This firm is in the business of transforming data into useful insights, and Uniform ROAs of 80%+ highlight just how profitable it is

The amount of digital data produced and stored globally continues to increase at a rapid rate. This is why data analytics has become an essential business—raw data is meaningless unless it’s analyzed to produce useful insights.

This data analytics company was able to amass a considerable amount of data, mostly from acquisitions. It then used its data to build models and software to help its clients make better business decisions.

However, looking at as-reported metrics, it seems like its data isn’t as useful as it should be, generating only meager returns. On the contrary, TRUE UAFRS-based (Uniform) analysis shows that its extensive data library and analytics services have actually generated huge returns of more than 80%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Ever since the modern computer became internet-compatible, the digitalization of processes has increased rapidly, and innovations such as the cloud or AI have only further sped up its progress.

The growth surrounding digitalization has given rise to a new commodity: data. Just in the last nine years, the total amount of digital data globally has grown from about 2 billion terabytes to 59 billion terabytes currently—and it’s even expected to triple over the next five years.

In the ever-growing digital economy, they say that data is the new oil. It has become a valuable economic resource that can unlock useful insight when used properly.

In the context of oil, petroleum has no practical use just right off the ground. It has to be refined into fuel in order for it to power cars, planes, and other machinery. Similar to that, raw data is useless if not evaluated and analyzed correctly.

Satellite images of a Walmart’s parking lot are just images by themselves, but this data can be used to count foot traffic coming into the store, and potentially even roughly estimate revenues for a given period.

This process of transforming data into useful information is called data analytics.

Data analytics allows businesses to optimize their operations by identifying bottlenecks and streamlining processes. It also enables them to gauge market demand and adjust supply accordingly. Targeted content is also a popular use of data analytics, with big tech companies such as Google, Facebook, and even TikTok, analyzing user data to tailor the ads that show up.

Considering that businesses—or organizations, in general—generate huge amounts of data every single day, it only reinforces data analytics as a necessary tool to reveal trends or key metrics essential to operational sustainability.

One of the companies helping other businesses understand their data is Verisk Analytics (VRSK).

Verisk currently provides services in 30 different countries, with clients spanning the insurance, energy, and financial services markets. Over the half-century since its inception, the company has amassed an extensive amount of data from public sources, gathered industry data, but most of it comes from acquisitions.

Some of its more recent ones are PowerAdvocate, Wood Mackenzie, Maplecroft, MediConnect Global, and Aspect Loss Prevention. These are companies that either collect data, provide data analytics, or develop software to analyze industry data.

With its massive collection, Verisk is able to build models and software based on relevant market data, helping clients focus on risk management, value chain efficiency, and overall better business decision making.

Its collection of data is also a major competitive advantage, considering how Verisk is a leading provider to the US property/casualty insurance market, it gives the company considerable pricing power and also creates high barriers to entry for those looking to compete.

Overall, with the advent of the digital age and the digital economy, the data analytics industry is a thriving one that would likely persist for a very long time, and Verisk has the assets and necessary advantages to thrive along with it.

