This company is setting “face ID” as the new standard to combat online identity fraud, allowing it to earn Uniform ROAs of 20%+ in the process

Financial institutions are always on the lookout for fraudulent transactions and identity scams. Especially now that more and more financial transactions are done online, it makes it more complicated for companies to detect digital fraud.

Thankfully, this company’s mobile identity verification system provides a solution to the growing fraud problem.

However, while as-reported ROAs make it seem that this solution isn’t as important as it should be, Uniform ROAs that have been up to 20x stronger would argue the opposite.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

They say that money makes the world go ‘round…and it’s true.

Valued at over $20 trillion, the global financial services market is the largest industry in the world, and arguably the most important.

The pace of growth in this industry has accelerated over the past decades as more investments are made toward financial technology (or fintech). We are now able to borrow capital, transfer money, and make investments online thanks to AI, cloud computing, and other tech advancements.

However, the growth in digital finance also came with significantly more risks, including cyber hacks, increased money laundering schemes, and identity theft.

Identity theft and fraud is especially rampant. In 2019, one in fifteen people were victims of identity theft, with a staggering 33% of U.S. adults having experienced identity theft once in their lives.

These attacks inflict an emotional toll on those forced to reclaim their identity from scammers and hackers. The economic toll is just as damaging as well—losses from fraud have climbed to $3.3 billion in 2020 from just $1.9 billion in the year prior.

It’s a massive issue for both individuals and companies, from lost revenue to livelihoods destroyed. Scammers have the ability to forge legal documents, engineer passwords to gain access to secure websites, or make a direct attack on a company’s database for valuable information or ransom funds.

Thankfully, there are companies like Mitek Systems (MITK) that create solutions to combat fraud.

Mitek’s core business is in mobile check deposits…and it owns roughly 98% of the market share in this space. So anyone who has ever taken a photo of a check to be deposited to their bank is most likely using the company’s system.

In total, Mitek has processed more than four billion mobile deposits and $1.5 trillion in cumulative check value through its platform, and that number continues to grow every day.

Which is why, for a company handling that many mobile transactions, it is imperative that measures against fraud are put in place—this is where Mitek’s digital identity verification business, Mobile Verify, comes in.

Mobile Verify is built on a biometric facial comparison tool that compares a user’s face on live camera to the pictures on file, or to a government-verified ID that’s provided at the same time.

Through analytics based on AI, the system can corroborate the results, block fraudulent attempts, and allow users access to their sensitive data or transactions.

Mobile Verify has seen a similar surge in demand to the Mobile Deposit business, as people have had a much harder time interacting face-to-face over the past year due to lockdowns.

Furthermore, other than individual mobile check depositors, Mobile Verify also serves other organizations, ranging from the government to large corporations such as Airbnb, Adobe, and Morgan Stanley.

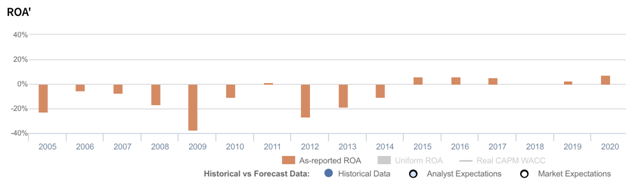

The combination of Mitek’s monopolistic hold on the mobile check deposits market and its fast-growing digital identity verification business would imply lucrative returns for the company. However, looking at as-reported metrics, this doesn’t seem to be the case.

As-reported return on assets (ROAs) have inflected positively in 2015—when the company started earnings profits—with below cost of capital returns ranging from 0%-8%.

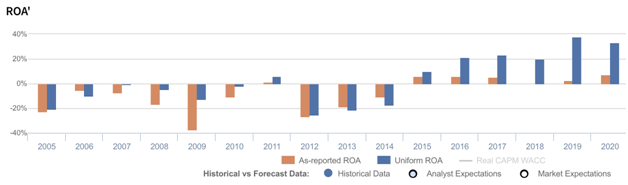

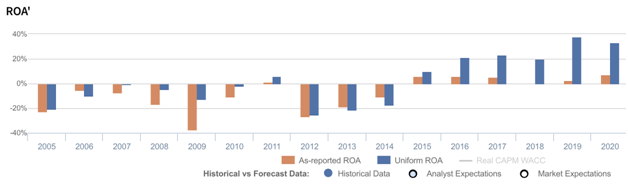

In reality, Uniform Accounting shows profitability levels that have been much stronger. Uniform ROAs have ranged from 10%-38% over the same time frame, showing a more accurate result of Mitek’s increasing adoption rates and growing scale.

The distortion comes from as-reported metrics incorrectly treating R&D as an expense. In recent years, Mitek’s R&D expense stood at around $23 million, about one-fourth of its total operating expenses.

In reality, R&D is an investment in the long-term cash flow generation of the company. Recording R&D as an expense violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is reported.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

As in the case of Mitek, as-reported ROAs are not capturing the true strength of the company’s earning power. Adjusting for R&D, you get returns that are greater than what is actually shown. Without this adjustment, it would appear that Mitek had been less successful with its R&D investments than it really is, leading to poorer valuations.

Mitek’s earning power is significantly more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Mitek’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, Uniform ROA was at 33% in 2020 while as-reported ROA was four times weaker at 8%.

Specifically, Mitek struggled to earn a profit from 2005-2014, with Uniform ROAs ranging from -26% to -1%, excluding outperformance in 2011. Uniform ROA has since inflected to positive levels in 2015, with a Uniform ROA at 10% that has expanded to 20% levels in 2016-2018. Since then, Uniform ROA has jumped to a peak of 38% in 2019 before declining slightly to 33% in 2020.

Mitek’s Uniform earnings margin and Uniform asset turns are driving recent strength in Uniform ROA

Uniform ROA expansion has been driven by trends in Uniform earnings margins, slightly offset by relatively stable Uniform asset turns.

Uniform margins have been largely negative from 2005-2014, ranging from -53% to -1%, excluding outperformance in 2011. Uniform margins have since inflected to positive levels in 2015, before stabilizing at 17%-18% through 2018. Since then, Uniform margins have jumped to peak levels of 35%-38%.

Meanwhile, Uniform turns have remained stable at 0.5x-0.7x levels through 2014 before jumping to 0.9x in 2015. Subsequently, Uniform turns have improved to 1.1x-1.3x levels through 2018, before declining slightly to just 1.0x through 2020.

At current valuations, the market is pricing in expectations for both Uniform margins and Uniform turns to decline from current levels.

SUMMARY and Mitek Systems, Inc. Tearsheet

As the Uniform Accounting tearsheet for Mitek Systems, Inc. (MITK:USA) highlights, the Uniform P/E trades at 25.6x, which is above the global corporate average of 21.9x and its own average historical P/E of 15.7x.

High P/Es require high EPS growth to sustain them. In the case of Mitek, the company has recently shown a 2% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Mitek’s Wall Street analyst-driven forecast is a 23% EPS decline in 2021 followed by a 32% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Mitek’s $21 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 6% annually over the next three years. What Wall Street analysts expect for Mitek’s earnings growth is below what the current stock market valuation requires in 2021, but is above that requirement in 2022.

Furthermore, the company’s earning power is 6x the long-run corporate average. Also, cash flows and cash on hand are 3x its total obligations through 2025—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, Mitek’s Uniform earnings growth is above its peer averages. Therefore, as is warranted, the company is also trading above peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com