average valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com