This company’s omnichannel strategy helped it survive the retail apocalypse, and it is still expanding! Uniform ROA is 26%, not 3%

The retail apocalypse signaled the end of an era for a lot of retailers. This company’s retail business, however, is still opening stores worldwide and its business model helped it thrive amid store closures everywhere.

As-reported metrics seem to ignore the success of the business, reporting below cost-of-capital returns. Uniform Accounting tells us otherwise, indicating that this company has a stronger Uniform return on assets (ROA) than what the market thinks.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Even after the Great Recession in 2008, retailers continue to suffer.

Many of the biggest department stores and other brick-and-mortar retailers have gone bankrupt and have closed their stores since the early 2010s. Analysts called this phenomenon the “retail apocalypse.”

Some of the factors that led to the retail apocalypse are the growth of online shopping, rising rental costs, and the over-expansion of malls. Consumer spending has also shifted from material purchases to food and travel, leading to a decline in revenues from retailers’ target market.

Large chain retailers were among the hardest hit, particularly because their large store formats meant higher operating expenses. American retailers such as Sears, Macy’s, Radioshack, Toys R Us, and J.C. Penney have either declared bankruptcy or closed many of their stores—and will probably continue to close more in the future.

It isn’t just the U.S. stores suffering from this shift in consumer behavior. The retail apocalypse is happening worldwide, and stores in Asia are not at all exempted. For example, Forever 21 has largely reduced its presence in Asia after filing a Chapter 11 bankruptcy in the U.S., and Zara also has plans to close a lot of its stores in the continent.

However, certain companies have managed to adapt to the retail apocalypse. One of them is CK Hutchison’s largest revenue-generating segment, A.S. Watson Group.

A.S. Watson Group is the world’s largest international health and beauty group, and Hong Kong’s oldest retailer. What started out as a single dispensary in Hong Kong is now a company with over 15,800 stores worldwide.

The rapid global expansion of the company started when Hutchison Whampoa bought the A.S. Watson Group in 1963 and opened Watsons’ pharmacies all over the world. One of these extensive expansions was the joint venture with SM Prime Holdings in the Philippines.

Along with these global expansions, the company has also acclimated itself to changes in the trends of the retail industry, making it immune to the retail apocalypse.

With its business mainly engaged in health and beauty products, Watsons needed to cater to the specific needs of different markets in order to grow. To do that, the company included an assortment of localized products along with its general international product mix.

Moreover, with the advancement of technology, the company started to invest in its digital initiatives as early as 2012, and has integrated an online-to-offline (O2O) business model.

This business model connects its stores to its e-commerce site. While most online retailers only offer a “click and deliver” process for ordering their products, Watsons’ O2O business model allows for consumers to opt for a “click and collect” option.

This gives customers the option to pick up their goods at any store branch any time after ordering. This setup is more beneficial for Watsons because its customers are more likely to purchase more goods in the store when they collect their order.

This business model shows how Watsons was able to embrace advancements in technology to address the anticipated surge of e-commerce. By adopting this model, the company made itself future-proof, withstanding the retail apocalypse.

The company did not only show resilience, but it also aimed for growth. While most retailers are closing their stores, Watsons is opening more.

In 2019, the company has been opening new stores at an average of one store every seven hours across its global markets for the fourth year in a row. However, its plan to open 1,300 more shops this year has been lessened to just 900 due to the pandemic. Nevertheless, this still signals growth for the firm.

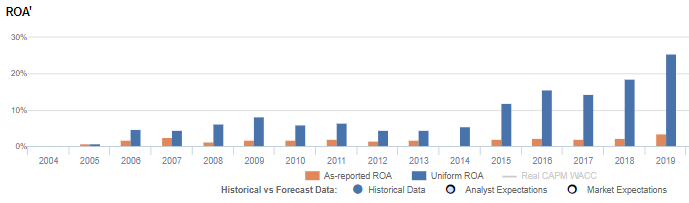

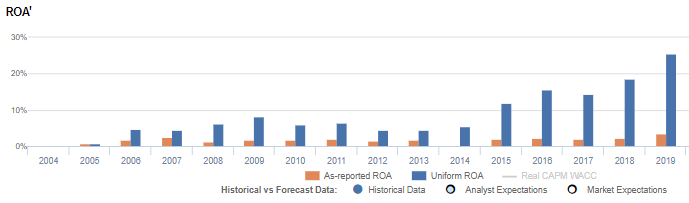

The huge success of A.S. Watson in merging online and offline business and its continuous opening of profitable stores worldwide would have made an impact on its parent company’s financial results. However, as-reported metrics do not reflect that, given that CK Hutchison’s returns are consistently below cost of capital for the past sixteen years, and is just sitting at 3% currently.

