This company’s innovative operating system solutions translate to a 22% Uniform ROA, which is more than 5x of as-reported returns!

Many might think that the Android OS is limited to smartphones and tablets. They might be surprised to learn that other objects like watches, glasses, televisions, and cars use this same operating system. Put the term “smart” on the device, and it can probably run on Android OS.

The application possibilities seem endless for this operating system, and this solutions company stands to benefit from these opportunities. This company provides operating system technology and specializes in mobile, IoT, automotive, and enterprise products.

However, as-reported metrics show that the company’s efforts to innovate Android solutions do not seem to translate to profitability. Uniform Accounting shows the opposite, with TRUE economic profitability 5x higher than the as-reported returns!

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Communication is essential to be able to live harmoniously and to understand each other. Being able to speak the same language makes it easier for us to understand and interact with one another.

The same is true with electronic devices. In order for our computers, phones, and other gadgets to understand what we want them to do, they must first understand the language that the user is utilizing.

An operating system bridges the gap between human and machine understanding. Humans can send instructions to a computer, which is then interpreted by its operating system, allowing the computer to carry out said instructions.

Without an operating system, a computer or smart gadget would be useless.

Aside from allowing the users to communicate with computers, the operating system is also in charge of the computer’s memory and processes, as well as its hardware and software.

Today, with the proliferation of smartphones, Android has been at the forefront of operating systems for mobile devices. In fact, there are more than 2.5 billion active Android users, according to Google.

Thunder Software Technology Co., Ltd. is principal in Android core technology and a solution provider for its middleware to upper application development. The company’s product line is rooted in the Android system, providing customizable solutions for smartphones, tablets, and internet TV and cable boxes.

ThunderSoft has heavily invested its research and development not only in Android, but also with the mobile operating system technology of Windows, Linux, and HTML5. As a result, the company has become vital in the global smart device ecosystem.

ThunderSoft has developed a strong vertical integration across different industries, holding strategic partnerships with large IoT (Internet of Things) vendors, software and internet vendors, and mobile carriers, to name a few. Among some of these partnerships include companies we have previously discussed, such as Tencent and Haier.

In the pursuit of elevating technological innovation in the smart industry, the company has also formed joint ventures with Arm, Qualcomm, and Intel.

Through its joint venture with Arm, they created “an incubator for leading startups” called the ARM Innovation Ecosystem Accelerator. This platform has accelerated over 115 tech-driven startups, having provided them with one-stop services, resources, and smart hardware.

Meanwhile, Thundercomm, the venture formed with Qualcomm, has provided developers and manufacturers of AI-enabled devices with an AI Developer kit. This kit is composed of several hardware and software components, as well as AI apps and models, to help accelerate on-device AI for its customers.

Today, ThunderSoft continues to enhance its operating system technology and invest in IoT and smart devices. It has released its Edge Station with Intel and has ongoing developments for their Intelligent Connected Vehicle software with GAC R&D Center.

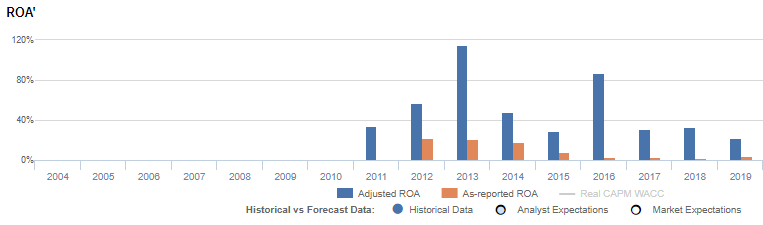

Despite the company’s strong innovative offerings for Android systems, its profits are still below cost of capital levels based on as-reported figures. As-reported return on assets (ROA) in 2019 was only at 4%, making it look weaker than what it actually is.

ThunderSoft’s real economic profitability is better reflected with Uniform Accounting adjustments. Looking at the company’s performance in 2019, ThunderSoft’s Uniform ROA was at 22%, which is more than 5x its as-reported ROA of 4%.

One key metric that is causing distortions in as-reported ROAs is R&D expenses.

ThunderSoft has regular material investments in research and development that it records as an outright expense, in accordance with the accounting standards. However, expensing R&D fails to recognize the matching principle of recognizing expenses in the period when the related revenue is incurred.

R&D investment is actually an investment in the long-term cash flow generation of the company. If this remains treated as an expense, the company’s profitability may appear substantially weaker than it actually is.

After R&D and other significant adjustments are made, the company’s TRUE earning power becomes obvious, and we see a far more profitable company.