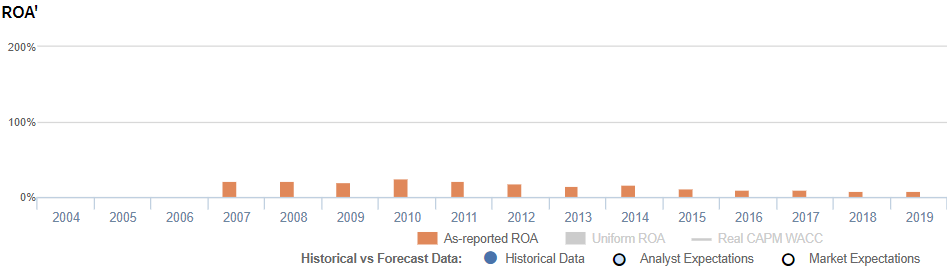

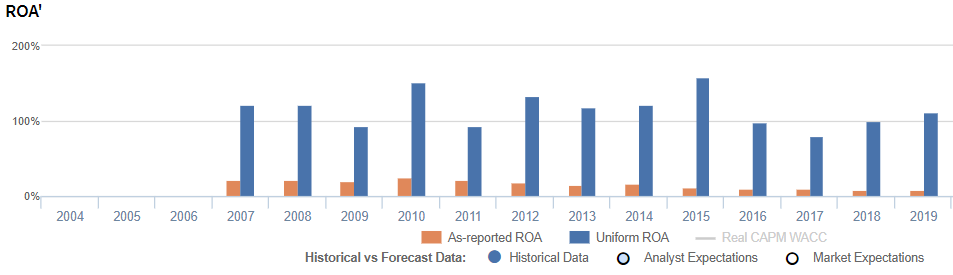

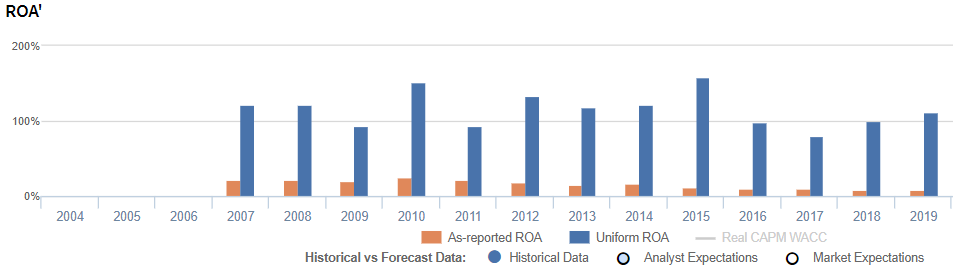

With the company’s indispensable data library and data analytics services, one can expect stellar returns. However, looking at as-reported return on assets (ROA), returns have been lackluster for the past thirteen years, ranging only from 8% to 25%.

In reality, Uniform Accounting reveals that the company is actually generating huge returns as expected, with Uniform ROAs ranging from 81% to 158%.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Verisk’s balance sheet. Due to the acquisitions made over the course of its operations to expand its collection of data, the company’s goodwill sits at about $2.5 billion to $3.8 billion, or at least 55% of its total assets in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Verisk’s earning power. Adjusting for goodwill, we can see that the company isn’t actually displaying meager performance. In fact, it is the opposite, with returns that are more than 8x greater.

Verisk’s earning power is actually far more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Verisk’s Uniform ROA has actually been higher than its as-reported ROA in the past thirteen years. For example, as-reported ROA was 8% in 2019, but its Uniform ROA was actually significantly higher at 112%. When Uniform ROA peaked at 158% in 2015, as-reported ROA was only at 12%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. Verisk’s Uniform ROA for the past sixteen years has ranged from 81% to 158%, while as-reported ROA ranged only from 8% to 25% in the same timeframe.

Verisk’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns slightly make up for it

Verisk’s volatility in profitability has been driven by trends in Uniform asset turns, coupled with a generally stable Uniform earnings margin.

After sustaining 4.7x-5.3x levels in 2007-2010, Uniform turns dropped to 3.2x in 2011 and recovered to 4.5x in 2015. Thereafter, Uniform turns faded to 3.0x in 2017, before improving to 3.5x in 2019.

Meanwhile, Uniform margins compressed from 24% in 2017 to 20% in 2009, before jumping to 29% in 2010. Since then, Uniform margins have stabilized at 27%-32% levels through 2019, excluding a 35% outperformance in 2015.

At current valuations, the market is pricing in expectations for further improvements in Uniform turns, accompanied by continued stability in Uniform margins.

SUMMARY and Verisk Analytics’ Tearsheet

As the Uniform Accounting tearsheet for the Verisk Analytics, Inc. (VRSK) highlights, its Uniform P/E trades at 38.6x, which is above the global corporate average of 25.2x and its historical average of 29.7x.

High P/Es require high EPS growth to sustain them. In the case of Verisk, the company has recently shown a 13% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Verisk’s Wall Street analyst-driven forecast is a 9% EPS growth in 2020 and a 1% EPS shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Verisk’s $193 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 13% each year over the next three years to justify current prices. What Wall Street analysts expect for Verisk’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 19x the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Verisk’s Uniform earnings growth is above its peer averages in 2020 while the company is also trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com