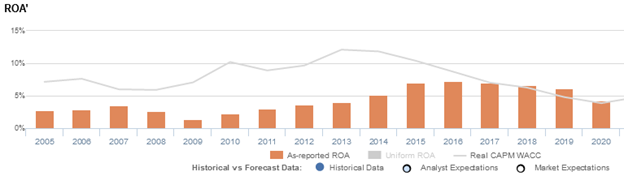

This company is dominating the traditional advertising space, displaying a Uniform ROA that is twice the as reported

In today’s era of smartphones and social media, the Google-Facebook duopoly dominates the advertising space. However, traditional advertising still manages to make people look up from their screens and grab their attention.

This company is one of the largest traditional advertising companies in the world, and it has invested in newer technology to ride the rising digital out-of-home (DOOH) advertising trend.

However, while as-reported metrics make it seem like its traditional advertising business is a losing game, with declining returns in the past five years, Uniform ROAs that are consistently at 8%-9% levels reveal that it still is a profitable space.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In the world of advertising, one of the most important metrics that companies gauge carefully is their “reach.” It refers to the number of consumers exposed to the advertisement—the higher the reach, the higher the probability of the advertisement getting seen by its intended market, and the higher its effectiveness.

However, over the last century, much of the advertising landscape has changed. While newspapers, radios, and TVs used to be the prominent mediums of advertising, now, companies favor advertising through online sites.

This makes a lot of sense. People are spending more time online now more than ever, so if companies are looking for maximum reach, there’s no better place than the internet.

Google and Facebook are dominating the online advertising space, taking up a combined 60% of the total market share. There’s no surprise there—Google has about 4 billion users and Facebook has close to 2 billion. That said, is it worth advertising anywhere else?

Last year, we talked about how billboards were popularized in the 19th century. At first, these were only used to advertise circus acts, but later on, billboards became a standard for businesses to advertise different products like food and clothing.

In this digital age, one may think that advertising on billboards is obsolete. However, technology has only enhanced this mode of advertising, allowing an innovative transition from out-of-home (OOH) advertising to digital out-of-home (DOOH) advertising.

While forms of OOH advertising include your run-of-the-mill outdoor ads like billboards and public transit ads, DOOH advertising is basically a digitized version that creates more value for brands and its audiences. An example of this would be the LED displays that we previously discussed with China’s AOTO Electronics Co., Ltd.

Brands and media buyers are utilizing DOOH advertising because the software behind these digital displays allow them to monitor and track the content in real time. Moreover, because DOOH advertising provides audience insight, the ads are effectively managed in terms of what is displayed and when a certain ad is displayed.

Still, is this better than online advertising?

Digital billboards are strategically located in high foot traffic places. Additionally, while we have the ability to dodge ads on our devices through ad blockers or simply skipping them, DOOH ads do not have these capabilities, and they are designed to capture the audience’s attention.

The company we are highlighting today knows that this is its competitive edge over online advertisers. Lamar Advertising (LAMR) is one of the largest outdoor advertising companies in the world, with more than 350,000 displays across the U.S. and Canada.

While Lamar already specializes in OOH advertising, such as billboards, logo signs, and transit displays, the company has also made investments to expand its DOOH business. Currently, Lamar has the largest network of digital billboards in the U.S with about 3,600 displays.

In a highly fragmented industry, Lamar continues to be a leading provider of outdoor advertising in the markets it serves. Moreover, the company continues to strengthen its position as one of the largest logo sign operators by acquiring new franchises, as well as other companies.

However, looking at as-reported metrics, it appears that Lamar is struggling to compete with online advertisers, with return on assets (ROA) that have consistently been below the company’s cost of capital.

In reality, Uniform Accounting displays a more accurate picture, with a Uniform ROA that is double the as-reported in 2020. This shows that even though online mediums have the most reach, there is still something to be argued for traditional OOH advertising. So long as people are outside, there will be a place for physical advertising.

The distortion comes from as-reported metrics failing to consider the number of operating leases Lamar has from the production facilities, vehicles, and other sites at which its advertising structures are built.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, would not be treated as an investment, but as an expense that would impact the income statement.

Specifically, operating leases on Lamar’s income statement are understating the company’s true earnings. Adjusting for the rent expense distortion, which historically has been about one-third of its total operating expenses, returns are actually stronger.

As a result, as-reported ROAs are not capturing the strength of Lamar’s earning power. Adjusting for operating leases, we can see that the company’s profitability isn’t actually weak, with Uniform ROAs above cost of capital at 8%.

Lamar is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Lamar’s Uniform ROA has actually been higher than its as-reported ROA in thirteen of the past sixteen years. For example, Uniform ROA was 8% in 2020 while as-reported ROA was only at 4%.

Specifically, Lamar’s Uniform ROA has ranged from 2%-9% in the past sixteen years while as-reported ROA ranged only from 1%-7% in the same timeframe.

Uniform ROA decreased from 4% levels in 2006-2007 to 2% in 2008, before rebounding to 4% in 2009 and compressing to 3% in 2010. Then, Uniform ROA gradually elevated to 8%-9% levels through 2020.

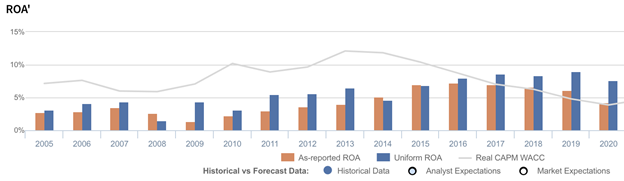

Lamar’s Uniform earnings margin is weaker than you think, but has steadily increased through 2020

Improvements in Uniform ROA have been driven primarily by Uniform earnings margin expansion.

Uniform margins expanded from 7% in 2005 to 11% in 2007, before collapsing to 4% in 2008 and recovering to 21% in 2013. Then, after declining to 15% in 2014, Uniform margins gradually improved to 36%-37% levels in 2018-2020.

SUMMARY and Lamar Advertising Company Tearsheet

As the Uniform Accounting tearsheet for Lamar Advertising Company (LAMR:USA) highlights, the Uniform P/E trades at 28.5x, which is above the global corporate average of 25.2x and its historical Uniform P/E of 26.0x.

High P/Es require high EPS growth to sustain them. In the case of Lamar, the company has recently shown a 17% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lamar’s Wall Street analyst-driven forecast is an 8% and a 12% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lamar’s $95 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 7% per year over the next three years. What Wall Street analysts expect for Lamar’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is in line with the corporate average. Also, cash flows and cash on hand are slightly higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Lamar’s Uniform earnings growth is above its peer averages, but the company is also trading below its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com