This conglomerate’s strong business portfolio enabled it to achieve Uniform ROAs that are higher than its as-reported

Starting out as a seller for secondhand vehicles, this company was able to grow its business by earning a strong track record of profitable businesses through its diversification strategy.

However, looking at as-reported metrics, it seems that its strategy hasn’t helped the company generate any returns. In reality, Uniform Accounting shows that the company’s strategy and diverse portfolio has actually achieved Uniform ROAs that are almost double than its as-reported.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

World War II was considered the deadliest and biggest war in global history, encompassing around 30 countries including the Philippines. Key trade centers like Manila and Cebu were left in ruins.

Before the war, Cebu had been the second most important industrial center in the country. The aftermath of the war left a city full of abandoned or destroyed cruisers and aircrafts. Some of the machines that survived the war weren’t even worth so much anymore that they were either destroyed or left to rot in their current locations.

With almost nothing left but their resourcefulness, many found recycling metal scraps to be a significant source of income. Those scraps became essential materials to restart the manufacturing industry.

One such person who took advantage of the wreckage was A.L. Gotianun, who turned to salvaging ships and eventually selling secondhand vehicles to support his family.

A few years after the war, Gotianun moved to Manila where he met his wife Mercedes. In 1955, both of them founded Filinvest Development Corporation (FDC:PHL) to continue the business of selling and financing secondhand vehicles.

With enough capital from the success of their secondhand vehicles business, Gotianun was able to enter the real estate business through the incorporation of Filinvest Realty Corporation, a business that was engaged in the development of residential subdivisions.

However, due to a recession, the Gotianun family divested its interests in its financial businesses in 1984. As a result, Filinvest Development consolidated its real estate interests and mainly focused on property developments.

When the economy began to recover, Filinvest Development decided to spin off most of its real estate assets and liabilities to Filinvest Land Inc. (FLI) in exchange for the latter’s shares in 1993.

In the following year, Filinvest Development branched out by incorporating East West Banking Corporation (EWBC). This marked the group’s re-entry into the financial and banking services industry.

Its real estate subsidiary, FLI, became widely known in the 1990s and the 2000s due to its strategic goal of serving the middle class market to high-end users. The Philippines’ middle class had grown from 29% of the population in 1991 to 39% in 2006. Today, 40% of the Philippine population is from the middle class market.

The middle-income residential sector is considered the largest housing segment in the country at 47% of the market share. By focusing on that market, Filinvest Development enjoyed a revenue CAGR of 9.5% from 1993 to 2007.

With a successful real estate business, Filinvest Development then turned its attention to its other segments. By executing its targeted diversification strategy, it aims to capture the growth momentum of other industries.

In 2007, Filinvest Development acquired 100% of Pacific Sugar Holdings Corporation for the commodities sector.

To establish its presence in the hospitality sector, the conglomerate formed Chroma Hospitality Inc. and Filinvest Hospitality Corporation in 2008 and 2012, respectively.

In 2009, FDC Utilities Inc. was formed to cater to the energy sector.

For the infrastructure sector, Filinvest Development won an “original proponent status” for the Ninoy Aquino International Airport as part of the NAIA consortium in 2018. In 2019, Filinvest Development made significant moves like signing an O&M concession agreement for Clark International Airport.

This diversification strategy provided a strong track record for Filinvest Development, helping it grow a diverse portfolio of profitable businesses. Its consolidated revenue improved greatly from PHP 12.6 billion in 2009 to PHP 74.8 billion in 2019.

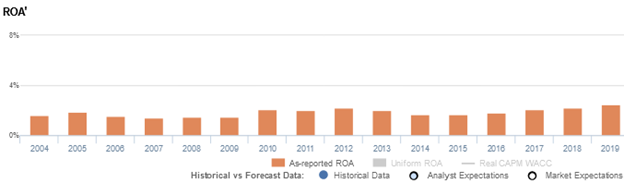

Filinvest Development’s extensive portfolio would make it seem like the company has been successful in executing its diversification initiatives. However, looking at as-reported metrics, it appears that this strategy has not helped Filinvest Development produce any economic profit, with return on assets (ROAs) only reaching a high of 3% in 2019.

