This multinational food company continues to build its brand with multiple initiatives, raising its Uniform ROA to 7%, not 6%

This food and beverage company capitalized on its initiatives to continue to grow amid rising inflation levels. However, looking at its as-reported data, it seems that the company’s ability to navigate challenges and making the most of its opportunities aren’t being accurately reflected.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Since its foundation by John Gokongwei Jr. in 1954, Universal Robina Corporation (URC:PHL) has produced countless food products that have become household names in the Philippines and around the world. Jack ‘n Jill snacks, C2 ready-to-drink teas, and Great Taste coffee are just some of their well-known brands.

Universal Robina took multiple steps to achieve record sales in 2022.

Compared to 2021, the company saw net income rise by 12% to PHP 14.5 billion, as well as a 20% increase in its operating income. Its branded consumer foods segment reported a 29% growth in total sales while its agro-industrial and commodities divisions saw an increase by 26%.

URC CEO and president Irwin Lee cited the importance of the opportunities that 2022 presented and how the company was able to take advantage of the reopening of the economy.

Partnerships and acquisitions have been one of the key initiatives for Universal Robina.

Its partnership with Asahi Beverages Philippines allowed the company to enter the cultured-milk segment. Its latest acquisition Munchy Food Industries, on the other hand, has just started to roll out its products in the Philippine market, since URC just closed the acquisition of Malaysia’s top biscuit company in late 2021.

This strategy has enabled URC to build a strong portfolio of brands that resonate with a wide range of consumers.

Furthermore, URC is highly committed to sustainable growth. The company implements sustainability programs in its operations, such as waste management and energy efficiency initiatives, and supports community development projects in the areas where it operates.

Lastly, Universal Robina saw robust growth in its international business segment in 2022, particularly in Indonesia and Thailand.

Overall, Universal Robina seems to be finding success in their various initiatives and strategic executions. However, as-reported metrics seem to be sleeping on this company’s profitability.

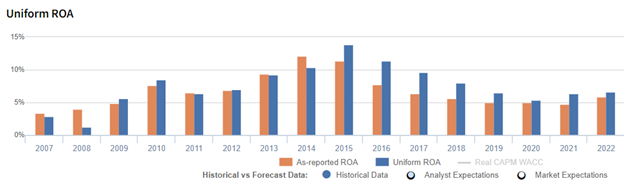

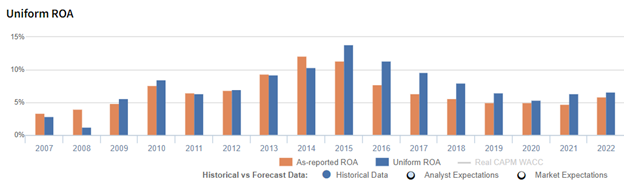

In reality, the company’s aggressive focus on its growth strategies enabled Universal Robina to achieve a Uniform ROA of 7%.

One of the distortions between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on URC’s balance sheet. The company’s goodwill sits at about PHP 24.2 billion in recent years, which was approximately 14% of its total assets, stemming from the acquisitions over the course of its operations.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of URC’s earning power. Specifically, if we remove goodwill along with the other necessary adjustments in Uniform Accounting in 2022, Universal Robina Corporation should be recognizing PHP 7 billion less in assets and a 7% Uniform ROA.

Universal Robina’s profitability is stronger than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

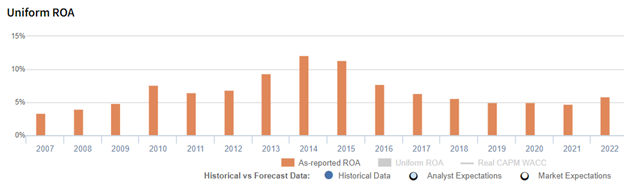

For example, Uniform ROA for Universal Robina was 7% in 2022, higher than the as-reported ROA of 6%, making the company appear to be a weaker business than real economic metrics highlight for the past eight years.

Moreover, since 2018, Uniform ROA has reached a high of 8%, while as-reported ROA has failed to eclipse 6% in the same time frame, substantially distorting the market’s perception of the firm’s ceiling.

Universal Robina has a more efficient business than you think

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

From 2016-2022, as-reported asset turnover ranged from 0.6x to 0.9x, while Uniform turns reached highs of up to 1.1x, making the company appear to be a less efficient business than real economic metrics reveal.

Moreover, as-reported asset turnover has been lower than Uniform turns in each of the past eight years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Universal Robina Corporation Tearsheet

As our Uniform Accounting tearsheet for Universal Robina Corporation (URC:PHL) highlights, the company trades at a Uniform P/E of 25.0x, above the global corporate average of 18.4x but below its historical P/E of 29.7x.

High P/Es require high EPS growth to sustain them. In the case of Universal Robina, the company has recently shown a 26% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Universal Robina’s sell-side analyst-driven forecast is to see Uniform earnings shrinkage of 27% and a growth of 15% in 2023 and 2024, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Universal Robina’s PHP 148.30 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 10% per year over the next three years. What sell-side analysts expect for Universal Robina’s earnings growth is above what the current stock market valuation requires in 2023 and 2024.

Moreover, the company’s earning power is in line with the long-run corporate average. Additionally, cash flows and cash on hand are 4x of total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate credit risk and a low dividend risk.

To conclude, Universal Robina’s Uniform earnings growth is in line with its peer averages, and in line with its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com