This company doesn’t play games with its 180% earning power. They are also much cheaper at 20x Uniform P/E, not 28x.

Online games have been gaining popularity in the Philippines, given the country’s young demographics who are avid internet users. According to a survey done by PUBLiCUS Asia Inc., 81.6% of millennials aged between 23 and 28 play online games, 55.8% of which classifying themselves as competitive gamers.

While other game developers still need to translate their games to different local languages, there’s barely any need for that in the Philippines since most Filipinos can understand English. This lack of language barrier made it easy for a vast collection of online games to proliferate in the country.

This company has developed several top-grossing online games that Filipinos are hooked into, and you won’t believe how cheap it really is compared to what the market thinks!

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Tearsheet & Embedded Expectations

Powered by Valens Research

Esports, or competitive video gaming, are often played in front of live audiences and may also be broadcasted. Much like an athletic sports event, esports have rules, referees, and commentators.

Esports made its debut in the 30th Southeast Asian Games (SEA Games) on December 5, 2019. It was the first time an esports competition was considered a medal event in a multisport competition allowed by the International Olympic Committee.

The Philippine team, with 27 players, battled against the best professional gamers in South East Asia in six events divided into three categories: PC, console, and mobile.

Dota 2, Hearthstone, and StarCraft II were the events under the PC category; Mobile Legends Bang-Bang and Arena of Valor in mobile category; and Tekken 2 fell under the console category.

The event concluded with the Philippine team taking home the most number of medals in esports, with three gold, one silver, and one bronze. Thailand came in second with two gold and two silver medals.

One particular esport event was made possible because of Tencent Games.

Arena of Valor, or AOV, was published by Tencent Games for iOS, Android, and Nintendo Switch, even for markets outside mainland China.

This game is a multiplayer online battle arena (MOBA) for mobile.

MOBA games are usually played with ten players divided into two teams having five members each. The goal is to beat your opponent by destroying their base.

Tencent has been really successful in this genre. Apart from AOV, they also developed and published popular games such as League of Legends and King of Glory.

They have also enjoyed success in other genres with titles like PUBG, Call of Duty, Chess Rush, and Monster Hunter.

According to Sensor Tower, the highest-grossing game for December 2019 is PUBG Mobile, followed by Honor of Kings. Both are Tencent-owned games.

It’s no wonder they have shown a solid, significant Uniform return on assets (ROA) in the past 15 years.

Central to their earnings growth is their acquisitions and controlling stakes in various industries.

One of their biggest deals was in 2016, when Tencent paid $8.6bn for a majority stake in Supercell, known for Clash of Clans and Clash Royale.

The company also has investments in different gaming companies including Riot Games, Epic, Ubisoft, Frontier, Miniclip, and Paradox.

Recently, Tencent made an offer to acquire Funcom, the game company that developed Conan Exiles and 28 other titles.

Although they are more widely known globally for their online games, Tencent also provides various services such as online advertising, instant messaging, mobile value-added services, and other interactive entertainment services.

They recently announced new initiatives for WeChat, their instant messaging app. They aim to fully monetize the app by launching more customized tools on the platform.

Tencent Holdings Limited is cheaper than you think

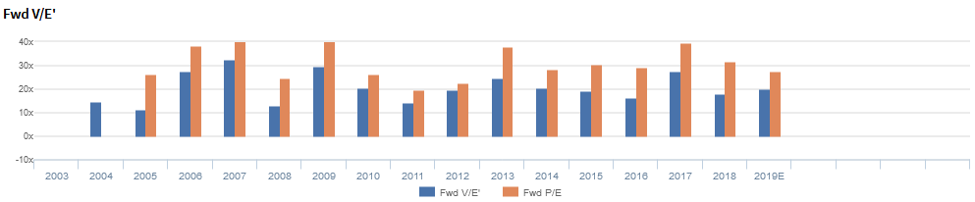

Tencent (700:HKG) currently trades around recent averages with a 19.8x Uniform P/E (blue bars). As-reported P/Es (orange bars), on the other hand, show Tencent as being more expensive at 27.6x.

At these levels, the market is pricing in expectations for Uniform ROA to fall from 180% in 2018 to 75% in 2023, accompanied by 25% Uniform asset growth going forward.

Moreover, analysts have less bearish expectations, projecting Uniform ROA to drop to 162% in 2019, accompanied by 29% Uniform asset growth.

Tencent’s earning power is actually better than you think

Tencent’s profitability is cyclical, with Uniform ROA ranging from 71% to 268% over the past 15 years.

Uniform ROA fell from 141% in 2004 to a historical low of 71% in 2007, before rebounding to 154% in 2010. After Uniform ROA decreased to 79% in 2011, it rose to a peak 268% in 2017, then dropped to 180% in 2018.

As-reported metrics are understating Tencent’s profitability.

For example, as-reported ROA was near 8% levels in 2019, a far cry from the Uniform ROA of 180%, making the company look like a weaker business than real economic metrics highlight. Moreover, as-reported ROA has been below Uniform ROA for the past 15 years, significantly distorting the market’s perception of the firm’s historical profitability trends.

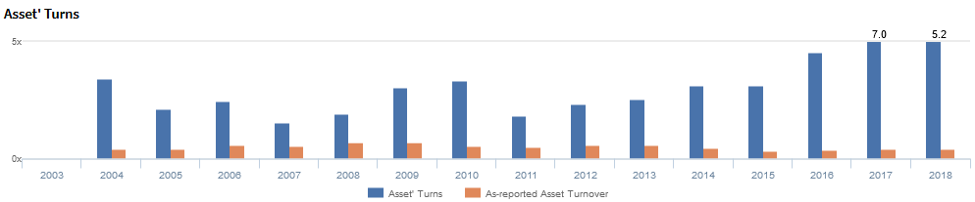

Tencent’s asset turns are stronger than you think

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

After dropping from 3.4x in 2004 to a historical low of 1.5x in 2007, Uniform asset turns rebounded to 3.3x in 2010. Thereafter, Uniform asset turns fell to 1.9x in 2011, before slowly rising to a peak of 7.0x in 2017 and eventually falling back to 5.2x in 2018. At current valuations, markets are pricing in expectations for Uniform asset turns to decrease.

SUMMARY and Tencent Holdings Limited Tearsheet

As the Uniform Accounting tearsheet for Tencent Holdings Limited highlights, they are trading at 19.8x Uniform P/E, which is around market average valuations and its recent average levels.

Low P/Es require low EPS growth to sustain them. In the case of Tencent, the company has recently shown an 18% increase in Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Financial Reporting Standards (HKFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Tencent’s sell-side analyst-driven forecast is for Uniform earnings to grow by 20% and 12% in 2019 and 2020, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify HKD 361 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Tencent, the company would have to have Uniform earnings grow by 8% each year over the next three years.

What sell-side analysts expect for Tencent earnings growth is more than enough to justify what the current stock market valuation requires.

To conclude, Tencent’s Uniform earnings growth is around peer averages in 2020. However, the company is trading at above average peer valuations.

The company’s earning power—based on its Uniform return on assets calculation—is 30x the corporate averages. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Tencent has low credit and dividend risk.

About the Philippine Market Daily

“Wednesday Uniform Earning Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; and Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in HKFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com