This electronics company has been shockingly raking in profits that as-reported metrics aren’t computing

Amidst continued headwinds in the semiconductor industry, this company is still positioned to grow. Although as-reported metrics fail to show the whole story of the company’s profitability, Uniform Accounting reveals a more accurate with more robust Uniform ROAs.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 1980, the Ayala Corporation (AC:PHL) and Resins, Inc began a business joint venture to assemble integrated circuits with a workforce of around 100 employees. Eventually, the business would manufacture other products such as automotive hybrid integrated circuits and printed circuit boards.

Expanding its offerings in hardware and software design services, the business venture, Integrated Micro-Electronics (IMI:PHL), evolved into the complete electronics manufacturing service (EMS) provider it is today.

To further its growth, Integrated Micro-Electronics set up 21 manufacturing facilities in more than 10 countries throughout Asia, the Americas, and Europe. The company used this geographical presence to better serve its target market and mitigate any country-specific market risks.

By 2020, the company ranked 21st in revenues out of the top 50 EMS providers in the world as identified by the Manufacturing Market Insider. It was also recognized as the 6th largest EMS provider in the global automotive market based on the New Venture Research.

Even during the pandemic, customer demand for electronic products remained strong as Integrated Micro-Electronics reported revenues increased by 15% in 2021.

Going forward, one of the primary drivers for industry growth will be the rising demand for Internet of things (IoT) products.

For reference, IoT products are devices integrated with software that can connect with other devices to exchange information over the internet. Semiconductor chips are key components of these products.

Some of this integrated software can be found in smart mobiles with their voice assistants (Siri and Alexa), smartwatches with their fitness trackers, and autonomous vehicles (self-driving cars) with their equipped sensors to pick up information from their surroundings.

While revenue has grown, various headwinds continue to pressure the firm’s profitability: high material and labor costs in 2019, strict quarantine restrictions in 2020, and supply chain disruption in 2021.

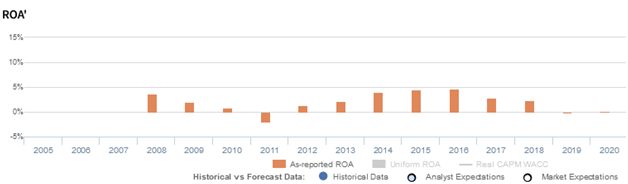

Looking at as-reported metrics, it appears that Integrated Micro-Electronics is barely profiting, with return on assets (ROAs) reaching immaterial levels since 2019.

However, Uniform Accounting tells us that this is a misrepresentation of Integrated Micro-Electronics’ profitability. In fact, the company’s Uniform ROA is more robust than what the as-reported figures show.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

For 2020, Integrated Micro-Electronics had a significant amount of excess cash sitting idly in its balance sheet for up to 16% of its as-reported total assets.

Integrated Micro-Electronics’ earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight, especially with recent years showing below cost-of-capital returns.

Through Uniform Accounting, we can see that the company’s true ROAs have been mostly understated in the past thirteen years. For example, as-reported ROA was immaterial in 2020, but its Uniform ROA was actually higher at 3%.

After declining from 4% in 2008 to negative levels in 2011, Uniform ROA expanded to 8% peaks in 2014-2015. Then, Uniform ROA collapsed to 2% in 2019, before rebounding to 3% in 2020.

Integrated Micro-Electronics is a more efficient business than you think

As-reported metrics significantly understate Integrated Micro-Electronics’ asset utilization. For example, as-reported asset turnover for the company was 1.0x in 2020, lower than Uniform asset turns of 1.4x, making the firm appear to be a less cost-efficient business than is accurate.

Moreover, as-reported asset turnover has never eclipsed beyond 1.7x, while Uniform asset turns have reached a peak of 2.6x in 2013, distorting the market’s perception of the company’s asset utilization over the past decade.

SUMMARY and Integrated Micro-Electronics, Inc. Tearsheet

As our Uniform Accounting tearsheet for Integrated Micro-Electronics, Inc. (IMI:PHL) highlights, the company trades at a Uniform P/E of 22.2x, around the global corporate average of 24.0x, but below its historical P/E of 39.1x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of Integrated Micro-Electronics, the company has recently shown a 169% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Integrated Micro-Electronics’ sell-side analyst-driven forecast is to see Uniform earnings shrink by 60% in 2021, but grow by 250% in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Integrated Micro-Electronics’ PHP 8.08 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 3% annually over the next three years. What sell-side analysts expect for Integrated Micro-Electronics’ earnings growth is below what the current stock market valuation requires in 2021, but above the requirement in 2022.

Moreover, the company’s earning power is below the long-run corporate average. However, cash flows and cash on hand are 2x above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals an average dividend risk.

To conclude, Integrated Micro-Electronics’ Uniform earnings growth is well below peer averages, and currently trades above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com