This freight company’s global expansion initiatives enabled it to deliver robust returns at 12%, not just at cost of capital

The demand for the shipment of essential goods and the rise of e-commerce have kept the freight and logistics industry going amid the pandemic, benefiting today’s company.

However, as-reported metrics do not seem to show how this company’s efforts to expand its global network through partnerships and acquisitions positively affect its returns. Uniform Accounting shows that the business has a better Uniform return on assets (ROA) than what you might think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

In the earlier part of the COVID-19 pandemic, the lockdowns and border closures around the world caused restrictions on movement of goods, disrupting global supply chains. This delay caused backlogs in major sectors internationally.

Eventually, transport of goods resumed, and with most places still on lockdown, more people turned to deliveries as a way to do their shopping. That trend accelerated the growth of e-commerce, boosting both local and global freight activity.

Furthermore, the urgency of the vaccine rollout all over the world has increased demand for air cargo since it is the best way to deliver vaccines on time. This additional demand helped set the industry on its way to recover to pre-pandemic levels.

One such company is taking advantage of these trends.

Kintetsu World Express (KWE) has been in this business since 1948 and now has international freight operations in 46 countries and 312 cities. It was able to expand its global reach through joint ventures and acquisitions.

In 2012, KWE signed a joint venture agreement with India-based provider Gati to form Gati-Kintetsu Express Pvt. Ltd., offering express distribution and supply chain solutions across the Asia Pacific region and SAARC countries.

KWE also acquired APL Logistics in 2015, enabling the company to increase its competitiveness with its U.S. and European rivals. APL Logistics was also able to offset revenue declines at other KWE units.

Today, KWE continues to expand its business in Asia, opening new warehouses in China, Thailand, and Malaysia.

Because of its growing global footprint and strategic acquisitions, investors would expect the company to have robust returns.

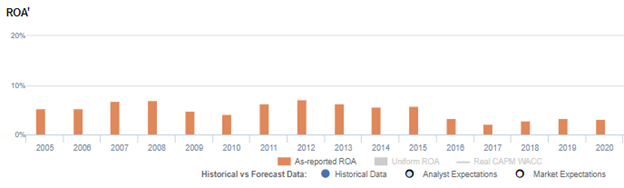

However, as-reported metrics show that the company’s profitability has been weak for the past sixteen years, ranging only from 2% to 7%.

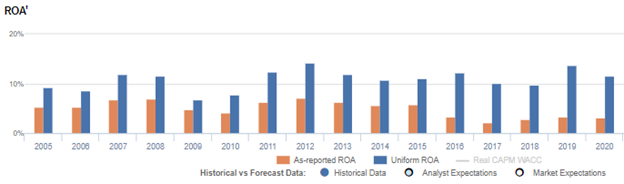

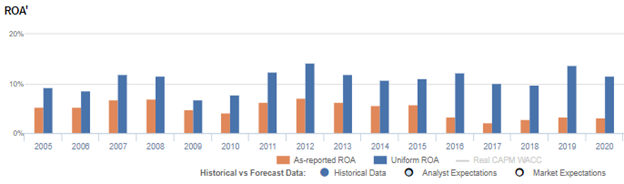

This is an inaccurate representation of KWE’s profitability. Using Uniform Accounting we can see that the company’s returns are actually stronger than what as-reported metrics show, ranging from 7% to 14%.

One metric that causes distortions in as-reported ROAs is the company’s massive amortization expense.

Amortization expense is generated from the company’s use of intangible assets in a given reporting period. As such, it is a non-cash expense that is spread throughout the intangible asset’s useful life. As a non-cash expense, it does not represent an actual cash outflow.

Deducting amortization expense from the company’s revenues distorts its profitability because there is no actual cash flow that happens when amortization is charged.

Adding back amortization expense is necessary to convert the company’s net income into actual cash flows.

After amortization expense and other significant adjustments are made, we can see that KWE has better profitability than what as-reported metrics show. Currently, the company’s Uniform ROA is 3x stronger than what the market sees.

Kintetsu World Express’ profitability is much more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

KWE’s Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, when Uniform ROA was at 14% in 2012, as-reported ROA was only half that at 7%.

The company’s Uniform ROA for the past sixteen years has ranged from 7% to 14%, while as-reported ROA has ranged only from 2% to 7% in the same timeframe.

Specifically, Uniform ROA gradually climbed from 9% in 2005 to 12% in 2007, before declining to 7% in 2009. It then peaked to 14% in 2012, before trending to 10%-12% in 2013 to 2018. Uniform ROA then recovered to 14% in 2019, then declined to 12% in 2020.

Kintetsu World Express’ Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in both Uniform earnings margin and Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform margins gradually rose from 2% in 2005 to 4% levels in 2012, before fading to 2% in 2018. It then recovered to 3% in 2020.

Meanwhile, Uniform turns remained stable at 3.8x-4.1x levels from 2005 to 2009, before falling to 3.1x in 2010. It then recovered to 4.5x in 2019 before falling to 3.5x in 2020.

SUMMARY and Kintetsu World Express, Inc. Tearsheet

As the Uniform Accounting tearsheet for Kintetsu World Express, Inc. (9375:JPN) highlights, the Uniform P/E trades at 9.9x, which is below the global corporate average of 23.7x but around its own historical average of 10.9x.

Low P/Es require low EPS growth to sustain them. In the case of KWE, the company has recently shown a 1% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, KWE’s sell-side analyst-driven forecast is a 74% EPS growth in 2021 and a 9% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify KWE’s JPY 2,477 stock price. These are often referred to as market embedded expectations.

KWE is currently being valued as if Uniform earnings were to shrink 3% annually over the next three years. What sell-side analysts expect for KWE’s earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, the company’s earning power is 2x above the long-run corporate average. Also, cash flows and cash on hand are more than 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, KWE’s Uniform earnings growth is above its peer averages, but the company is also trading significantly below its average peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com