This company’s stock has skyrocketed but as-reported ROAs were flat, Uniform Accounting wipes away the grime to reveal a clearer picture

Disinfecting is more crucial than ever as people continue to experience one of the worst global pandemics of this century.

A major player in this space, this company continues to benefit from the surge of consumer demand for disinfectants and other cleaning products.

They have been able to sustain this demand through a steady stream of advertising and acquisition investments that enabled them to strengthen their brand identity while they expanded their product portfolio.

However, while as-reported metrics imply that these investments have only translated into muted returns over the last decade, Uniform Accounting shows that profitability has actually grown.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

“An ounce of prevention is worth a pound of cure. It’s more prudent to head off a disaster beforehand than to deal with it after it occurs.” – Henry de Bracton, De Legibus

With almost 3 million COVID-19 cases worldwide, it’s safe to say that people are adopting best practices to make sure the virus does not spread further.

A few of these practices include social distancing, which prevents the spread by cutting off human-to-human contact, wearing masks to protect from the virus, and disinfecting both yourself and any products brought in from outside.

Following only the first two methods does not guarantee a 0% virus transmission probability. In fact, there have been reported cases where people still tested positive despite following quarantine procedures. This is because the virus can survive on object surfaces for an extended period of time, which is why disinfecting is as crucial as social distancing and wearing protective gear.

Clorox, a major player in that space, is benefiting from this pandemic as the outpour of demand provides them the boost they needed to get out of the competition-centered rut they were in. Specifically, with many of their competitors selling lower-priced alternatives, this created a challenging headwind for the company.

However, when it comes to household products like disinfectants, consumers tend to buy products that they trust. They are less likely to be stringent about price differences, especially during a time of fear and uncertainty.

Building that trust took years and millions of advertising and marketing dollars—on average, half a billion dollars annually.

Their advertising strategy focused on value—making sure their products are worth the price.

To do that, they strengthened their brand identity by expanding their visibility. They aimed for popularity because brand recognition increases the trust and value consumers associate with the product. This means that the more the consumers see a brand, the likelier it is for their products’ perceived credibility to increase.

Once product visibility ramped up, so did their market shares. Currently, 80% of the company’s sales are from products that hold the top spots in their respective categories. Because of their strong presence, they were able to increase prices while keeping production and distribution costs lower, subsequently increasing margins.

To complement this strategy, Clorox also made several acquisitions to expand their offerings by using new sales channels. These acquisitions included Aplicare and Healthlink, to bolster growth in the healthcare industry by targeting the facilities cleaning front.

The company also made acquisitions to venture into areas where they could leverage their capabilities to create new sources of revenue. Specifically, they expanded into the food industry (Hidden Valley) and the personal care market (Burt’s Bees), and more recently, the health and wellness market (Nutranext).

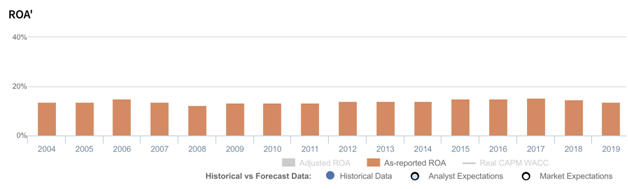

Their successful advertising and acquisition strategy has sent the stock steadily reaching new highs over the last decade. But as-reported metrics (ROA) would argue that this is unwarranted, with ROAs remaining stable at only 13%-15% levels since 2011.

In reality, Clorox’s Uniform ROAs have gone up from 14% to 23% over the same period. As-reported metrics directionally distorted the company’s performance, making it seem that the stock’s almost 200%+ price increase in the last decade was unjustified.

Furthermore, as-reported metrics failed to consider the amount of goodwill on the Clorox’s balance sheet, seeing that the company has made a substantial number of acquisitions in the past.

This intangible asset is purely accounting-based and unrepresentative of the company’s actual operating performance, distorting the company’s profitability by artificially inflating the asset base. As a result, ROAs seem smaller by about 1x-2x on average.

While these adjustments show a stronger earning power, in order to sustain its strength, Clorox is leveling up their advertising by riding on the influencer marketing trend. This targets younger audiences and increases their digital media footprint at the same time, creating a new channel for e-commerce growth.

The company also keeps a disciplined approach when it comes to the process of making international acquisitions. Identifying demand-building investments on the global front will place the company in a stronger position to scale their operations while they build their brand portfolio further.

Successful execution of these strategies will most likely drive long-term growth, commanding higher margins and subsequently, higher profitability.

Clorox’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

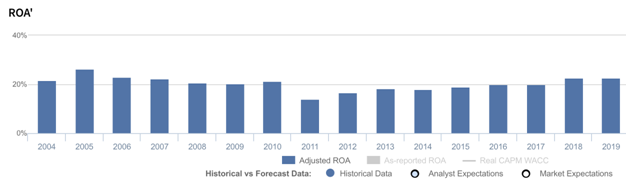

Uniform ROA has been higher than as-reported ROA in the past sixteen years. For example, as-reported ROA for Clorox was 14% in 2019, which is significantly lower than its Uniform ROA of 23%.

Clorox’s Uniform ROA has ranged from 14% to 26% over the past sixteen years. From a historical high of 26% in 2005, Uniform ROA fell to 14% in 2011. It then recovered to 18% to 20% levels in 2013 to 2017, and jumped to 23% in 2018, remaining there since.

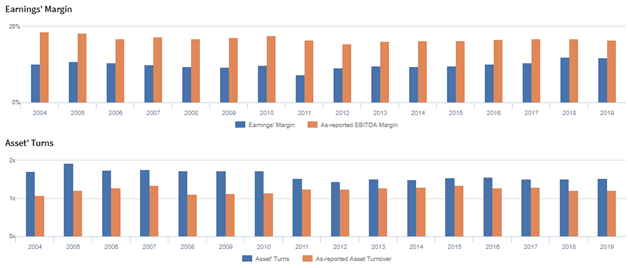

Clorox’s Uniform ROA is driven by significantly more robust Uniform asset turns but is slightly offset by Uniform earnings margins

Trends in Clorox’s Uniform ROA have largely been driven by trends in Uniform earnings margin and Uniform asset turns.

From 2005-2011, Uniform earnings margins declined from 14% to 9%. It recovered to 12% levels in 2015, and further increased to 15% in 2019. Meanwhile, Uniform asset turns fell from 1.9x in 2005 to 1.4x in 2012. It then improved to 1.6x in 2016, before stabilizing at 1.5x levels through 2019.

At current valuations, markets are pricing in expectations for Uniform earnings margin and Uniform asset turns to reach new peaks.

SUMMARY and Clorox Tearsheet

As the Uniform Accounting tearsheet for The Clorox Company (CLX) highlights, the Uniform P/E trades at 29.7x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Clorox, the company has recently shown immaterial Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Clorox’s Wall Street analyst-driven forecast is a 6% growth in 2020, and an immaterial growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Clorox’s $191 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 7% each year over the next three years. What Wall Street analysts expect for Clorox’s earnings growth is below what the current stock market valuation requires.

The company’s earning power is 4x the corporate average. However, cash flows are below their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate risk for their dividend.

To conclude, Clorox’s Uniform earnings growth is in line with peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com