This company’s diversification strategies helped it thrive for almost 200 years, with an 8% Uniform ROA that is twice the as-reported!

This company has been around for almost two centuries, surviving different eras including the Opium War and World War II. Even with this company’s balanced portfolio of companies and conglomerates from different industries, as-reported accounting displays years of muted profitability.

Uniform Accounting reveals that the company’s diversification strategies are actually generating Uniform ROAs that are double what is reported.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Hong Kong’s history is an eventful one.

The Fragrant Harbour, which is the literal translation of Hong Kong, is one of the special administrative regions (SAR) of China. This has been possible through the “One Country, Two Systems” doctrine, which was negotiated and signed in 1984 but took effect in 1997. This agreement gives Hong Kong its economic autonomy in everything except defense for the next 50 years after it took effect.

However, this autonomy seems to be in jeopardy, after protests arose in June 2019, following plans to allow extradition to mainland China. Other reasons for these protests include democratic reform and the fear of losing Hong Kong’s autonomy.

Prior to all this, Hong Kong was originally an island of China. In the 1800s, London had been trading with China for its tea leaves, but the English capital did not have any product that China was primarily interested in so London had to pay with silver. Because of this, the British incurred deficits from trading.

To eliminate these deficits, the British started smuggling opium in China and sold them at expensive prices. However, due to the increasing number of addicts, the court ordered the elimination of the illegal trade of opium, signaling the start of the Opium War in 1839.

This war lasted for a few years, and the British emerged as the victor of the war.

The company that played a major role in the turning over of the island of Hong Kong to the British is Jardine Matheson. As a major opium dealer during that time, the company’s founders, William Jardine and James Matheson, urged London to force China to hand over the island of Hong Kong to the British and make it their colony. It was made official under the Treaty of Nanking in 1843.

After this, Jardine Matheson moved its headquarters from Canton to Hong Kong and continued its business as a tea exporter, shipping insurance agent, and opium trader. As the company diversified into other businesses like sugar refining, textiles, property development, and tramways, it dropped the opium business in 1872.

Founded in the early 1830s, the company has witnessed Hong Kong’s entire history, survived two world wars, and is still operating today, thanks to its diversification strategy and social and political influence.

Throughout its almost two centuries of existence, the company diversified, expanded, and transformed its offerings to fulfill the needs of the market. Jardine Matheson operates in major sectors such as engineering and construction, food retailing, luxury hotels, transport services, and more.

Today, the company has a cross-holding structure wherein Jardine Matheson holds an 85% interest in Jardine Strategic, while the latter also holds 59% of the former.

One reason to have this structure is to prevent a hostile takeover, as the number of shares that are cross held can hinder the takeover. Jardine Matheson put this structure in place for that reason, given its history of having accrued debts from defending one of its businesses from a takeover.

Jardine Strategic holds substantial ownerships in Jardine Matheson’s major interests such as HongKong Land, Dairy Farm, Mandarin Oriental, Jardine Cycle & Carriage, and Astra International. These companies are industry leaders in their respective sectors in Asia.

Jardine Matheson’s secret to its longevity is its diversification and transformation strategies. Its ability to serve a wide range of customers in different industries and its ability to transform its businesses according to the market’s needs made the company survive for more than 180 years.

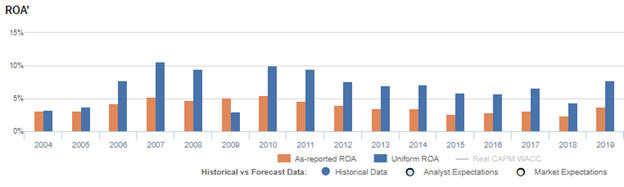

However, as-reported metrics show that the company’s returns have been consistently weak at below cost of capital for the past sixteen years. As-reported return on assets (ROA) currently sits at just 4%.

This is not an accurate representation of Jardine Matheson’s profitability. Uniform Accounting shows that the company has actually stronger returns in fifteen of the past sixteen years. Currently, its Uniform ROA is at 8%.

One key metric that is causing distortions in as-reported ROAs is minority interest expense.

Minority interest expense is the portion of the company’s total earnings that is attributed to its minority shareholders. These minority shareholders are investors or other organizations that own less than 50% of the company.

Jardine Matheson, regularly reports minority interest expenses, which are deducted from the company’s total earnings. This is done to account for the part of the earnings that is allocated to the company’s minority shareholders.

However, removing minority interest expenses from a company’s net income does not show its performance as a whole, making the company’s profitability appear substantially weaker than it actually is. By adding it back to the company’s net income, we can see the company’s true earning power as a whole and not just a part of it.

After adjusting for minority interest expense and applying other adjustments, we can see that Jardine Matheson is not at all a weak business as implied by its below cost-of-capital as-reported ROAs. In fact, its Uniform returns are 2x stronger than what the market thinks.

Jardine Matheson Holdings Limited’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Jardine Matheson’s Uniform ROA has been higher than its as-reported ROA in fifteen of the past sixteen years. For example, Uniform ROA was 8% in 2019, while as-reported ROA was only 4%.

The company’s Uniform ROA for the past sixteen years has ranged from 3% to 11%, while as-reported ROA has ranged only from 2% to 6% in the same time frame.

From 3%-4% levels in 2004-2005, Uniform ROA rose to 11% in 2007 before falling back to 3% in 2009. Uniform ROA then improved back to 10% levels in 2010-2011, before gradually compressing to 4% in 2018 and subsequently jumping to 8% in 2019.

Jardine Matheson Holdings Limited’s Uniform earnings margins are weaker than you think, but its Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

After expanding from 2% in 2004 to 5% in 2007, Uniform margins compressed to 3% in 2009, before rising to a peak of 11% in 2010. It then declined to 7%-8% levels in 2013-2016, before briefly falling to 5% in 2018 and elevating back to 10% in 2019.

Meanwhile, Uniform turns maintained 1.8x-2.2x levels from 2004-2008, excluding a 1.3x underperformance in 2005. It then gradually compressed to 0.7x levels in 2019.

SUMMARY and Jardine Matheson Holdings Limited Tearsheet

As the Uniform Accounting tearsheet for Jardine Matheson Holdings Limited (J36:SGP) highlights, its Uniform P/E trades at 34.2x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Jardine Matheson, the company has recently shown a 274% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Singapore Financial Reporting Standards (SFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Jardine Matheson’s sell-side analyst-driven forecast is a 139% and 64% earnings shrinkage in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Jardine Matheson’s USD 56.99 stock price. These are often referred to as market embedded expectations.

Jardine Matheson can have Uniform earnings shrink by 9% in each of the next three years and still justify current market expectations. What sell-side analysts expect for Jardine Matheson’s earnings is well below what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is around the corporate average. Moreover, cash flows and cash on hand are below its total obligations, and the intrinsic credit risk is 60bps above the risk-free rate. Together, this signals a high dividend and credit risk.

To conclude, Jardine Matheson’s Uniform earnings growth is above its peer averages in 2020, and the company is trading above its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com