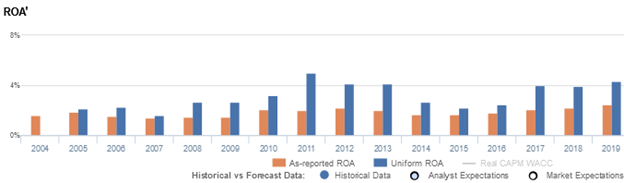

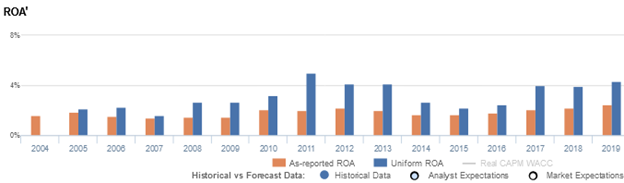

In reality, Uniform Accounting shows that Filinvest Development’s initiative to diversify its business has generated better returns, with Uniform ROAs reaching above cost of capital levels at 5%. This difference in returns numbers spells the difference between a company that is generating economic loss and a company that is actually generating economic profits though small.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example, in 2019, Filinvest Development recognized an interest expense of PHP 4.4 billion, a third of its as-reported net income of PHP 11.9 billion. When we add the PHP 4.4 billion back to earnings, because it is not an operating expense, net income increases.

Cross-comparison against peers also becomes possible since the performance, expectations, and valuations of companies are now evaluated irrespective of the amount of leverage.

Filinvest Development’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight, especially with recent years showing below cost-of-capital returns.

Filinvest Development’s Uniform ROA has actually been higher than its as-reported ROA in the past fifteen years. For example, as-reported ROA was 3% in 2019, but its Uniform ROA was actually higher than that at 4%. When Uniform ROA peaked at 5% in 2011, as-reported ROA was only at 2%.

Specifically, Filinvest Development’s Uniform ROA has ranged from 2% to 5% in the past fifteen years, while as-reported ROA has ranged only from 2% to 3% in the same timeframe. Uniform ROA expanded from 2% levels in 2005-2007 to a peak of 5% in 2011, before compressing back to 2% levels in 2015 and subsequently recovering to 4% in 2019.

Filinvest Development’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin. Since 2004, Uniform margins have been significantly lower than as-reported EBITDA margins each year.

As-reported EBITDA margins declined from a peak of 35% in 2005 to 26% levels in 2007-2008, before expanding to 31% levels in 2010-2011 and falling to 26% in 2014. Since then, as-reported EBITDA margins have recovered to 32%-34% levels in 2017-2019

Meanwhile, Uniform margins compressed from 26% in 2004 to a low of 9% in 2007, before improving to a peak of 27% in 2011 and compressing to 12% levels in 2015-2016. Thereafter, Uniform margins expanded to 21% levels in 2017-2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Filinvest Development Corporation Tearsheet

As the Uniform Accounting tearsheet for Filinvest Development Corporation (FDC:PHL) highlights, it trades at a Uniform P/E of 21.6x, below the global corporate average of 25.2x, but around its historical average of 21.8x.

Low P/Es require low EPS growth to sustain them. In the case of Filinvest Development, the company has recently shown a 17% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Filinvest Development’s sell-side analyst-driven forecast calls for a 6% growth in 2020, followed by an immaterial Uniform EPS decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Filinvest Development’s PHP 8.90 stock price. These are often referred to as market embedded expectations.

Filinvest Development is currently being valued as if Uniform earnings were to grow 2% annually over the next three years. What sell-side analysts expect for Filinvest Development’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

The company’s earning power is below the long-run corporate average. However, cash flows are almost 2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 400bps above the risk free rate. Together, this signals a low dividend risk but a moderate credit risk.

To conclude, Filinvest Development’s Uniform earnings growth is the highest among peers in 2020, and trades above its average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com