This mall company still became the star of the show despite trying times, shining at Uniform ROAs of 7%+ in recent years

Venturing into the retail and commercial segment has been a common practice among real estate companies. That is why this mall and office developer company was acquired by one of the largest home developers in the country.

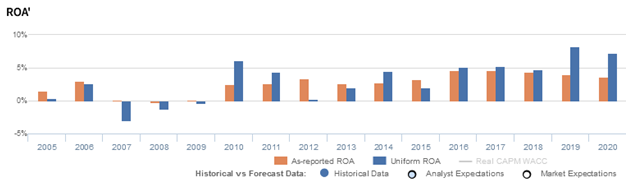

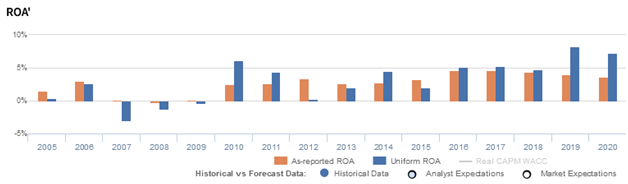

Although its as-reported metrics do not show it, the company’s ability to remain profitable despite the pandemic enabled it to reach Uniform ROAs of more than 7% in the past two years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

A couple of months ago, we established that operating in the real estate industry is more than just your regular DIY project. For starters, having big competitors is already in and of itself a challenging feat to overcome.

That is why most of these real estate companies have been successful at remaining profitable, constructing different kinds of properties that cater to all income segments.

A tried and tested strategy is to venture into the retail and commercial segment, building leisure and entertainment malls in some of the most populated areas in the country—such as Makati, BGC, and Manila.

Some firms like SM Prime Holdings, Inc. (SMPH:PHL) did this by creating its SM supermall chain, making it the largest mall operator in the country. On the other hand, others opted to acquire existing malls, like how Vista Land (VLL:PHL) acquired mall and office developer Starmalls, Inc. (STR:PHL), which is the company we are going to talk about today.

Even before Starmalls was acquired and renamed Vistamalls, Inc., the company had already been producing a diverse set of offerings, bringing its customers a better shopping experience, with malls operating in Bulacan, Cavite, Bataan, and Taguig, to name a few.

After the acquisition, “Vistamalls” was able to gain more traction in the retail space because of Vista Land’s name. This enabled the company to expand its reach and sport the holding company’s exclusive stores, including AllDay, AllHome, and Coffee Project.

Furthermore, this transaction, coupled with the continued network growth in shopping malls, contributed to Vistamalls’ net income jumping 71% to PHP 1.6 billion in 2016.

Since then, the company’s profitability has been in an upward trend.

However, when the pandemic hit, malls were severely affected as people were forced to remain at home. As a result, the company had to alter the way it operates by shifting its business online.

While the SM Group (SM:PHL) has developed its own online shopping channels—ShopSM and THE SM STORE—Vistamalls partnered with logistics provider GetAll. Through this partnership, the company was able to create a shopping service under a unified hotline, which is currently operational across the Vista group’s 30-mall network.

On top of that, Vistamalls launched its DropBuy service to help its customers conveniently pick up their pre-ordered items at easily accessible areas.

Due to these initiatives, the company was still able to report a net income of PHP 2.7 billion in 2020, which was up 4% from the previous year’s PHP 2.6 billion.

Overall, the company’s ability to efficiently adapt to the pandemic further strengthened its position in the real estate industry.

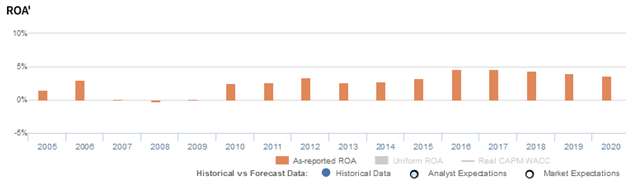

However, looking at the as-reported metrics, the company continued to produce returns near cost-of-capital levels, implying that Vistamalls hasn’t generated enough profitability since 2005.

In reality, the company’s real economic profitability has actually been more than the as-reported metrics since being acquired.

What as-reported metrics fail to consider is how current liabilities are factored into the ROA calculation. Traditional ROA calculations for measuring a firm’s earning power only include current and long-term assets as part of the cost of investment.

However, a company’s ability to receive goods and services in advance of payments—the current operating liabilities—ought to be factored in as well.

Current liabilities (excluding short-term debt) are necessary for operations. Items such as accounts payable, accrued expenses, and others are used to maintain the firm’s current capital position. On the other hand, long-term liabilities are mostly just used to finance the business.

If a company has a ton of cash to service its current liabilities and we only factor in its cash, it would make the company look inefficient. In reality, the company is just being responsible by building liquid assets to meet short-term obligations.

As such, net working capital (current assets – current liabilities) is used for the firm’s ROA calculation. This shows a company’s real cash management ability and thereby, its true earning power.

In the case of Vistamalls, the as-reported metrics’ asset base for ROA calculation is at PHP 73.7 billion in 2020, leading to a 4% as-reported ROA.

However, when subtracting current operating liabilities and applying other needed adjustments, we arrive at Vistamalls’ PHP 28.1 billion Uniform assets, resulting in an 8% Uniform ROA.

Vistamalls’ profitability is stronger than you think in recent years

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

For example, Uniform ROA for Vistamalls was 8% in 2019, substantially higher than the as-reported ROA of 4%, making the company appear to be a much weaker business than real economic metrics highlight for the past six years.

Moreover, since 2005, Uniform as-reported ROA reached a peak of 8, while as-reported ROA has not eclipsed past 5% in the same time frame, substantially distorting the market’s perception of the firm’s ceiling.

Vistamalls’ Uniform earnings margins are weaker than you think but its Uniform asset turns make up for it in recent years

General improvements in Uniform ROA have been driven primarily by Uniform earnings margin, and to a lesser extent, Uniform asset turns.

After falling from 0.2x levels in 2005-2006, Uniform turns fell to immaterial levels, before gradually expanding 0.3x levels in 2019-2020.

Meanwhile, after improving from negative levels in 2007 to a peak of 77% in 2010, Uniform margins compressed to 3% in 2012. Since then, Uniform margins have oscillated from 17% to 37%.

SUMMARY and Vistamalls, Inc. Tearsheet

As our Uniform Accounting tearsheet for Vistamalls, Inc. (STR:PHL) highlights, the company trades at a Uniform P/E of 18.3x, below the global corporate average of 24.0x, and its historical P/E of 24.5x.

Low P/Es require low EPS growth to sustain them. In the case of Vistamalls, the company has recently shown an 18% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Vistamalls’ sell-side analyst-driven forecast is to see Uniform earnings growth of 6% in 2021, but a shrinkage of 5% in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Vistamalls’ PHP 3.69 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink immaterially over the next three years. What sell-side analysts expect for Vistamalls’ earnings growth is below what the current stock market valuation requires in 2021, but above the requirement in 2022.

However, the company’s earning power is 1x the long-run corporate average. Moreover, cash flows and cash on hand are above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend risk.

To conclude, Vistamalls’ Uniform earnings growth is above peer averages, but it currently trades above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com