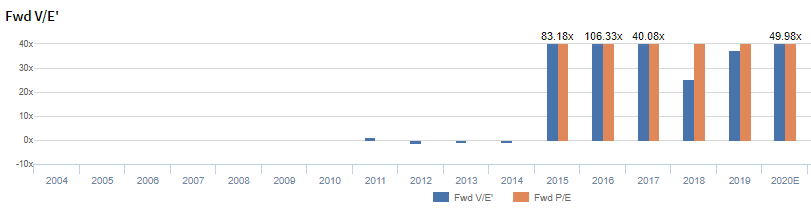

ThunderSoft’s valuations are cheaper than as-reported

Thunder Software Technology Co., Ltd. (300496:CHN) currently trades above corporate averages at a 50.0x Uniform P/E (blue bars), below its as-reported P/E of 78.8x (orange bars).

Even at these levels, the market is pricing in expectations for Uniform ROA to fall slightly to 21% in 2024, accompanied by 31% Uniform asset growth going forward.

Analysts have similar expectations, projecting Uniform ROA to remain at 22% levels in 2021, accompanied by a 38% Uniform asset growth.

ThunderSoft’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

ThunderSoft’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA is 4% in 2019, significantly lower than its Uniform ROA of 22%. When Uniform ROA peaked at 115% in 2013, as-reported ROA was just at 21%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher. ThunderSoft’s Uniform ROA for the past nine years has ranged from 22% to 115%, while as-reported ROA ranged only from 2% to 21% in the same timeframe.

From 34% in 2011, Uniform ROA expanded to a peak of 115% in 2013, before falling to 29% in 2015. Afterwards, Uniform ROA recovered to 87% in 2016, before compressing to 22% in 2019.

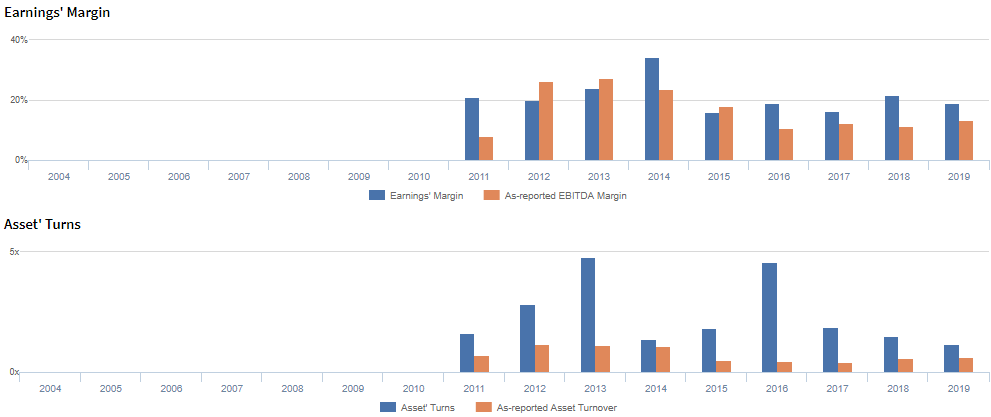

ThunderSoft’s margins and turns are stronger than you think

Volatility in Uniform ROA has been driven primarily by trends in Uniform asset turns and to a lesser extent, by Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins increased from 21% in 2011 to 35% in 2014, before falling to 16% in 2015. It then recovered to 22% in 2018, before fading to 19% in 2019.

Meanwhile, Uniform asset turns rose from 1.6x in 2011 to a peak of 4.8x in 2013, before contracting to 1.4x in 2014. It then rebounded to 4.6x in 2016, before declining to 1.2x in 2019.

SUMMARY and Thunder Software Technology Co., Ltd. Tearsheet

As the Uniform Accounting tearsheet for Thunder Software Technology Co., Ltd. (300496:CHN) highlights, the Uniform P/E trades at 50.0x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of ThunderSoft, the company has recently shown an 11% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, ThunderSoft’s sell-side analyst-driven forecast is a 42% and 28% earnings growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ThunderSoft’s CNY 64.51 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, ThunderSoft would need to have Uniform earnings grow by 33% each year over the next three years. What sell-side analysts expect for ThunderSoft’s earnings growth is above what the current stock market valuation requires in 2020, but below that requirement in 2021.

The company’s earning power is 4x the corporate average. Also, cash flows are 4x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, ThunderSoft’s Uniform earnings growth is above its peer averages in 2019. However, the company is trading above average peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com