This popular chocolatier indulged in healthy acquisitions, with Uniform ROAs now reaching sweet new highs of 30%+

Known for its widely popular line of confectionery items, this chocolate company decided to expand its portfolio by improving some of its core brands and venturing into a market you’d least expect it to: the healthy snack industry.

While as-reported data suggests that the strategic move to capitalize on another market is creating less profitability for the company, Uniform Accounting shows that it has actually helped Uniform ROAs reach new highs of more than 30%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Milton Hershey, one of the most famous confectioners in the world, has had an undeniable love for candies ever since his mother sent him off to learn the ways of candy making.

This passion-turned-opportunity eventually led him to establish the Lancaster Caramel Company in 1886. After learning that caramels sold better in bulk, his venture became an instant success. During one of his many travels, he came across another ingredient that would earn him his legacy—chocolates.

Shortly after experimenting and applying chocolate coating on his caramel candies, he decided to sell his caramel company for $1 million and build an empire that was purely focused on his chocolate creations, naming it the Hershey Chocolate Company (HSY).

For decades, some of its core brands—Kisses, Reese’s, Kit-Kat, and Hershey’s Chocolate Bar—have been wildly popular favorites for chocolate consumption. With the U.S. chocolate market set to surpass $20 billion by 2025, it makes sense that Hershey’s would stand to gain considerably from this secular tailwind.

Hershey’s decided to take it one step further by expanding and capitalizing on an even bigger market—the healthy snack industry. By 2025, it is expected that this market would grow to a value of $32 billion, which is even larger than the chocolate market.

The company made its first venture into the snacking business with the acquisition of Krave Jerky in 2015. It has since expanded its line of healthy products with the acquisition of healthy-snack companies Amplify, Pirate Brands, and ONE Brands.

With the significant number of competitors in the market, Hershey’s also needed to create a stronger strategy to reinvent itself into a more unique snacking firm to its consumers.

The company then developed the “snackfection” strategy, enabling it to provide a little twist to its traditional confectionery and snack items by adding a combination of sweet and savory flavors to the mix.

Hershey’s ability to listen to consumers and adapt to changes in their tastes enabled it to develop a wider variety of snacks that helped boost its product line growth. Some of the company’s newer creations included snack bars that have mixed nuts with real fruit, as well as other snack combinations of chocolate, popcorn, pretzels, and nuts.

With the company’s deeper move into the snacking industry, Hershey’s was able to achieve a wider consumer base and a more diverse set of consumables.

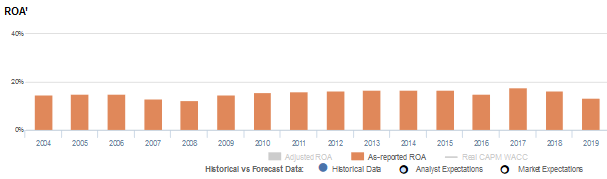

Looking at as-reported return on assets (ROAs), Hershey’s has had decent profitability over its operating history. That is, until recently, when ROAs began deteriorating to decade lows, levels not seen since the 2008 global financial crisis. It seems that its expansion into healthy snacks may not have been the right strategy for growth.

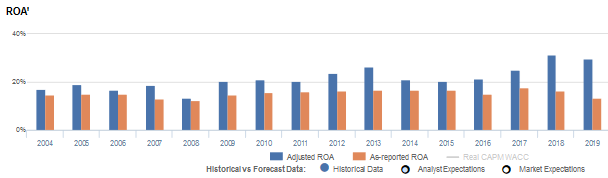

In reality, Uniform Accounting shows that Hershey’s efforts to expand its product offerings were successfully executed, with Uniform ROAs reaching new highs of over 30%.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of accumulated goodwill on Hershey’s balance sheet. In recent years, goodwill sits at about $1.8 billion to $1.9 billion, stemming from the company’s aforementioned acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Hershey’s earning power. Adjusting for goodwill, returns are actually significantly greater.

Hershey’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Hershey’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 13% in 2019, but its Uniform ROA was actually over 2x higher at 30%.

Furthermore, Hershey’s Uniform ROA has ranged from 13% to 31% in the past sixteen years while as-reported ROA ranged only from 12% to 18% in the same timeframe.

After ranging from 17%-19% levels in 2004-2007, Uniform ROA fell to 13% in 2008 before gradually expanding to 26% in 2013 and falling to 21% in 2014. Thereafter, Uniform ROA improved to a peak of 31% in 2018 before settling at 30% in 2019.

Hershey’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Hershey’s improvements in profitability has been driven by improving Uniform earnings margins, slightly offset by trends in Uniform asset turns.

After fading from 14% levels in 2004-2005, Uniform earnings margins faded to 9% in 2008, before stabilizing at 12%-13% levels through 2016. Thereafter, Uniform margins expanded to 16%-20% levels in 2017-2019.

Meanwhile, after steadily improving from 1.2x in 2004 to a peak of 2.0x in 2013, Uniform turns compressed to 1.6x levels through 2019.

At current valuations, the market is pricing in expectations for further improvements in Uniform margins and Uniform turns.

SUMMARY and Hershey’s Tearsheet

As the Uniform Accounting tearsheet for The Hershey Company (HSY) highlights, its Uniform P/E trades at 24.0x, which is around corporate average valuation levels but above its own recent history.

Average P/Es require average EPS growth to sustain them. In the case of Hershey’s, the company has recently shown a 3% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hershey’s’s Wall Street analyst-driven forecast is a 4% EPS shrinkage in 2020 before a 6% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hershey’s $146 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 3% each year over the next three years to justify current prices. What Wall Street analysts expect for Hershey’s’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows are 2x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Hershey’s’s Uniform earnings growth is around its peer averages in 2020. As warranted, the company is also trading in line with average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com