This Japanese company is conveniently using its localization strategy in international markets, resulting in a stronger Uniform ROA of 6%!

Convenience stores are popular because they offer a wide range of products from packaged goods to cooked meals, all in one convenient location. Open 24/7, they’ve also become a great source of emergency supplies, which is why customers don’t mind if their products are priced higher than the suggested retail prices.

This “konbini,” as the Japanese call convenience stores, has been expanding its reach globally. With its localization strategy, it is winning the hearts of the locals in its target countries. However, as-reported metrics do not show that, showing that the company is weaker than it actually is.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

As the smallest segment of the grocery market in the Philippines, convenience stores were able to expand its coverage at a faster pace than larger segments, having the highest growth in sales at 8% in 2018. According to Euromonitor, convenience stores saw a 21% current value growth in 2019, reaching PHP 68.5 billion in sales in the Philippines.

Neighboring nations are seeing the same growth, with convenience stores growing rapidly in Indonesia, Vietnam, and China. According to the International Grocery Research Organization (IGD), Vietnam will be Asia’s fastest-growing convenience store market by 2021, followed by the Philippines and Indonesia.

Due to urbanization and a fast-paced lifestyle, convenience stores have become an increasingly important part of daily life for many Filipinos.

Convenience stores are convenient for a number of reasons. One, they offer a wide assortment of products, making it an easy stop for customers to buy what they need. Another reason is that convenience stores are open for longer hours than other groceries or sari-sari stores. Finally, these stores are also strategically located where most people can easily get to them.

One of the convenience stores that are currently gaining popularity in the Philippines is Lawson.

Lawson, Inc. was founded on April 15, 1975, and is headquartered in Tokyo, Japan. As of May 2020, Lawson has 14,469 stores located throughout Japan. It is continuously rebuilding its store portfolio and expanding its franchised stores in high-traffic areas. For example, department store basements in Japan have become the ideal locations for new store openings.

Lawson is focused on increasing its store count overseas, especially in Asian countries.

One of the numerous strategies that Lawson has implemented is a localization effort in its international markets that includes expanding its number of franchisees, working with local organizations, and acquiring local brands to accelerate convenience store expansion.

In China, for instance, Lawson was one of the primary challengers to enter the Chinese market, having established Shanghai Hualian Lawson Co. Ltd. in 1996.

Lawson was initially unsuccessful in increasing its number of stores in China and making a profit. However, the company decided to change its strategy in the early 2000s by entering county-level urban areas with populations of 500,000.

Moreover, the company worked with local organizations to comprehend local spending habits and obtain prime store locations. Lawson also started to appoint more local Chinese staff to replace the Japanese staff. This strategy succeeded and in 2003, Lawson began to boom in China.

The company began to rapidly broaden its presence abroad in 1996, seeing enormous room for development in other countries. Today, the Philippines is the fifth country abroad to open a Lawson store, following Lawson’s entry into China, Indonesia, the United States, and Thailand.

In March 2015, PG Lawson, Inc., a joint venture organization between Lawson Asia Pacific Holdings Ptd. Ltd and Puregold Price Club, Inc. opened the first Lawson store in Sta. Ana, Manila.

However, in 2018, Puregold pulled out of the minimart business, selling all its joint venture shares to Lawson.

Lawson then partnered with Philippine conglomerate Ayala Corporation in October 2019. It also had plans of teaming up with Ayala’s online retail business to transform convenience stores into item pickup stations as well.

With the help of Ayala, Lawson plans to grow to around 500 stores in the Philippines by 2024, a ten times increase from the 50 stores that are currently open, as it pushes forward with an aggressive foreign expansion.

Lawson’s strategy is to offer products that people in its specific location can culturally relate to. For example, Lawson stores in the Philippines offer Filipino food like kaldereta or menudo, and even fried chicken served with unlimited rice.

Adapting in international markets through its localization strategy can help Lawson best satisfy its customers in different countries. Given this strategy of understanding the market’s cultural preferences, one would expect that the company can increase its profitability and further grow its presence in these countries, as shown with its efforts here in the Philippines.

