This company’s unprecedented 2.5 billion reach is powering the REAL returns that are 2-3x the as-reported numbers

Through a series of innovative developments, this company became one of the biggest duopolies in advertising, making its way to the top by focusing on connections as their main product.

As more of the disconnections between people are bridged, the more the company grows—both in users and in earnings.

Though as-reported metrics understate the true strength of their product, TRUE UAFRS-based (Uniform) analysis shows that this company deserves its industry leadership.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The largest social media platform in the world was originally just a website for Harvard students to judge other students and vote on who’s “hot” and who’s “not.”

This was shut down, of course, by the higher-ups over at the university.

A new website, TheFacebook, emerged a few months later, but this time as a way to connect students within the university.

The platform became so popular that the creators decided to expand their network to universities across the US and, eventually, to anyone older than 13.

By the end of 2008, just five years after the launch, the total number of users ballooned to 150 million.

Facebook had finally gone mainstream.

Features like Facebook Chat, the Wall, and People You May Know were launched in that same year.

Back then, if people wanted to insta-chat, they’d do it with Yahoo! Messenger or AOL. If they wanted to connect with other people through about-me-type profiles, they’d sign on to Myspace or Friendster.

But Facebook was all of this rolled into one. Users flocked to the site because it was easier to maintain just one social profile.

Eventually, the then-greats of social media died out as Facebook continued to garner sign-ups by the millions.

With the rapid evolution of smartphones, the company took the opportunity to ride this new wave of technology with their mobile app.

The app increased the company’s reach and user accessibility. Now everyone can log onto Facebook from wherever, whenever.

Currently, with over 2.5 billion monthly active users, there’s no doubt that Facebook has shaped social media culture as we know it.

It makes it easier to communicate with people thousands of miles away and be updated with the latest global happenings in real time, so it’s not difficult to see why people are attached.

The Philippines is especially attached, with its standing title of “social networking capital of the world.” You wouldn’t expect anything less considering that in the country, Facebook is free!

Out of the 109 million people in the country, around 76 million are social media users. That’s 70% of the total population.

Filipinos are the world’s top users of Facebook, spending an average of four hours daily on the app. Globally, users spend about two and a half hours, making it the top social media platform in the world.

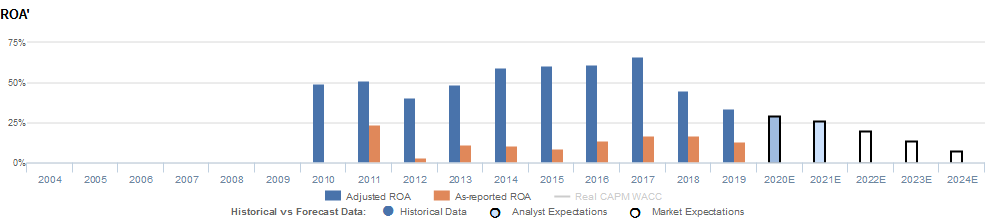

Uniform Accounting indicates that as-reported metrics are understating Facebook’s profitability and shows how its global reach and position as an industry leader has enabled it to have robust returns, with Uniform return on assets (ROA) north of 30% in each year since 2010.

However, even as the company sustains its leadership, markets are still pessimistic about its outlook given rapid declines in profitability from a Uniform ROA of 66% in 2017 to just 34% in 2019.

Historically, the company has done an amazing job of identifying accretive acquisitions. Instagram, WhatsApp, and Oculus are among the companies that Facebook has transformed into high-growth, profitable businesses.

Furthermore, the company has gotten better at leveraging data to improve audience targeting, enabling them to take a larger share of advertising revenue across their platforms.

These growth drivers, coupled with management’s confidence in their ability to drive platform engagement, continued daily active user strength, and mobile ad revenues indicate that the market may be TOO pessimistic and that equity upside is likely.

Facebook’s earning power is still actually more robust than you think

As-reported metrics significantly understate Facebook, Inc.’s (FB:USA) profitability.

For example, as-reported ROA for Facebook was 13% in 2019, which is materially lower than Uniform ROA of 34%, making Facebook appear to be a much weaker business than real economic metrics highlight.

Moreover, as-reported ROA has slightly decreased from 17% in 2017 to current 13% levels, while Uniform ROA also decreased from 66% to 34% over the same period, significantly distorting the market’s perception of the firm’s historical profitability trends.

Historically, Facebook has seen somewhat volatile but robust profitability.

After falling from 49%-51% levels in 2010-2011 to 41% post-IPO in 2012, Uniform ROA expanded to 60%-62% levels in 2014-2016.

Since then, Uniform ROA rose to a peak of 66% in 2017, before collapsing to 34% in 2019.

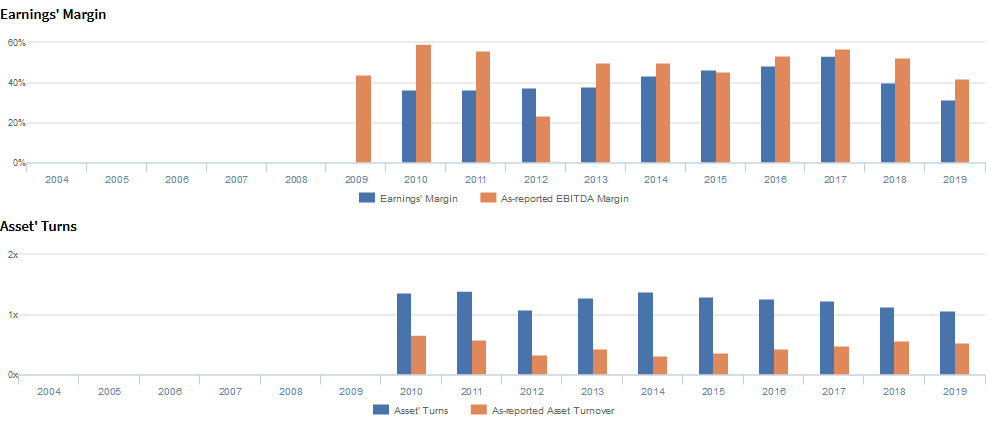

Facebook’s Uniform ROA is driven by significantly more robust Uniform asset turns but is offset by Uniform earnings margins

Trends in Uniform ROA have largely been driven by trends in Uniform earnings margin and stability in Uniform asset turns.

From 2010-2017, Uniform earnings margins improved markedly from 36% to 54%, before decreasing to 32% in 2019.

Meanwhile, after falling from 1.4x in 2011 to 1.1x in 2012, Uniform asset turns improved to 1.4x in 2014, before fading to 1.1x in 2019.

At current valuations, markets are pricing in expectations for both Uniform Margins and Uniform Turns to fall to historically low levels, which appears far too pessimistic.

SUMMARY and Facebook Tearsheet

As the Uniform Accounting tearsheet for Facebook highlights, the Uniform P/E trades at 19.2x, which is below corporate average valuation levels but around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Facebook, the company has recently shown a 1% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Facebook’s Wall Street analyst-driven forecast is 13% into 2020, and 11% into 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Facebook’s $185 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 2% each year over the next three years. What Wall Street analysts expect for Facebook’s earnings growth is far above what the current stock market valuation requires.

The company’s earning power is 6x the corporate averages. Also, cash flows are 5x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, Facebook’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading below average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com