This hotel giant’s focus on its business model might continue to accommodate Uniform ROAs of 94%+ levels going forward

The hotel industry took a major hit, as global tourism ground to a halt due to people staying at home to slow the spread of the novel coronavirus.

This hotel giant’s operations have been interrupted as well, with occupancy rates in most regions down to new lows. While near-term headwinds are disrupting the business, the company’s business model and acquisitions might accelerate profitability when the economy recovers.

However, while as-reported metrics show that their strategy might not be accretive, TRUE UAFRS-based (Uniform) analysis shows that this has actually helped the company reach record highs and will continue this streak in the following years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The World Travel and Tourism Council reported that about $8.8 trillion, or 10% of the world’s total GDP, can be attributed to the travel industry as of 2018.

However, the entire industry ground to a halt when the novel coronavirus became a serious threat. Governments around the world locked down their borders, tightened travel regulations, and ordered people to stay home.

Many components that fuel the industry, such as airlines, hotels, and travel agencies, were also adversely impacted, with almost all of them relying on tourists for revenues.

Some regional airlines in the US, UK, and Australia have already filed for bankruptcy. Cruise lines have grounded their ships indefinitely, and casinos and hotels have seen little to no foot traffic in the past couple of months.

While the airline space seems to be taking the brunt of the blow, hospitality businesses aren’t doing so well either.

Demand for hotels has decreased dramatically, with some hotels closing temporarily while others implement provisional layoffs of thousands of workers.

Marriott (MAR), one of the largest hotel chains in the world, has seen occupancy rates drop below 25% in North America and down to a bottom of just 2% in China. These two geographical segments are where a majority of their revenues are sourced.

However, though the outlook appears grim for this hotel giant, its business strategy might be the key to accelerating fundamental improvements once the economy recovers.

Like major hotel brands, Marriott follows a franchising strategy. The company essentially lends their brand to a third party, who then builds and runs the operations of the franchised property in exchange for a fee.

Consequently, with 70% of their hotels under franchise instead of direct ownership, the company is incredibly asset light, which results in lower fixed costs and less volatile profits.

This setup also allows Marriott to grow its international footprint without having to shell out massive investments in capex.

However, this strategy wouldn’t have been successful if Marriott did not have a wide collection of strong and recognizable brands in the first place.

Their brands can be categorized into three distinct tiers: luxury, premium, and select. The luxury and premium brands, such as the Ritz-Carlton or the Sheraton, cater to higher income customers while the select brands, like Fairfield and Courtyard, are generally more affordable.

Furthermore, Marriott has been expanding their portfolio through acquisitions. Their more recent ones, Starwood Hotels and Elegant, increased property numbers by more than 6,000 across 100+ countries.

What’s compelling about these acquisitions is that they also grow the number of brands that the company can license out to franchisees.

With an expanding collection of household names and an aggressive franchising strategy, it is expected that Marriott would see a significant acceleration in returns over the next five years.

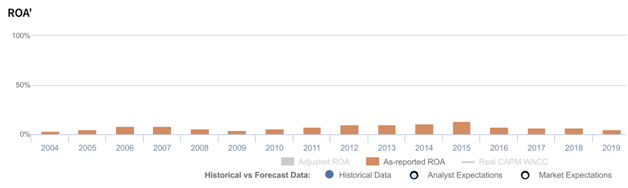

However, looking at as-reported ROAs, it seems that the company’s franchising model hasn’t been lucrative.

After rising to a peak of 13% in 2015, as-reported ROA has since fallen back to 5%-8% lows. As-reported metrics would have signaled to investors that the company’s Starwood acquisition in 2016 hasn’t been synergistic. It would appear as if Marriott has struggled to convert their business to a more pure-play franchising model.

In reality, ROAs have actually gone up to record highs using Uniform Accounting, opposite to what as-reported metrics would tell you.

The distortion comes from as-reported metrics failing to consider the amount of goodwill on Marriott’s balance sheet, which is substantial given their many acquisitions in recent years.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Marriott’s earning power. Once you adjust for goodwill, returns are actually 5x-15x greater.

The company’s acquisition of Starwood Hotels, which grew their portfolio and strengthened their franchising power, didn’t destroy value as the decline in as-reported ROA from 13% in 2015 to just 5% in 2019 would suggest.

Instead, Uniform ROAs have shot up to new highs of 91% before fading to 77% in 2019—still above the pre-acquisition ROA of 70%.

While concerns about the pandemic might disrupt operations and revenues for Marriott in the short-term, the successful execution of their franchising business model would likely continue the company’s ROA momentum in the long-term.

Marriott’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Marriott’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 5% in 2019, but its Uniform ROA is actually 15x higher at 77%. When Uniform ROA peaked at 91% in 2017, as-reported ROA was just at 7%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. Marriott’s Uniform ROA for the past sixteen years has ranged from 8% to 91%, while as-reported ROA ranged only from 4% to 13% in the same timeframe.

After jumping from 27% in 2013 to 42% in 2014, Uniform ROA further increased to 70% in 2015. Afterwards, Uniform ROA reached its peak at 91% levels in 2017 before declining to 77% in 2019.

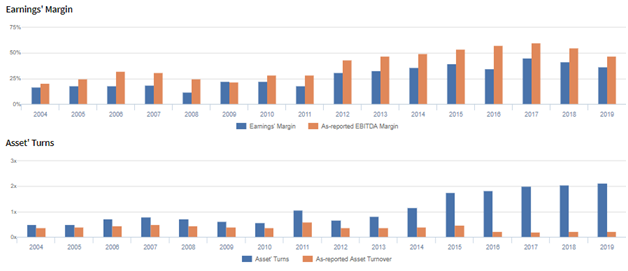

Marriott’s margins are weaker than you think, but it is significantly offset by the trend in Uniform asset turns

Marriott’s improving profitability has been driven by trends in both Uniform earnings margins and Uniform asset turns.

From 2004-2006, Uniform earnings margins remained stable at 17% to 19% levels. It then gradually improved to 40% in 2015, before falling to 35% in 2016. Thereafter, Uniform margins increased to a peak of 45% in 2017 before stabilizing to 36% levels in 2019.

Meanwhile, Uniform asset turns remained at 0.5x to 0.8x levels from 2004-2010. It then improved to 1.2x in 2014, which further increased to 1.8x to 2.1x levels through 2019.

At current valuations, markets are pricing in expectations for expanding Uniform margins and stable Uniform turns near current peak levels.

SUMMARY and Marriott Tearsheet

As the Uniform Accounting tearsheet for Marriott International, Inc. (MAR) highlights, the Uniform P/E trades at 37.5x, which is above corporate average valuation levels, but below its own recent history.

High P/Es require average EPS growth to sustain them. In the case of Marriott, the company has recently shown a 9% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Marriott’s Wall Street analyst-driven forecast is a 64% shrinkage in 2020, and a 174% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Marriott’s $80 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 3% each year over the next three years. What Wall Street analysts expect for Marriott’s earnings growth is below what the current stock market valuation requires in 2020 but is above that requirement in 2021.

The company’s earning power is 13x the corporate average. However, cash flows sufficiently cover its total obligations—including debt maturities, capex maintenance, and dividends—up until 2024 when it reaches a material debt headwall. Together, this signals moderate credit and dividend risk.

To conclude, Marriott’s Uniform earnings growth is below peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com