This company’s continuous growth in renewable energy initiatives has sparked a Uniform ROA of 10%, not 4%

This power company established partnerships and expanded their renewable energy portfolio to stress the importance of continuous improvement in the firm’s operations.

However, as-reported metrics seem to distort this development, only reporting 4% instead of a Uniform return of 10%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The power sector was one of the most affected sectors during the pandemic because of the sharp decline in demand for electricity and gas, as most establishments halted their operations and people stayed at home.

As the Philippine economy started to gain momentum last year, the lifting of pandemic-led restrictions allowed Aboitiz Power Corporation (AP:PHL) to restart its uptick of production towards power generation, distribution, and energy supply once again.

Being the largest subsidiary of Aboitiz Equity Ventures Inc. (AEV:PHL), Aboitiz Power contributes more than half of its parent company’s total revenue.

Financial results in 2022 showed a 32% increase in Aboitiz Power’s net income compared to 2021, combined with a 7% increase in total capacity sold. This was mainly due to the company’s initiatives of growing its renewable energy portfolio and its integration of technology and digital improvements into its business processes.

Currently, Aboitiz Power is set to complete multiple renewable energy projects within the year such as the Cayanga solar project in Pangasinan, the Laoag solar project, and the Magat BESS project in Isabela.

In order to achieve the company’s long-term goal of having a 4,600-MW net attributable sellable capacity by 2030, capital expenditures starting this year includes prioritizing the development and construction of various solar, geothermal, hydro, and wind projects.

Most recently, the company has also partnered with multiple organizations to help achieve and grow their business initiatives.

Aboitiz Power and Japan’s JERA Co., Inc., have committed to collaborative efforts in assessing the feasibility of ammonia co-fired power generation and further development of the ammonia and hydrogen value chains in the Philippines. Emerging Power, Inc. has also partnered with the company by signing a power supply agreement that will provide solar energy to its retail electricity entities.

On top of that, Aboitiz Power has maintained its spot in the FTSE4Good Index Series for the fifth straight year, which measures a company’s performance in Environmental, Social, and Governance (ESG) practices, due to its commitment towards environmental conservation.

Through the years, the company’s multidimensional focus on company strategy, management, and innovation has helped it adjust to the constantly changing environment.

However, the as-reported metrics of Aboitiz Power imply that the company may not be as adaptable as it appears to be, with as-reported metrics displaying less than half of its Uniform profitability in 2022.

In reality, the company’s real economic profitability has actually been more than what as-reported metrics highlight, reaching 10% in 2022.

As-reported metrics overstate Aboitiz Power’s cost efficiency primarily because of how interest income, among many other accounting distortions, is treated.

Interest income arises from the earnings related to the firm’s investment in stocks, deposits, and associates/affiliates, which are not essential to the company’s core operations. Therefore, interest income should be subtracted from a company’s earnings.

In 2022, Aboitiz Power recognized PHP 15.8 billion of interest income from its bank deposits and investments, making up more than half of its net income.

Removing PHP 15.8 billion from Aboitiz Power’s earnings along with the many other adjustments made leads to just 12% Uniform earnings margin in 2022, lower than as-reported earnings margin of 21%.

Aboitiz Power’s profitability is stronger than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

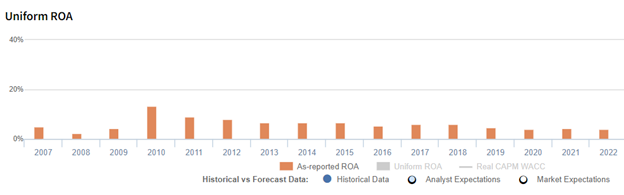

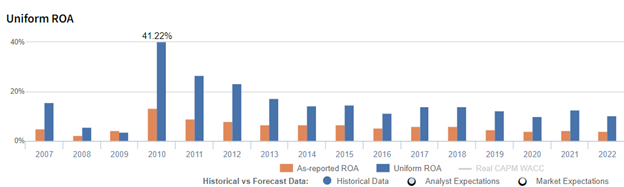

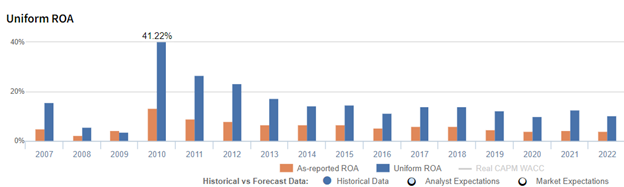

For example, Uniform ROA for Aboitiz Power was 10.2% in 2022, substantially higher than the as-reported ROA of 4.1%, making the company appear to be a much weaker business than real economic metrics highlight for the past six years.

Moreover, since 2019, Uniform ROA has remained higher than 10%, while as-reported ROA has not eclipsed past 5% in the same time frame, substantially distorting the market’s perception of the firm’s ceiling.

Aboitiz Power’s Uniform earnings margins are weaker than you think but its Uniform asset turns make up for it in recent years

Trends in Uniform ROA have been driven primarily by Uniform earnings margin, and to a lesser extent, Uniform asset turns.

Since compressing to 4.5% in 2008, Uniform margins have fluctuated between 8% and 39%. Meanwhile, Uniform turns remained at 0.6x to 0.7x levels from 2017 to 2021, before expanding to 0.9x levels in 2022.

SUMMARY and Aboitiz Power Corporation Tearsheet

As our Uniform Accounting tearsheet for Aboitiz Power Corporation (AP:PHL) highlights, the company trades at a Uniform P/E of 19.7x, above the global corporate average of 18.4x and its historical P/E of 16.6x.

High P/Es require high EPS growth to sustain them. In the case of Aboitiz Power, the company has recently shown a 17% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Aboitiz Power’s sell-side analyst-driven forecast is to see Uniform earnings growth of -20% and 3% in 2023 and 2024, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aboitiz Power’s PHP 36.80 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink immaterially per year over the next three years. What sell-side analysts expect for Aboitiz Power’s earnings growth is well above what the current stock market valuation requires in 2023 and 2024.

Moreover, the company’s earning power is 2x the long-run corporate average. Additionally, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate credit risk and a high dividend risk.

To conclude, Aboitiz Power’s Uniform earnings growth is above its peer averages, but below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com