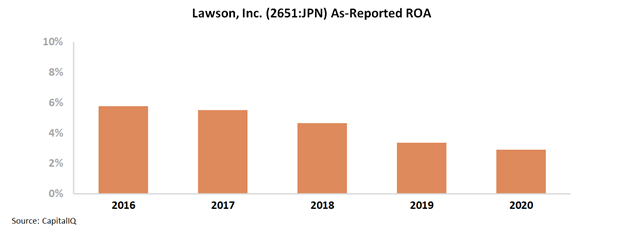

However, as-reported metrics make it look like Lawson has weakening returns, declining from 6% in 2016 to just 3% in 2020.

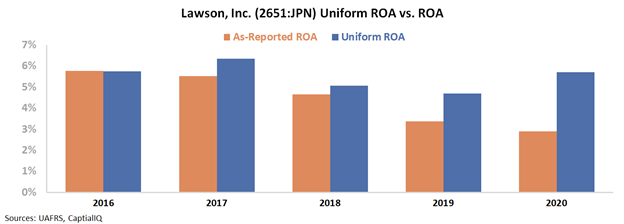

Uniform Accounting paints a different picture. In recent years, Lawson’s Uniform ROA has been more robust than what the market thinks. Uniform ROA currently sits at 6%, which is double the as-reported ROA of 3%.

The distortion comes from as-reported metrics failing to consider the number of operating leases Lawson has from its numerous existing retail stores.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, does not get treated as an investment, but as an expense that would impact the income statement.

Specifically, operating leases on Lawson’s income statement are understating the company’s true earnings. After adjusting for the rent expense distortion, we can see that returns actually bounced back to 6%, which is double the current as-reported ROA of 3%.

Lawson’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight. Lawson’s Uniform ROA has been higher than its as-reported ROA in recent years. For example, Uniform ROA is at 6% in 2020, while as-reported ROA is just 3%.

The company’s Uniform ROA for the past five years has remained at 5%-6% levels, while as-reported ROA has been declining from 6% to 3% in the same time frame.

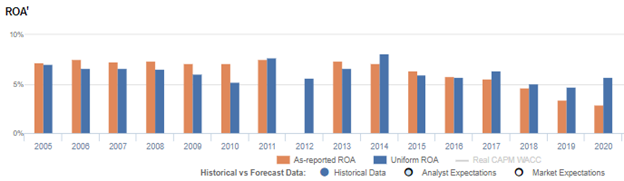

After falling from 7% in 2005 to 5% in 2010, Uniform ROA rose to 8% in 2014 before declining again to 5% in 2019. Then, Uniform ROA increased to 6% in 2020.

Lawson’s Uniform earnings margins are weaker than you think

Volatility in Uniform ROA has been driven by weak Uniform earnings margins. In fact, Uniform margins have been lower than as-reported EBITDA margins in each of the past sixteen years.

As-reported EBITDA margins steadily declined from a peak of 24% in 2005 to 17% in 2010, before recovering to 24% in 2014. It then gradually faded to 20% in 2020.

Meanwhile, after contracting from 15% in 2005 to 9% in 2010, Uniform margins improved to 14% levels in 2014 before gradually falling to 9% in 2020.

SUMMARY and Lawson, Inc. Tearsheet

As the Uniform Accounting tearsheet for Lawson, Inc. (2651:JPN) highlights, its Uniform P/E trades at 42.3x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Lawson, the company has recently shown a 15% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Lawson’s sell-side analyst-driven forecast is a 68% earnings shrinkage in 2021, followed by a 68% earnings growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lawson’s JPY 4,830 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 1% each year over the next three years and still justify current prices. What sell-side analysts expect for Lawson’s earnings is well below what the current stock market valuation requires in 2021, but significantly above that requirement in 2022.

The company’s earning power is around the corporate average. Additionally, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Lawson’s Uniform earnings growth is well below its peer averages in 2020. However, the company is trading above its peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com