This company was one that revolutionized the travel agency industry. Could its Uniform ROA (true earning power) really be 50x higher than most think?

“It’s more fun in the Philippines…” and apparently there is lots of fun elsewhere too.

Travel & Tourism is the fastest growing sector worldwide, with some estimating its growth at 3.9%, outpacing the rest of the global economy set to only grow by 3.2%.

In the US, travel and tourism ranked second in priority for consumers’ discretionary spending. Millennials are even likely to take on debt just to go on a trip.

And because this age group grew up in a time when technology has all but replaced personal human interaction, going on DIY trips and booking online has been the prominent trend globally.

As developments in this sector continue to grow, there is a greater demand for secure and efficient online booking transactions. Here is a company that is viewed as an unprofitable business, but actually earns 50x higher returns based on Uniform ROA.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

“It’s more fun in the Philippines!” was a viral marketing campaign that started in 2012, aimed at attracting more foreign tourists to travel to and within the country. Three years after the campaign began, the number of tourists went up from 4.27 million in 2012 to 5.36 million.

What made the campaign so much more effective was the decision to tap into social media and understand how it affects the public’s consumption behaviours.

This was particularly strategic because 66% of Philippine travelers were made up of 15-34 year olds—the millennials.

It has become common practice for this age group to consult online sources before going on a trip. Online inquiries include looking for the “instagrammable” places, asking for dining recommendations, and searching for safe and convenient accommodations.

The travel industry’s shift from brick-and-mortar agencies to digital domains facilitated the growth in the global tourism industry.

Companies like Booking Holdings, Expedia, and Ctrip took advantage of this transition, providing consumers with accessibility and ease of travelling.

Booking, particularly, is more successful because they use the Agency Model, which allows travel agencies to list services from hospitality establishments and get paid on commission.

The Merchant Model, on the other hand, is where establishments sell to travel agencies in bulk at discounted prices then resell them to customers at a marked-up price.

The Agency Model allows Booking’s operations to be as cost-effective as possible, which is why they are one of the few companies with the best earnings margins versus their industry peers.

In addition, Booking has made a significant number of acquisitions over its operating life.

Booking acquired Agoda (online travel agency), OpenTable (restaurant reservations), Rentalcars (car rental service), Cheapflights (flight comparison search engine), and other travel services companies.

So when their stock price skyrocketed from $40 in 2007 to current $2,000 levels, it was primarily due to their strategic acquisitions and the effectiveness of their business model.

With the public’s increasing desire for local and international experiences, Booking and its many services are well-positioned to soak up the demand for future growth.

However, management appears concerned about the sustainability of the demand for their attractions products, as well as competition in the travel industry.

Given that current ROAs have tapered off from previous years, the market seems to think that this downward trend will continue.

Booking’s earning power is actually more robust than you think

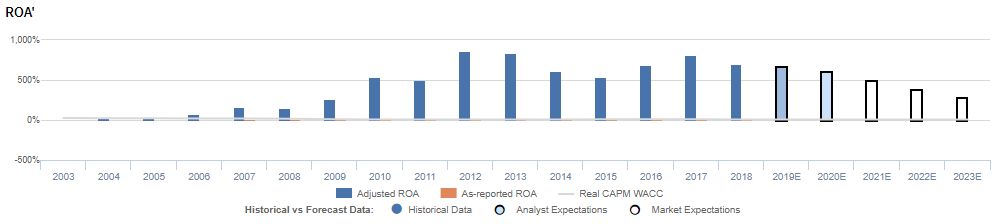

As-reported metrics significantly understate BKNG’s profitability. As-reported ROA for BKNG was near 14% levels in 2018, massively lower than its Uniform ROA of 704%. As-reported ROA makes BKNG appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2015, as-reported ROA has remained at 13%-14% levels, while Uniform ROA increased from 541% to 704% over the same timeframe, significantly distorting the market’s perception of the firm’s historical profitability trends.

Overall, BKNG has seen robust, improving profitability. From 2003-2012, Uniform ROA steadily expanded from -4% to a peak of 860% as they successfully acquired and integrated competitors such as Kayak Corporation.

However, due to the rise of non-hotel accommodation giant Airbnb, and increased competition among other Online Travel Agencies (OTA), Uniform ROA compressed to 541% by 2015.

Since then, however, Uniform ROA had rebounded to 809% in 2017, fueled by successful partnerships in China and their acquisition of Open Table, before compressing slightly to 704% in 2018.

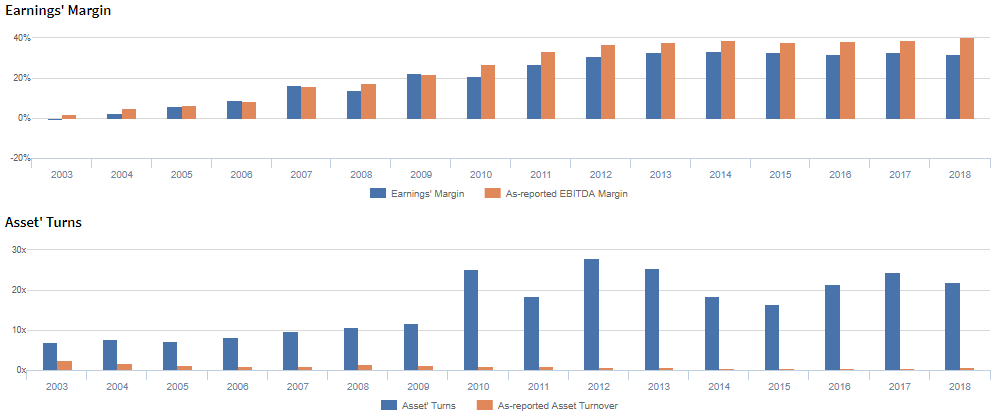

Booking’s earnings margins are in line with Uniform metrics, while asset turns are not

Robust Uniform ROA has been driven by improvements in both Uniform earnings margin and Uniform asset turns.

From 2013 to 2018, Uniform earnings margins steadily improved from -1% in 2003 to 32%-33%.

Meanwhile, Uniform asset turns have been more volatile, improving from 7.1x in 2003 to 11.8x in 2009, before jumping to peak 27.9x levels in 2012. However, Uniform asset turns compressed to 16.4x in 2015, before rising to 24.4x in 2017, and decreasing to 22.0x in 2018.

The as-reported numbers make the company appear to be much less efficient in churning revenue out of their asset base than real economic metrics highlight. It also distorts the market’s perception of the firm’s historical asset efficiency trends.

At current valuations, markets are pricing in expectations for material compression in both Uniform earnings margins and Uniform asset turns.

SUMMARY and Booking Holdings Inc. Tearsheet

As our Uniform Accounting tearsheet for Booking Holdings Inc. (BKNG:USA) highlights, BKNG’s Uniform P/E trades at 16x, well below corporate average valuation levels and in line with historical valuations.

Low P/Es require low EPS growth to sustain them. In the case of BKNG, the company has recently shown a 16% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, BKNG’s Wall Street analyst-driven forecast is a historically high growth of 22% into 2019, which then drops to a no-growth earnings forecast in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $1,974 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of BKNG, the company would have to sustain a 2% decline in Uniform earnings, over the next three years.

What Wall Street analysts expect for BKNG’s earnings growth falls above what the current stock market valuation requires.

To conclude, BKNG’s Uniform earnings growth is in line with peer averages in 2019 but will lag behind peers in 2020. Also, the company is trading at well below average peer valuations. The company has an average earnings power, based on its Uniform return on assets calculation. Together, this signals a low cash flow risk to the current dividend level in the future.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company listed outside of Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com