This trading company’s strategic network and partnerships resulted in a 10% Uniform ROA, catching Buffett’s attention

Today’s company is the largest of Japan’s sogo shosha, driven by its massive network and presence in several industries and countries.

However, as-reported metrics do not seem to show how this helped the company to generate returns. Uniform Accounting shows that the business has a better Uniform return on assets (ROA) than what you might think.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

In one of our previous articles, we discussed how the automobile industry in Japan began from the first-ever gas-powered vehicle in the country. We also tackled how the Japanese zaibatsu, or influential conglomerates, ventured in the industry and how these large companies were dissolved into smaller companies after World War II.

As trade in Japan picked up in the 1950s, companies in the country began to diversify again. The remaining smaller units of the dismantled zaibatsu even merged to form new large-scale trading conglomerates, the sogo shosha.

Sogo shosha refers to a group of general trading companies in Japan. What sets these companies apart from other trading companies is their enormous market share, their international connections, and the large assortment of commodities they trade.

This scope gives these companies a significant influence, not only in the economy of Japan but also globally.

These sogo shosha were recently in the news when Warren Buffett’s company, Berkshire Hathaway, acquired shares of five of Japan’s biggest trading companies. It was also reported that the investing giant is looking for partnership opportunities between these companies and his current businesses.

One of the sogo shosha that Buffett invested in is today’s company of interest, Mitsubishi Corporation.

This company is more popularly known for manufacturing vehicles than as a trading conglomerate even though it is the largest trading company in Japan, operating in ten different business segments.

Starting as a shipping firm, Mitsubishi has expanded into various fields, such as urban development, power solution, petrochemicals, food, and automotives.

Since the company deals with numerous industries, partnerships and joint ventures are crucial to further its global footprint.

In 2018, due to rapid economic and population growth in Asia, Mitsubishi entered into a joint venture with a Singaporean government-owned consultancy company, Surbana Jurong. The JV’s purpose was to embark on urban development projects in Asian emerging markets such as the Philippines, Indonesia, India, and Vietnam.

Additionally, as the world becomes more digitized, Mitsubishi and HERE Technologies formed a partnership in 2020 to focus on improving efficiency in transportation and logistics for Japanese cities. This partnership also pushes Mitsubishi’s own digital initiatives by integrating HERE’s platform in the corporation’s many segments.

Finally, one of its most well-known partnerships is the Renault-Nissan-Mitsubishi Alliance, formed by the three companies to improve efficiency and increase their scale. Together, they are the world’s leading automotive alliance, selling 1 in 9 vehicles worldwide.

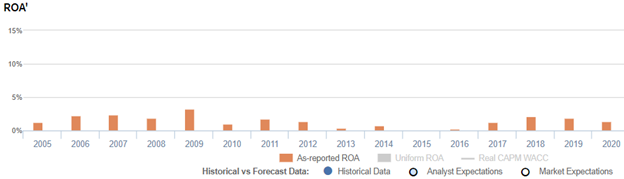

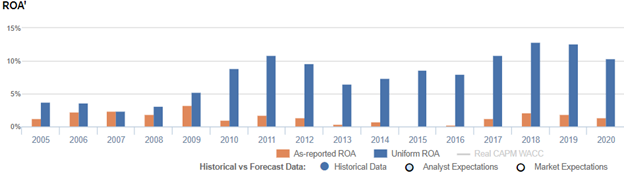

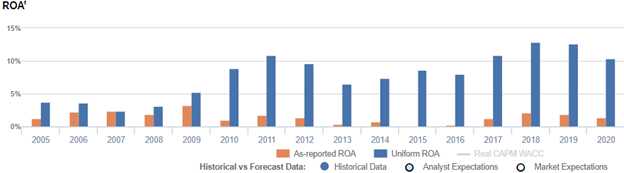

Seeing how influential and how large the network of this sogo shosha actually is, one might expect that Mitsubishi is enjoying robust returns. However, as-reported metrics do not seem to take this into account, showing an ROA of just 1% in 2020.

Uniform Accounting paints a totally different picture of the company’s profitability. Specifically, the company’s Uniform returns are actually significantly higher than its as-reported metrics in the past 16 years. In 2020, while as-reported ROA was only at 1%, Uniform ROA was actually 10 times that at 10%.

What as-reported data fails to do is to consider pension and OPEB cost as non-cash expenses. These are not operating expenses, and so when as-reported accounting includes these as expenses, earnings are incorrectly reduced and profitability is incorrectly lower than it should be.

In reality, pension and OPEB costs are simply actuarial adjustments, not operating expenses, and Uniform Accounting adds these back.

This mistreatment of pension and OPEB costs results in the distortion of as-reported ROA. After the adjustments were made, we can see that this sogo shosha isn’t performing weakly, but actually has more robust returns than what the market sees.

Mitsubishi’s profitability is much more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

Mitsubishi’s Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, when Uniform ROA was at 10% in 2020, as-reported ROA was only 1%.

The company’s Uniform ROA for the past sixteen years has ranged from 2% to 13%, while as-reported ROA has ranged only from 0% to 5% in the same timeframe.

Specifically, Uniform ROA declined from 4% in 2005 to 2% in 2007, before rebounding to 11% in 2011 and compressing to 7% in 2013. Then, Uniform ROA recovered to 10%-13% levels from 2017 onwards.

Mitsubishi’s Uniform earnings margins and Uniform asset turns are stronger than you think

Volatility in Uniform ROA has been driven by trends in both Uniform earnings margin and Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform margins declined from 4% in 2005 to 2% in 2007. It then recovered to 10% levels in 2010 to 2011, before gradually decreasing to 7% levels from 2013 to 2016. Uniform margins then reached peak levels of 12% in 2018 before falling back to 5% in 2020.

Meanwhile, Uniform turns remained at 0.9x-1.2x levels from 2005 to 2018, before rising to 2.0x in 2019 and 2020.

SUMMARY and Mitsubishi Corporation Tearsheet

As the Uniform Accounting tearsheet for Mitsubishi Corporation (8058:JPN) highlights, the Uniform P/E trades at 9x, which is below the global corporate average of 23.7x but around its own historical average of 8.1x.

Low P/Es require low EPS growth to sustain them. In the case of Mitsubishi, the company has recently shown a 25% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Mitsubishi’s sell-side analyst-driven forecast is a 16% and 5% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Mitsubishi’s JPY 2,935 stock price. These are often referred to as market embedded expectations.

Mitsubishi is currently being valued as if Uniform earnings were to shrink 15% annually over the next three years. What sell-side analysts expect for Mitsubishi’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 2x above the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals an average credit and dividend risk.

To conclude, Mitsubishi’s Uniform earnings growth is in line with its peer averages, but the company is trading below its average peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com