This service provider continues to connect the world with its growth strategies, boosting Uniform ROA to 17%, not 9%

In 2020, we saw many companies file for initial public offerings (IPOs) despite the pandemic. That was also the same year we saw some of the biggest IPOs in Philippine history.

Specifically, one of these IPOs has been making waves across the globe through its expansion initiatives. However, as-reported metrics seem to think that that’s not the case.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

2020 was no doubt a tough year for small, medium, and large businesses. Some were able to hold on and stay afloat while others had no other choice but to close their doors permanently.

The Philippine stock market was even down 20% in the first half of the year, most of it caused by the 13% drop in value on March 19, 2020.

However, even with the noticeable market volatility during that time, many management teams still chose to take their companies public. They might have seen this period as an opportunity to expand their business, especially with the renewed investor interest in the market around mid-2020.

During the pandemic, the Philippines recorded some of the biggest IPOs in the country’s history, namely Monde Nissin Corporation (MONDE:PHL), Fruitas Holdings, Inc. (FRUIT:PHL), and Converge ICT Solutions, Inc. (CNVRG:PHL)

For Converge, the company highly depended on continued higher demand for online services given that people stayed at home most of the time. On top of that, the company is also banking on its expansion initiatives.

Specifically, in 2022, Converge acquired shares of Digital Telecommunications Phils. Inc. (DTPI) in the following firms in order to expand its telecommunication capabilities:

- Digitel Crossing Inc. (DCI) — maintains cable landing stations in the Philippines, which connects to the East Asia Crossing (EAC) and C2C cable systems. These two systems will help this company grow as they have useful landing points in Singapore, Hong Kong, China, Taiwan, South Korea, Japan, and the Philippines.

- Asia Netcom Philippines Corp. (ANPC) — on the other hand, holds land assets where the EAC cable landing station is found.

For context, landing stations are facilities where international cable systems connect or land.

Given that Converge is on a roll with its expansion initiatives, this deal helped the company bring its costs down despite increasing its presence internationally.

That same year, Converge also won an agreement to lease fiber lines and other types of support to SpaceX’s Starlink project.

According to the Department of Trade and Industry (DTI), the Philippines would be the first Southeast Asian country to use SpaceX’s technology, delivering high-speed satellite connectivity across the nation. As of February 2023, Starlink is already available in the Philippines.

These developments pushed Converge to achieve a 27% jump in consolidated revenue to PHP 33.7 billion.

On top of those achievements, the company also received the go signal to provide its internet services in Singapore through its new subsidiary, Converge ICT Singapore Pte. Ltd.

Overall, it seems that Converge has been nicely moving forward with its growth plans, which isn’t what as-reported data seems to show.

In reality, the company’s aggressive focus on its growth strategies enabled Converge to achieve a Uniform ROA of 17%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example, in 2022, Converge recognized an interest expense of PHP 1.7 billion, a third of as-reported net income of PHP 7.4 billion. When we add the PHP 1.7 billion back to earnings, because it is not an operating expense, Uniform Earnings is actually valued at PHP 8.5 billion.

Converge’s profitability is stronger than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

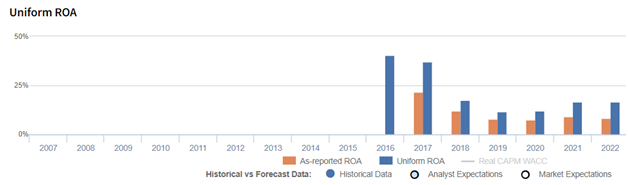

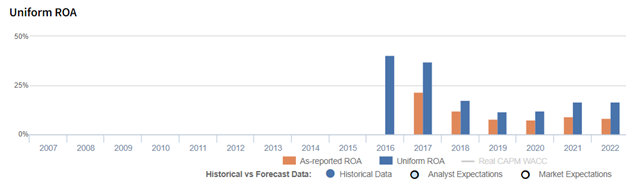

For example, Uniform ROA for Converge was 17% in 2022, substantially higher than the as-reported ROA of 9%, making the company appear to be a much weaker business than real economic metrics highlight for the past seven years.

Moreover, since 2016, Uniform ROA has reached a high of 41%, while as-reported ROA has already eclipsed at 22% in the same time frame, substantially distorting the market’s perception of the firm’s ceiling.

Converge has a more efficient business than you think

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

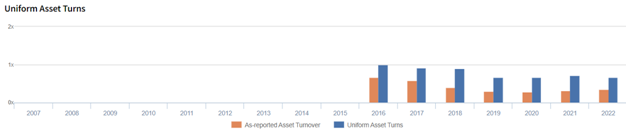

From 2016-2022, as-reported asset turnover declined from 0.7x to 0.3x, while Uniform turns only declined from 1.0x to 0.7x, making the company appear to be a less efficient business than real economic metrics reveal.

Moreover, as-reported asset turnover has been lower than Uniform turns in each of the past seven years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Converge ICT Solutions, Inc. Tearsheet

As our Uniform Accounting tearsheet for Converge ICT Solutions, Inc. (CNVRG:PHL) highlights, the company trades at a Uniform P/E of 14.6x, below the global corporate average of 18.4x and its historical P/E of 20.2x.

Low P/Es require low EPS growth to sustain them. In the case of Converge, the company has recently shown a 20% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Converge’s sell-side analyst-driven forecast is to see Uniform earnings shrinkage of 6% and a growth of 13% in 2023 and 2024, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Converge’s PHP 12.32 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 4% per year over the next three years. What sell-side analysts expect for Converge’s earnings growth is below what the current stock market valuation requires in 2023, but above its requirement in 2024.

Moreover, the company’s earning power is 3x the long-run corporate average. Additionally, cash flows and cash on hand are 2x of total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals an average credit and dividend risk.

To conclude, Converge’s Uniform earnings growth is in line with its peer averages, but below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com