This retail holding company was able to offset inflation with strategic cost and expense management, achieving a Uniform ROA of 14%, not 5%

This retail holding company has continued its development and growth in various areas such as grocery retail, oil and mineral exploration, real estate, and liquor distribution.

However, as-reported metrics seem to show this company is just getting by despite being able to expand its products and range of businesses. On the other hand, Uniform Accounting shows that the business has better profitability in reality.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Although the retail industry has recovered from pandemic lows, high inflation rates have been a persistent headwind in an industry trying to recover to its pre-pandemic levels.

With the rising prices of goods making consumers more thoughtful about their purchases, many retailers continue to suffer from lower-than-expected returns despite the economy opening back up. However, there’s one retail holding company that does not seem to be experiencing this problem—Cosco Capital Inc. (COSCO:PHL).

Cosco is primarily engaged in the grocery and specialty retail, wine and liquor distribution, real estate, and oil and minerals businesses. It holds shares in various businesses including Puregold Price Club Inc. (supermarkets), Ellimac Prime Holdings (real-estate), Meritus Prime Distributions (liquor distribution), and Pure Petroleum (oil storage tanks).

Cosco’s growth in large part is due to its grocery retail segment, consisting 63% of its total net income. In 2022, Cosco posted P9.3 billion in net income for its grocery stores, a 14% increase from the previous year.

This is attributable to the company’s changes in strategic initiatives, specifically through stronger supplier support, sustained strategic costing, and expense management. This, coupled with the recovering levels of consumer demand, propelled Cosco to benefit from higher revenue growth across all its business segments.

In addition, Keepers Holdings, the largest imported liquor distributor in the Philippines and one of Cosco Capital’s subsidiaries, experienced a 41% growth in its net income for 2022.

Aside from organic growth strategies, the acquisitions of Island Mixers, a cocktail mixer brand, and Bodegas Williams & Humbert SA, the producers of Alfonso, further expands the portfolio of Cosco’s liquor distribution segment.

Cosco Capital also continued to focus on organic expansion and the opening of more grocery stores, with the company introducing 24 new Puregold stores and six new S&R stores. This brought its Puregold Group’s network to a total of 525 stores.

All in all, Cosco’s portfolio expansion via both acquisition and organic means has seen successful results in 2022. Effective cost management and pricing strategies have also allowed Cosco to offset the negative effects brought by inflation and other macroeconomic conditions.

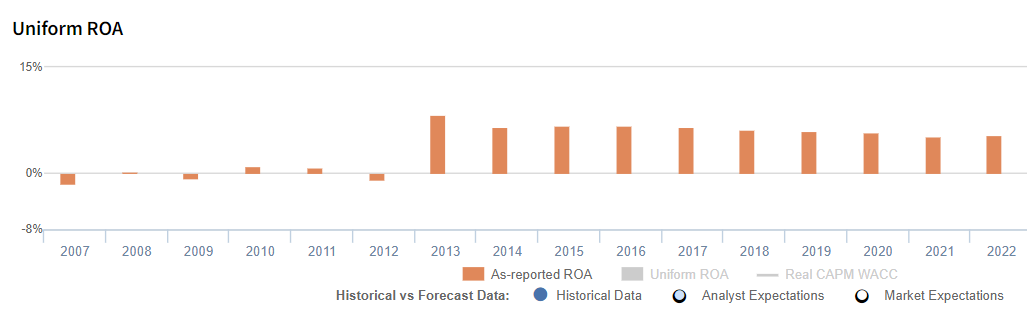

However, looking at as-reported data, it seems these strategies are being overlooked, with ROAs barely reaching above cost-of-capital levels.

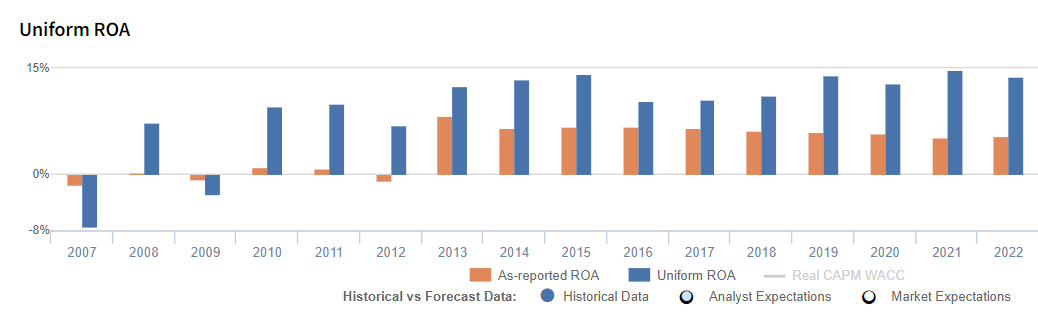

In reality, the company’s Uniform ROA was actually able to reach above cost-of-capital levels at 14%, almost tripling its as-reported ROA of 5%.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

For 2022, Cosco had a significant amount of excess cash sitting idly in its balance sheet of up to 25% of its as-reported total assets.

If we remove this item from Cosco’s asset base and with the many other necessary adjustments Valens makes, we arrive at a 14% Uniform ROA for 2022, nearly triple its as-reported ROA of only 5%.

Cosco’s profitability is much more robust than you think

As-reported ROA can distort the market’s perception of a firm’s profitability. For example, Cosco’s as-reported ROA has not surpassed 7% in the last nine years, hovering between 5%-6%.

However, a more accurate picture of the company’s profitability can be obtained by using Uniform Accounting, which adjusts for certain accounting choices that can artificially inflate or deflate ROA.

Using Uniform ROA, we can see that Cosco’s profitability was actually between 11%-15% for the past nine years, at least double the profitability that as-reported metrics show.

SUMMARY and Cosco Capital, Inc. Tearsheet

As the Uniform Accounting tearsheet for Cosco Capital, Inc. (COSCO:PHL) highlights, the company trades at a Uniform P/E of 5.3x, below the global corporate average of 18.4x, but around its historical P/E of 5.8x.

Low P/Es require low EPS growth to sustain them. In the case of Cosco, the company has recently shown a 6% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Cosco’s sell-side analyst-driven forecast is to see a Uniform earnings growth of 10% in 2023 and immaterial shrinkage in 2024.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cosco’s PHP 5.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 22% annually over the next three years. What sell-side analysts expect for Cosco’s earnings growth is above what the current stock market valuation requires through 2024.

Moreover, the company’s earning power is 2x the long-run corporate averages. However, cash flows and cash on hand are 7.4x the total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low dividend risk.

To conclude, Cosco’s Uniform earnings growth is below its peer averages and its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com