This is a clear misrepresentation of CK Hutchison’s profitability, when in fact, its business model and growth strategies have caused its Uniform ROAs to rise from below cost-of-capital levels to its 26% levels currently.

This shows that Watsons’ strategies to adapt to the retail apocalypse through its O2O business model and its aggressive store openings are working. Being CK Hutchison’s largest segment, the success of Watsons greatly impacted the company’s profitability.

One of the things that as-reported metrics failed to consider is the company’s goodwill and other intangible assets, which caused the distortions between Uniform and as-reported ROAs.

Goodwill and other intangibles are purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not showing the real strength of CK Hutchison’s earning power. After goodwill, other intangible assets, and other significant adjustments are made, we can prove that the company does not really have weak, below cost-of-capital returns. In fact, it has been performing well beyond what the market thinks, with Uniform ROA that is approximately 8x stronger than as-reported.

CK Hutchison’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

CK Hutchison’s as-reported ROA has been lower than its Uniform ROA in the past fifteen years. For example, as-reported ROA is 3% in 2019, significantly lower than its Uniform ROA of 26%. When Uniform ROA was at 19% in 2018, as-reported ROA was only a meager 2%.

The company’s Uniform ROA for the past fifteen years has ranged from 1% to 26%, while as-reported ROA arranged only from 1% to 3% in the same time frame.

From 1% in 2005, Uniform ROA gradually increased to 16% in 2016 and further soared to its peak of 26% in 2019.

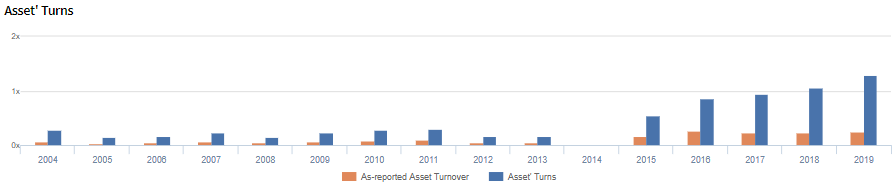

CK Hutchison’s Uniform asset turns is stronger than you think

Strength in Uniform ROA has been driven by the strength in Uniform asset turns. Uniform asset turns have been higher than as-reported asset turnover in each of the past sixteen years.

As-reported asset turnover declined from 0.1x in 2004 to immaterial levels in 2014, before reaching its peak of 0.3x in 2016 and compressing back to 0.2x in 2019.

Meanwhile, Uniform asset turns trended at a range of 0.1x to 0.3x from 2004 to 2013 before falling to immaterial levels in 2014. Since then, Uniform asset turns soared, reaching its peak of 1.3x in 2019.

SUMMARY and CK Hutchison Holdings Limited Tearsheet

As the Uniform Accounting tearsheet for CK Hutchison Holdings Limited (1:HKG) highlights, its Uniform P/E trades at 7.4x, which is below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of CK Hutchison, the company has recently shown a 23% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Accounting Standards (HKAS) earnings and convert them to Uniform earnings forecasts. When we do this, CK Hutchison’s sell-side analyst-driven forecast is a 39% earnings shrinkage in 2020, followed by a 25% earnings growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CK Hutchison’s HKD 46.70 stock price. These are often referred to as market embedded expectations.

CK Hutchison can have Uniform earnings shrink to 24% each year over the next three years and still justify current market expectations. What sell-side analysts expect for CK Hutchison’s earnings is below what the current stock market valuation requires in 2020, but well above that requirement in 2021.

The company’s earning power is 4x than the corporate average. Additionally, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, CK Hutchison’s Uniform earnings growth is below its peer averages in 2020. However, the company is trading in line with its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com