This electricity provider’s drive to capitalize on its opportunities gives it sky-high potential moving forward, reaching a Uniform ROA of 14%, not 2%

This power corporation managed to perform relatively well despite the systemic risks brought by the COVID-19 pandemic and Typhoon Odette in 2021. It managed to do this by focusing on providing affordable and sustainable power supply, properly maintaining its existing power plants, and entering into new ventures in renewable energy resources.

However, as-reported metrics failed to present a clearer picture of the company’s underlying earnings potential. In fact, Uniform Accounting demonstrated that the company has a better return on assets (ROA) than it appears.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In this day and age, electricity is a basic necessity. Nearly everything we do is run by some form of electric power, whether as a final product or as an input to produce goods and services we use.

One of many electricity providers in the Philippines is the SPC Power Corporation (SPC:PHL).

The company engages with the National Power Corporation (NPC) in the rehabilitation, operation, maintenance and management of the Naga Power Plant Complex (NPPC) in Colon, Naga, and Cebu, which include electricity generation and distribution.

Recently, the company has also started to engage in the exploration and development of renewable energy resources.

In the middle of 2021, SPC decided to expand its operations by setting aside a budget for new hydropower plant projects in parts of Luzon and Visayas.

This ambitious goal to add renewable energy sources and projects to its portfolio put SPC off to a stable start in 2021, averaging a quarterly income of PHP 458.7 million in the first three quarters.

However, Typhoon Odette struck parts of the Visayas region that same year, causing damages to the company’s power facilities, including the distribution system connecting SPC’s power plants to the retail electricity consumer. This turned in a net loss of PHP 178.7 million in Q4 2021.

Despite this, SPC still saw a material increase in its year-on-year revenue from PHP 2.0 billion in 2020 to PHP 2.5 billion in 2021.

Going forward, the company remains focused on seeking growth opportunities in new markets and customer demographics, specifically in its renewable energy segment. As it expands into those areas, it will still maintain a strong grasp in the gas-based industry.

The power company wasted no time in acquiring two of ACEN Corp.’s diesel-fired power barges. It is also set to acquire 470 megawatts (MW) of thermal capacity and around 300 MW of renewable projects.

SPC looks to take advantage of the resurgence in demand after the COVID-19 pandemic and typhoons that ravaged the Visayas region with its prospective projects and continual growth of its existing plants.

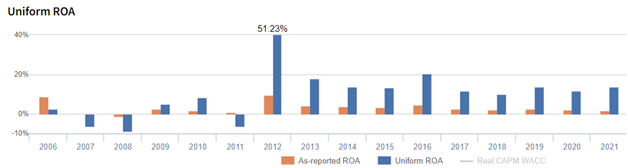

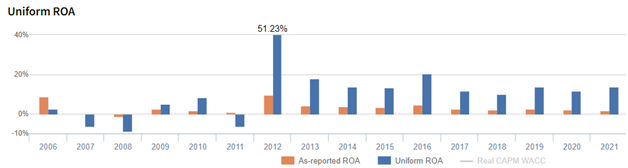

Looking at its as-reported metrics, SPC has managed to maintain its profitability levels despite seeing a slowdown in recent years due to continued pressures on its margins brought by inflationary effects and natural calamities. However, with ROAs near 2%, the company is barely breaking even.

Uniform Accounting tells us a different story—SPC’s profitability is significantly better at more robust levels reaching 14% in 2021, which is more than 7x its as-reported metrics.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

In 2021, SPC recognized PHP 902.4 million of interest income from its bank deposits, making up more than two thirds of its net income.

Removing PHP 902.4 million from SPC’s earnings along with the many other adjustments made leads to 14% Uniform earnings margin in 2021, higher than the as-reported earnings margin of 2%.

SPC Power Corporation’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that SPC’s profitability has been weaker than what real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROA has been understated. For example, as-reported ROA was 2% in 2021, but its Uniform ROA was way higher at 14%.

SPC Power Corporation’s Uniform asset turns are stronger than you think

For the past seven years, as-reported metrics have understated SPC’s asset turns, a key driver of profitability.

Moreover, since 2015, as-reported turns ranged from 0.2x-0.3x through 2021 while Uniform asset turns were able to reach a high of 1.5x.

SUMMARY and SPC Power Corporation Tearsheet

As our Uniform Accounting tearsheet for SPC Power Corporation (SPC:PHL) highlights, the company trades at a Uniform P/E of 22.0x, which is above the global corporate average of 18.4x but below its historical P/E of 26.7x.

High P/Es require high EPS growth to sustain them. In the case of SPC, the company has recently shown a 50% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, SPC’s sell-side analyst-driven forecast calls for a 5% Uniform EPS growth and an immaterial Uniform EPS growth in 2022 and 2023, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SPC’s PHP 9.40 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% annually over the next three years. What sell-side analysts expect for SPC’s earnings growth is above what the current stock market valuation requires in 2022, but below its requirement in 2023.

Furthermore, the company’s earning power is 2x the long-run corporate average. Meanwhile, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high dividend risk and moderate credit risk.

Lastly, SPC’s Uniform earnings growth is in line with peer averages in 2022, while the company is trading in line with its peer average valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com