This educational institution became a star pupil with its growth initiatives, reaching a Uniform ROA of 12%, not 2%

The Philippines has been dealing with learning poverty for decades. This was most evident during the pandemic.

As a way to mitigate these losses, some schools have already started opening, and one educational institution has capitalized on this—achieving better results than its as-reported data.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

“Learning Poverty” has been an ongoing issue that has been hurting the global economy for years. Its detrimental effects have accelerated during the pandemic.

According to a recent article published by the World Bank, this issue has been worsening in the past years, especially in low- and middle-income countries. It is currently estimated that 70% of 10-year-old kids these days do not know how to understand basic written text.

The Philippines is among the countries with the highest rates of “learning poverty” in East Asia and Pacific—estimating about 91% of children not being able to read and write.

To address this issue, 76% of schools have already implemented face-to-face classes—with 29,721 schools utilizing blended learning while 24,175 schools adopting five-day in-person learning.

One of the educational institutions to open its campus in 2022 is Far Eastern University (FEU:PHL).

Starting off with a limited setup, FEU welcomed its first batch of students mid-February. Initiating steps towards normalcy for its operations and business environment.

Its decision was received with a boost in student population in comparison to its pre-pandemic numbers, which served as a beneficial cause factor to its 16% growth in educational profits.

Looking at the improvement in operation restrictions, FEU also saw an opportunity to become involved in a number of acquisitions, joint ventures, or investments—continuing on its expansion activities that were hindered by the pandemic.

Specifically, in 2022, FEU had a notable partnership with Jerudong Park Medical Centre in Brunei to put in place the first private health science college being the earliest on the list.

A few months later, this partnership was followed by its acquisition and investment in Good Samaritan Colleges, where FEU has 77,273 shares, further developing its academic portfolio.

These initiatives show FEU has been investing a portion of its efforts into enhancing its market share, room for growth, and brand image.

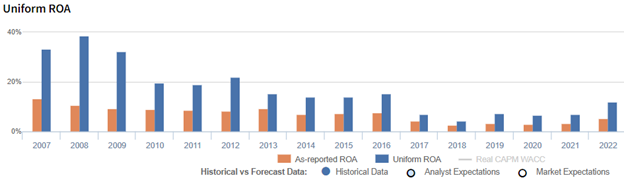

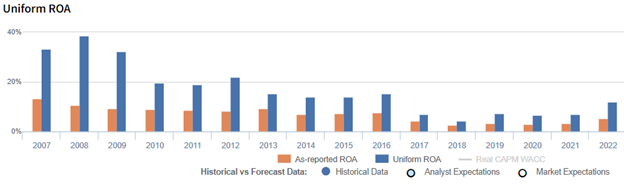

Looking at its as-reported metrics, it looks like FEU hasn’t been generating robust returns, with ROAs barely hitting cost of capital levels of 6%.

In reality, FEU has managed to maintain its profitability levels despite the crisis, reaching a Uniform ROA of 12%.

One of the main contributors to such discrepancy is its treatment of excess cash. While as-reported financials treat FEU’s entire cash balance as part of its asset base, Uniform Accounting removes the cash that’s not necessary to operate and fulfill obligations—cash above what one might view as “operating” cash.

The purpose of removing excess cash is to see what the true operating assets of the firm are. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In 2022 particularly, FEU has PHP 3.8 billion worth of excess cash, making up 24% of the company’s as-reported assets.

Removing excess cash and applying the other adjustments Valens makes, FEU’s 6% as-reported ROA and PHP 16.2 billion asset base are adjusted to reveal its TRUE Uniform ROA of 12%, by essentially utilizing just PHP 10.6 billion of Uniform assets.

FEU’s profitability is stronger than you think in recent years

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that FEU’s profitability has been weaker than what real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROA has been understated. For example, as-reported ROA was 6% in 2022, but its Uniform ROA was way higher at 12%.

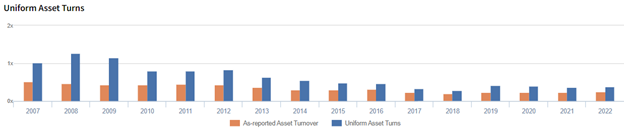

FEU’s historical asset turns are stronger than you think

For the past sixteen years, as-reported metrics have understated FEU’s asset turns, a key driver of profitability.

Moreover, since 2007, as-reported turns only ranged from 0.2x-0.5x through 2022 while Uniform asset turns were able to reach a high of 1.3x.

SUMMARY and The Far Eastern University, Incorporated Tearsheet

As our Uniform Accounting tearsheet for The Far Eastern University, Incorporated (FEU:PHL) highlights, the company trades at a Uniform P/E of 9.8x, which is below the global corporate average of 18.4x and its historical P/E of 13.4x.

Low P/Es require low EPS growth to sustain them. In the case of FEU, the company has recently shown a 97% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, FEU’s sell-side analyst-driven forecast is to see a 4% and immaterial Uniform earnings decline in 2023 and 2024, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify FEU’s PHP 530.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 12% over the next three years. What sell-side analysts expect for FEU’s earnings growth is above what the current stock market valuation requires through 2023.

However, the company’s earning power is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk.

To conclude, FEU’s Uniform earnings growth is below its peer averages and it also currently trades below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com