This semiconductor equipment company has positioned itself in the right markets, conducting Uniform ROAs more than double as-reported ROAs

For decades, electronic products have been the Philippines’ top export, making up at least half of total exports. Although the industry is vulnerable to economic disruptions, this semiconductor manufacturer has positioned itself to be able to buck that trend.

As-reported metrics fail to show the company’s potential, but Uniform Accounting reveals the opposite. Profitability may look like it is fading, but it is actually on the rise.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the past weeks, the COVID-19 vaccine has been making headlines around the world, as the U.S. government approved Pfizer’s and Moderna’s COVID-19 vaccine for emergency use.

The U.S. government’s action has given many countries, including the Philippines, confidence to begin negotiations with many COVID-19 vaccine providers.

However, the vaccine companies will still need approval from each country’s respective health agencies. In addition, vaccinating the majority of Filipinos would take a long while, even if there are enough doses for everyone.

As such, medical devices and other safety equipment will likely still be needed for much of 2021.

A seemingly unlikely company that benefits from persisting medical device demand is Cirtek Holdings Philippines Corporation (TECH:PHL), a semiconductor assembly and testing company.

Since many of the needed medical equipment are electronic, such as ventilators and oxygen level monitors, there is high demand for the computer chips enabling these devices.

Cirtek is well-positioned in medical chip production, committed to producing a million per week since April. While competitors will also see growth in 2020, this just comes mainly from the global economy’s recovery and from customers resuming investment plans.

Meanwhile, Cirtek is seeing growth tailwinds aside from the macro environment.

Even when most of the population has been vaccinated, demand for medical equipment will likely continue. Governments and hospitals will likely be looking to shore up their own medical equipment inventory in the event of a future pandemic.

Furthermore, Cirtek has been developing relationships in the rapidly growing 5G market. As the internet plays a more integral role to peoples’ daily lives, the value of a reliable and fast internet connection grows.

The Philippines and other developing countries are slow to catch up with the 5G trend, but this isn’t as much of an issue for Cirtek.

The company’s acquisition of the Silicon Valley company Quintel in 2017 allowed Cirtek to tap into the fragmented U.S. 5G market, where the U.S. telecom providers are still scrambling to lead the market.

In fact, just in September, Cirtek was able to sign a deal with an undisclosed U.S. telecom provider, where Cirtek will manufacture the antennas of the client’s 5G towers.

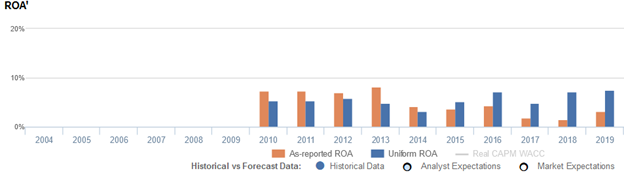

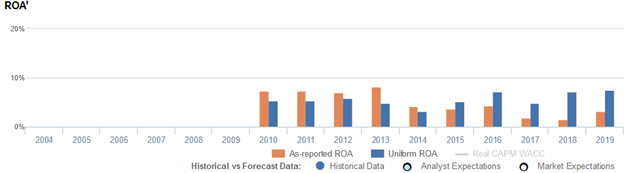

However, as-reported metrics give the idea that Cirtek is unable to take advantage of its secular growth trends. Since 2010, as-reported ROA has been on a general decline, standing at just 3% as of 2019.

Uniform Accounting shows the complete opposite of what as-reported metrics are suggesting.

Cirtek’s Uniform ROA has actually been on a general upswing since 2010, peaking at 8% in 2019. This implies the company is more capable of capitalizing on its medical device and 5G tailwinds than what the market may perceive.

As-reported metrics materially understate Cirtek’s profitability largely because of how goodwill, among many other accounting distortions, is treated.

As is the case with most mergers and acquisitions, management teams often pay a premium for the acquired assets, which increases the goodwill in the company’s balance sheet.

Although required by the Philippine Financial Reporting Standards (PFRS), goodwill artificially inflates the company’s asset base. It is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating assets.

Therefore, goodwill should be removed from the company’s assets.

With the $83.2 million acquisition of Quintel in 2017, Cirtek recognized $61.9 million of goodwill. Goodwill fell to $55.5 million in 2018-2019, but still amounted to 20% of the total as-reported assets in those years.

Removing $55.5 million from Cirtek’s assets, along with the many other necessary adjustments made, leads to an 8% Uniform ROA in 2019, significantly higher than their as-reported ROA of 3%.

Cirtek’s recent earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think Cirtek’s profitability has been weaker than real economic metrics have highlighted in the past five years.

In reality, Cirtek’s true profitability has been higher than as-reported ROA claims since 2015. Specifically, as-reported ROA was only 3% in 2019, but Uniform ROA actually peaked at 8% that year.

As-reported ROA sustained 7%-8% levels from 2010-2013, before gradually fading to a low of 1% in 2018. Since then, as-reported ROA has only recovered to 3% in 2019.

Meanwhile, after maintaining 5%-6% levels from 2010-2013, Uniform ROA dropped to 3% in 2014 and subsequently rebounded to 7% in 2016. Thereafter, Uniform ROA fell to 5% in 2017, before expanding to a peak of 8% in 2019.

Cirtek’s asset turns are stronger than you think

The strength in Cirtek’s Uniform ROA has been driven by strong Uniform asset turns. In fact, Uniform turns have been higher than as-reported asset turnover in each of the past five years.

Since 2010, as-reported asset turnover has slowly declined from 1.1x to 0.3x-0.4x lows in 2017-2019.

Meanwhile, Uniform turns were stable at 0.8x from 2010-2013, before contracting to 0.6x in 2014. Then, Uniform turns recovered to 0.7x in 2015-2016, before compressing to 0.5x in 2019.

Looking at the firm’s turns alone, as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and Cirtek Holdings Philippines Corporation Tearsheet

As the Uniform Accounting tearsheet for Cirtek Holdings (TECH:PHL) highlights, the Uniform P/E trades at 13.9x, which is below corporate averages and its own history.

Low P/Es require low EPS growth to sustain them. In the case of Cirtek, the company has recently shown a 15% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Cirtek’s sell-side analyst-driven forecast calls for a 5% Uniform EPS decline in both 2020 and 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cirtek’s PHP 7.08 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 8% each year over the next three years and still justify current valuations. What sell-side analysts expect for Cirtek’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is near the long-run corporate average, but cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, Cirtek’s Uniform earnings growth is well below peer averages, and the company is also trading well below peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com