This packaged food company does more than leaven bread, its Uniform ROA has risen to 2x corporate averages…as-reported metrics say it’s fallen flat

Though rice has long been Filipinos’ staple food, low flour prices and shifting diets of the middle class are driving the growing flour demand. Based on Euromonitor, growth in per capita wheat foods in the Philippines has increased by 45% from 23.1 kg in 2014 to 33.7 kg in 2019.

This is the reason why this food packaging company is continuously generating robust UAFRS-based (Uniform) profitability. However, as-reported metrics are claiming the company to be a much weaker business.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Archeological evidence suggests that flour has been around since Ancient Rome, particularly for breadmaking.

The oldest techniques for producing flour were by grinding seeds or roots through a stone mortar and pestle. Then the Ancient Greeks discovered they could grind seeds using watermills, and then by windmills. When the Industrial Age began, flour mills were powered by steam with rollers which were metal or porcelain.

With the technology, different varieties of wheat have been produced, enriched with iron, niacin, and other vitamins.

Since then, flour is not only made for bread but also the main ingredient of numerous favorites such as pancakes, pasta, and crackers.

The vitamins and additional nutrients flour offers have made it a staple in households across the globe. China, the European Union, and India are top consumers of this raw ingredient. In recent years, even Filipinos who are known to prefer rice over bread or pasta have started choosing whole wheat alternatives for health reasons.

RFM Corporation (RFM:PHL) is benefiting from this shift in Filipino diet.

Established in 1957, the company is known to be the pioneer in the flour-milling industry in Asia. It supplies several bakeshops, as well as manufacturing biscuits, noodles, and other flour-based products in the country.

After 30 years in the flour milling business, RFM expanded to packaged products and introduced its hotcake, cake, and ingredient mixes.

Then, between 1990 and 2000, RFM decided to develop and expand its business further outside its current core business. One of its notable business ventures is its partnership with Unilever to produce Selecta, a well-known brand of ice cream and milk, in 1999.

Despite its efforts to expand its business and attract more customers, RFM’s stock price has not done well. From PHP 3.9 per share in its initial public offering in 1995, RFM traded below PHP 1.0 until it achieved its low levels in 2009. This stock price decline can be explained by its declining revenue and increasing costs attributable to higher fuel prices.

When fuel prices started to decline, RFM revenue and costs improved, leading to its stock price peaking at PHP 6.6 in May 2014. During this year, the company acquired Royal pasta brand to dominate market leadership in the pasta market with their Fiesta brand.

However, as the company was on its way to recovery, competition in the flour and packaged business became more intense due to the influx of imported products and arrival of new players in the market.

Still, the company managed to maintain its above cost-of-capital profitability in 2015-2019. Additionally, even with the COVID-19 pandemic, RFM was also still able to declare cash dividends last July. This indicates management’s confidence that the firm’s balance sheet and cash position remain strong.

However, as-reported metrics do not see how essential the products of RFM are. Over the years, these metrics have been incorrectly portraying the company as a less profitable business.

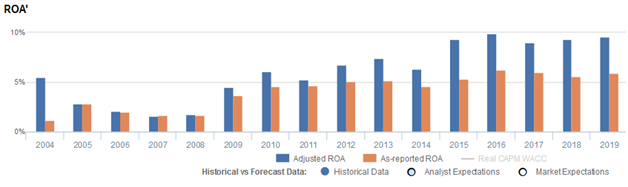

In 2019, as-reported ROA only shows 6%, while Uniform ROA was significantly higher at 10%.

Much of the distortion comes down to how excess cash is treated. In as-reported financials, RFM’s entire cash balance is treated as part of its asset base. Meanwhile, Uniform Accounting removes the cash as it is not necessary to operate and fulfill obligations–cash above what one might view as “operating” cash.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

Since RFM has maintained a substantial cash balance each year, the company’s true asset base has been materially inflated each year.

For example in 2019, RFM’s excess cash amounted to PHP 3.5 billion or 19% of the company’s PHP 19 billion as-reported assets. By removing excess cash, along with all the other necessary adjustments in Valens makes, we arrive at a PHP 11 billion true asset base in 2019. This led to a Uniform ROA of 10%.

RFM’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

RFM’s Uniform ROA has actually been higher than its as-reported ROA for fifteen of the past sixteen years. Most recently, as-reported ROA was 6% in 2019, but Uniform ROA shows a much stronger profitability of 10%.

Through Uniform Accounting, we can see that the company maintains above cost-of-capital ROAs since 2012. Additionally, Uniform ROA has generally improved from 5% in 2009 to 10% in 2019.

Meanwhile, as-reported ROA has only improved from 4% to 6% levels in the same time frame.

RFM’s asset utilization is more efficient than you think

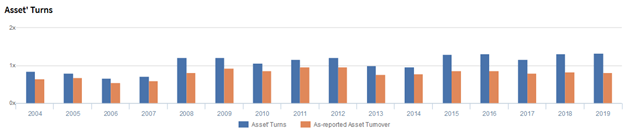

RFM’s profitability has been driven primarily by stronger asset turns, a key driver of profitability.

Uniform asset turns improved from 0.7x-0.8x levels in 2004-2007 to 1.1x-1.2x levels in 2008-2012, before fading to 1.0x levels in 2013-2014. Thereafter, Uniform turns ranged from 1.2x-1.3x in 2015-2019.

As-reported metrics have been making the firm appear to be a less asset efficient business than real economic metrics highlight.

SUMMARY and RFM Corporation Tearsheet

As the Uniform Accounting tearsheet for RFM, the Uniform P/E trades at 12.7x, which is currently below corporate average valuation levels and its own history.

Low P/Es require low EPS growth to sustain them. In the case of RFM, the company has recently shown a 6% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, RFM’s sell-side analyst-driven forecast calls for a 7% Uniform EPS growth in 2020 followed by an immaterial decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify RFM’s PHP 4.50 stock price. These are often referred to as market embedded expectations.

The company can have its EPS shrink by 9% each year over the next three years and still justify current valuations. What sell-side analysts expect for RFM’s earnings growth is above what the current stock market valuation requires in 2020 and in 2021.

Furthermore, the company’s earning power is almost 2x the long-run corporate average. Additionally, cash flows and cash on hand are more than 4x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, RFM’s Uniform earnings growth is around peer averages, and the company is trading below its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus ”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com